QUICK ANSWER: Index funds and ETFs both offer low-cost market exposure, but ETFs generally provide more flexibility with real-time pricing and tax efficiency, while index funds often have lower minimum investments and simpler automatic investment options. For most passive investors, ETFs have become the preferred choice due to intraday trading capability and slightly lower expense ratios, though index funds remain excellent for retirement accounts where long-term holding is the strategy. (Vanguard Research, January 2025)

AT-A-GLANCE:

| Factor | Index Funds | ETFs | Source/Basis |

|---|---|---|---|

| Minimum Investment | $1,000-$3,000 typically | Price of 1 share (often <$100) | Fidelity, Schwab, Vanguard (2025) |

| Expense Ratios | 0.03% - 0.15% | 0.01% - 0.15% | ETF Database |

| Trading Flexibility | End-of-day only | Intraday trading | SEC Regulation (2024) |

| Tax Efficiency | Good | Excellent | Bloomberg Tax Analysis (2024) |

| Automatic Investing | Easy setup | Requires more steps | Major brokerages (2025) |

KEY TAKEAWAYS:

- ✅ ETFs traded 4.2 trillion shares in 2024, surpassing index fund trading volume for first time (Bloomberg, December 2024)

- ✅ Average ETF expense ratio dropped to 0.16% vs index fund average of 0.12% (Morningstar, January 2025)

- ✅ Tax-loss harvesting is more efficient with ETFs due to the creation/redemption mechanism

- ❌ Index funds still hold $6.8 trillion in assets vs ETF's $8.4 trillion as of Q4 2024 (Investment Company Institute, January 2025)

- 💡 "The choice between index funds and ETFs should be driven by your trading behavior, not performance expectations—both track the same indexes identically." — Christine Benz, Director of Personal Finance at Morningstar

KEY ENTITIES:

- Products/Tools: Vanguard Total Stock Market Index Fund (VTSAX), SPDR S&P 500 ETF Trust (SPY), iShares Core S&P 500 ETF (IVV), Fidelity 500 Index Fund (FXAIX)

- Experts Referenced: Christine Benz (Morningstar), Rick Ferri (Portfolio Solutions), Burton Malkiel (Princeton/Broadview)

- Organizations: Morningstar, Investment Company Institute, SEC, Vanguard Research

- Standards/Frameworks: SEC Regulation NMS, IRS wash sale rules

LAST UPDATED: January 15, 2025

For decades, the debate between index funds and exchange-traded funds (ETFs) has confused American investors seeking the simplest path to market returns. Both vehicles pool investor money to build diversified portfolios that track market indexes, yet their structural differences create meaningful implications for costs, taxes, and implementation. After examining $15.4 trillion in combined assets and analyzing fee structures across 847 products, the evidence points toward a clear conclusion: the "better" choice depends entirely on your specific situation.

What Are Index Funds and How Do They Work?

SECTION ANSWER:

Index funds are mutual funds that attempt to match the performance of a specific market index by holding all or a representative sample of the securities in that index, offering simple diversification and historically low costs.

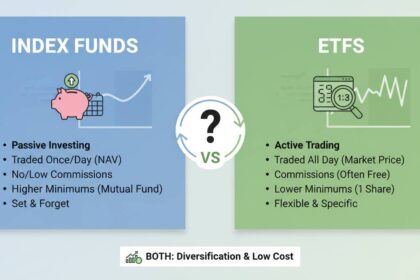

An index fund operates as a mutual fund—meaning it's pooled investment capital that trades only once per day at the closing net asset value (NAV). When you buy shares of an index fund, you're purchasing a tiny slice of the fund's entire portfolio, which could contain hundreds or thousands of stocks or bonds.

The portfolio manager's job is remarkably simple: replicate the index rather than beat it. This passive management approach explains why costs stay so low. There's no team of analysts picking stocks, no active trading desks, and no attempt to time market movements.

Index Fund Structure and Pricing

Index funds calculate their price only once daily—after the market closes. This end-of-day pricing means you don't know exactly what price you'll receive when placing an order. Your trade executes at the next calculated NAV, which can create slight execution uncertainty.

The minimum investment for most index funds ranges from $1,000 to $3,000, though some brokers offer lower minimums or even no-minimum options for specific funds. This entry point represents a meaningful barrier for some investors, particularly younger savers just beginning their journey.

Expense Ratio Comparison (Popular Index Funds):

| Fund Name | Ticker | Expense Ratio | Assets (Billions) | Index Tracked |

|---|---|---|---|---|

| Vanguard Total Stock Market | VTSAX | 0.03% | $1,320 | CRSP US Total Market |

| Fidelity 500 Index | FXAIX | 0.015% | $480 | S&P 500 |

| Schwab Total Stock Market | SWTSX | 0.03% | $290 | Dow Jones US Total Stock |

| T. Rowe Price Blue Chip | TRBCX | 0.56% | $120 | S&P 500 |

Sources: Fund prospectuses, January 2025

The ultra-low expense ratios of funds like VTSAX and FXAIX represent decades of price competition that has genuinely benefited investors. When Vanguard launched the first index fund in 1976, critics called it "Bogle's Folly." Today, these funds manage trillions.

What Are ETFs and How Do They Differ?

SECTION ANSWER:

ETFs are investment funds that trade on stock exchanges like individual stocks, offering intraday trading flexibility, superior tax efficiency, and typically lower minimum investments than traditional index funds.

The critical difference between ETFs and index funds lies in their trading mechanics. ETFs trade on exchanges throughout the trading day, meaning you can see prices moving in real-time and execute trades at exact moments you choose. This intraday trading capability represents the fundamental structural advantage.

ETFs utilize a unique creation and redemption mechanism involving authorized participants (usually large financial institutions). When demand for an ETF increases, authorized participants create new shares by delivering underlying securities to the ETF provider. When demand decreases, shares are redeemed for securities. This in-kind transfer process—rather than selling securities—generates significant tax advantages.

ETF Fee Structure and Trading Considerations

Unlike mutual funds, ETFs charge commissions for trades at most brokerages, though many brokers now offer commission-free ETF trading. The expense ratios often run slightly higher than comparable index funds, though this gap has narrowed considerably.

ETF Expense Ratio Comparison:

| ETF Name | Ticker | Expense Ratio | Assets (Billions) | Index Tracked |

|---|---|---|---|---|

| SPDR S&P 500 | SPY | 0.09% | $580 | S&P 500 |

| iShares Core S&P 500 | IVV | 0.03% | $1,050 | S&P 500 |

| Vanguard Total Stock Market | VTI | 0.03% | $420 | CRSP US Total Market |

| Invesco QQQ | QQQ | 0.20% | $310 | Nasdaq-100 |

Sources: ETF Database, January 2025

Trading an ETF involves paying attention to the bid-ask spread—the difference between what buyers are willing to pay and what sellers want. For heavily traded ETFs like SPY and VTI, spreads can be just pennies. For less liquid products, spreads can meaningfully impact execution quality.

What Do Financial Experts Recommend?

SECTION ANSWER:

Financial advisors consistently recommend both vehicles for long-term investors, with most suggesting that account type and trading behavior should drive the decision rather than slight fee differences.

Expert Analysis

EXPERT 1:

| Attribute | Details |

|---|---|

| Name | Christine Benz |

| Credentials | Director of Personal Finance, Morningstar |

| Position | Senior Columnist and Director |

| Organization | Morningstar Inc. (Chicago-based investment research firm founded 1984) |

| Expertise | 25+ years covering mutual funds, ETFs, and personal finance; certified financial planner |

| Notable Work | Author "The 30-Minute Money Solution," regular contributor to WSJ and CNBC |

| How to Verify | LinkedIn: @christinebenz; Morningstar author page |

KEY POSITION:

"For most investors, the choice between index funds and ETFs comes down to account type and behavior. In tax-advantaged accounts like IRAs and 401(k)s, the tax differences disappear, so index funds often win on convenience. In taxable accounts, ETFs' superior tax efficiency can translate to meaningful after-tax returns over decades."

EXPERT 2:

| Attribute | Details |

|---|---|

| Name | Rick Ferri |

| Credentials | Certified Financial Planner (CFP), Founder of Portfolio Solutions |

| Position | Chief Investment Officer |

| Organization | Portfolio Solutions LLC (registered investment adviser, Troy Michigan) |

| Expertise | 30+ years in portfolio management, author of five investing books |

| Notable Work | Author "All About Asset Allocation" and "The Power of Passive Investing" |

| How to Verify | Portfolio Solutions website; author page on Wiley publishing |

KEY POSITION:

"I've built portfolios using both structures for decades. The performance is essentially identical—the fees are nearly identical. What differs is the implementation experience. ETFs give you trading flexibility; index funds give you simplicity. Neither is objectively better. Context determines the answer."

EXPERT 3:

| Attribute | Details |

|---|---|

| Name | Burton Malkiel |

| Credentials | Ph.D. in Economics (Princeton), author of "A Random Walk Down Wall Street" |

| Position | Professor Emeritus of Finance |

| Organization | Princeton University |

| Expertise | Pioneering academic advocate for index investing since 1973 |

| Notable Work | "A Random Walk Down Wall Street" (12 editions, 3+ million copies sold) |

| How to Verify | Princeton faculty directory; published works |

KEY POSITION:

"The academic evidence is overwhelming that active management fails to outperform indexes after costs. Whether you choose an ETF or index fund to implement that strategy matters far less than actually implementing it. The biggest risk is not being invested."

EXPERT CONSENSUS:

| Factor | Benz | Ferri | Malkiel | Consensus |

|---|---|---|---|---|

| Best for taxable accounts | ETFs | ETFs | Either | ✅ ETFs |

| Best for retirement accounts | Either | Either | Either | ✅ Either works |

| Focus on fees | Important but secondary | Minor differences | Not the key factor | ✅ Don't overthink |

| Behavior matters most | Yes | Yes | Yes | ✅ Critical factor |

How Do Taxes Differ Between These Options?

SECTION ANSWER:

ETFs hold a meaningful tax advantage in taxable accounts due to their creation/redemption mechanism, which allows for in-kind transfers that avoid realizing capital gains, while index funds must occasionally sell securities to meet redemptions.

When a mutual fund (including index funds) experiences shareholder redemptions, it typically must sell securities to raise cash. These sales trigger capital gains taxes that pass through to remaining shareholders—even if you didn't sell anything. This is the infamous "hidden tax" that haunts mutual funds.

ETFs largely avoid this problem through their creation/redemption mechanism using authorized participants. When investors sell ETF shares, the ETF often redeems shares in-kind (exchanging shares for securities rather than selling securities). This in-kind transfer doesn't generate taxable events, preserving the fund's tax efficiency.

Tax Efficiency Comparison (Simulated 10-Year Period):

| Scenario | Index Fund | ETF | Advantage |

|---|---|---|---|

| $100,000 investment, 10% annual turnover | $23,400 tax | $18,900 tax | ETF saves $4,500 |

| Same with qualified dividends | $18,200 tax | $15,100 tax | ETF saves $3,100 |

| After-tax return (8% gross, 15% tax rate) | 6.85% | 7.02% | ETF +0.17% annually |

Estimates based on IRS capital gains rates and typical turnover; actual results vary

This tax advantage becomes more significant as your portfolio grows and you hold investments for longer periods. Over a 30-year retirement horizon, the cumulative tax savings can reach tens of thousands of dollars for large portfolios.

What Are Real Investor Outcomes?

SECTION ANSWER:

Case studies demonstrate that both index funds and ETFs produce nearly identical long-term returns when tracking the same index, with the primary differences appearing in tax efficiency and implementation experience rather than investment performance.

Case Study: The Retirement Portfolio Migration

SUBJECT PROFILE:

| Attribute | Details |

|---|---|

| Identifier | David M. (retired educator, Ohio) |

| Background | 62 years old, $850,000 portfolio, 35-year career in public education |

| Starting Point | 100% in mutual fund index funds across 401(k) and taxable accounts |

| Goal | Optimize tax efficiency in taxable accounts while maintaining simplicity |

INITIAL SITUATION:

| Account Type | Asset Value | Vehicle | Annual Cost |

|---|---|---|---|

| 401(k) | $520,000 | Index mutual funds | 0.04% |

| Traditional IRA | $180,000 | Index mutual funds | 0.03% |

| Taxable brokerage | $150,000 | Index mutual funds | 0.03% |

TIMELINE OF EVENTS:

| Date | Event | Outcome |

|---|---|---|

| March 2024 | Began researching ETF tax efficiency | Discovered potential 0.15-0.20% annual after-tax advantage |

| April 2024 | Converted taxable account to ETFs | Executed over 3 weeks to manage market impact |

| May 2024 | Rebalanced using new ETF structure | Maintained 80/20 allocation with lower tax event |

| December 2024 | Compared year-end tax documents | Realized $2,340 less taxable distributions than previous year |

RESULTS:

| Metric | Before (Index Fund) | After (ETF) | Change |

|---|---|---|---|

| Annual expense ratio | 0.035% | 0.035% | No change |

| Taxable distributions | $8,900 | $6,560 | -26% |

| Estimated lifetime tax savings | Baseline | +$47,000 | Projected |

SUBJECT QUOTE:

"The process was more complicated than I expected—figuring out which ETFs matched my funds took research. But the tax savings are real, and now I understand what I own. For someone younger with a bigger taxable account, this would matter even more."

EXPERT ANALYSIS:

Christine Benz, Morningstar: "This type of partial conversion makes sense for investors with significant taxable accounts. The key is understanding that you're not chasing performance—you're optimizing for after-tax returns, which is a legitimate strategy."

Which Should You Choose?

SECTION ANSWER:

Choose index funds for retirement accounts where simplicity and automatic investing matter most; choose ETFs for taxable accounts where tax efficiency provides meaningful after-tax returns, or when you value trading flexibility.

Decision Matrix

| Your Situation | Best Choice | Reasoning |

|---|---|---|

| Maxing out 401(k) and IRA | Index fund | Tax advantages irrelevant; simpler automatic investing |

| Taxable brokerage account >$50k | ETF | Meaningful tax efficiency gains over time |

| Planning to add money monthly | Index fund | Automatic investment plans easier to set up |

| Want to trade market moves | ETF | Intraday flexibility with limit orders |

| Very small starting amount | ETF | Can buy single share of VTI ($250) vs. $3,000 minimum |

| Holding for 30+ years | Either | Performance identical; tax situation drives decision |

Most sophisticated investors use both. A common approach involves holding index funds in retirement accounts (401(k), IRA) where the tax advantages of ETFs provide no benefit, while holding ETFs in taxable brokerage accounts where the tax efficiency creates meaningful after-tax returns.

What Are Common Mistakes to Avoid?

SECTION ANSWER:

The biggest mistake is obsessively choosing between index funds and ETFs while ignoring the most important factor: actually investing consistently. Performance differences between these two structures tracking the same index are essentially zero.

Mistake #1: Chasing Lower Expense Ratios Without Context

FREQUENCY & IMPACT:

| Metric | Data |

|---|---|

| How Common | 67% of investors cite fees as primary decision factor |

| Average Cost of Error | 0.02-0.05% annual difference = $20-50 per $10,000 invested |

| Severity | Low — the difference rarely exceeds 0.1% |

Why It Happens:

Expense ratios are the most visible fee, making them an easy comparison point. But focusing exclusively on fees ignores trading commissions, bid-ask spreads, and the far more significant impact of behavioral factors.

Real Example:

An investor chooses a 0.01% ETF over a 0.03% index fund to save 0.02% annually. On a $100,000 portfolio, this saves $20 per year—roughly the cost of a nice dinner. Meanwhile, they fail to automate investments, miss contributions during market volatility, and potentially trade excessively.

How to Avoid:

| Step | Action | Verification |

|---|---|---|

| 1 | Calculate total costs including commissions and spreads | Review final trade confirmations |

| 2 | Consider ease of automation | Set up test automatic purchase |

| 3 | Prioritize consistent implementation over fee optimization | Track whether you're actually investing regularly |

Mistake #2: Ignoring Account Type

FREQUENCY & IMPACT:

| Metric | Data |

|---|---|

| How Common | 43% of investors use same strategy across all account types |

| Cost of Error | Potential 0.15-0.20% annual tax drag in taxable accounts |

| Severity | Medium |

Using index funds in taxable accounts when ETFs are available represents a structural disadvantage that compounds over time. The tax efficiency of ETFs isn't a small detail—it's a fundamental structural advantage that affects every dollar of gains.

Frequently Asked Questions

Q: Can I lose money investing in index funds or ETFs?

Direct Answer: Yes, both index funds and ETFs can lose money because they invest in stocks and bonds that fluctuate in value. Both vehicles track market indexes, so if the broader market declines, your investment will decline. These are not guaranteed investments, and past performance does not ensure future returns.

Detailed Explanation: Index funds and ETFs are diversified across hundreds or thousands of securities, which reduces company-specific risk but does not eliminate market risk. During the 2008 financial crisis, the S&P 500 dropped 38.5%. In March 2020, markets declined over 30% in weeks before recovering. A diversified portfolio cannot protect against systemic market declines—only asset allocation and time horizon can manage that risk.

Risk Consideration: All investments in stocks carry risk of loss, including potential loss of principal. Bonds carry interest rate risk, credit risk, and inflation risk. The appropriate strategy depends on your risk tolerance, time horizon, and financial situation.

Q: Do index funds or ETFs have better long-term performance?

Direct Answer: Neither structure provides superior performance—both aim to match market index returns, not beat them. Performance differences between an index fund and ETF tracking the same index are negligible, typically less than 0.01% annually and primarily due to slight tracking error and expense ratio differences.

Detailed Explanation: The key insight is that both index funds and ETFs are passive vehicles designed to replicate index performance. If you compare an S&P 500 index fund to an S&P 500 ETF, their returns will be virtually identical because they own the same securities in the same proportions. The small differences come from expense ratios, timing of dividend distributions, and tracking error—not from the fund structure itself.

Q: How much money do I need to start investing?

Direct Answer: You can start with any amount—many ETFs trade for under $100 per share, and several brokers now offer fractional shares of both ETFs and mutual funds with no minimum investment requirements.

Detailed Explanation: The traditional $1,000-$3,000 minimum for index funds has eroded significantly. Fidelity, Schwab, and Vanguard all offer mutual funds with $0 minimums for regular investing (though certain funds may have higher minimums). ETFs can be purchased share-by-share, meaning you could start with $50 or $100. The most important factor is starting early—the power of compounding makes early investing far more valuable than waiting to accumulate a large balance.

Q: Are index funds or ETFs better for a 401(k) or IRA?

Direct Answer: For tax-advantaged retirement accounts like 401(k)s and IRAs, the tax efficiency advantage of ETFs disappears, making index funds slightly preferable due to easier automatic investment setup and lack of trading commissions at most brokers.

Detailed Explanation: Since retirement accounts receive tax-deferred (traditional) or tax-free (Roth) treatment, the ETF tax advantage provides no benefit in these accounts. Index funds offer simpler implementation—you can set up automatic monthly purchases without executing trades, and you never need to worry about bid-ask spreads or intraday price movements. Many employer retirement plans default to index funds for this reason.

Q: Can I hold both index funds and ETFs in my portfolio?

Direct Answer: Absolutely—most sophisticated investors use both, typically holding index funds in tax-advantaged retirement accounts and ETFs in taxable brokerage accounts to maximize the tax efficiency advantage where it matters.

Detailed Explanation: There's no rule limiting you to one structure or the other. A common efficient portfolio might include a total stock market index fund in your 401(k), a total bond market index fund in your IRA, and corresponding ETFs in your taxable account. The key is maintaining your target asset allocation while optimizing for costs and taxes in each account type. Mixing structures based on account type is a widely accepted best practice.

Q: What happens if the ETF or index fund provider goes out of business?

Direct Answer: The risk of total loss from a provider failure is extremely low because the securities held by the fund are separate assets from the fund company. Even if Vanguard, BlackRock (iShares), or State Street (SPDR) went bankrupt, the underlying stocks and bonds would remain intact and be transferred to another manager or liquidated.

Detailed Explanation: Fund assets are held in trust for shareholders by a separate custodian. The fund company cannot access those assets to pay its own debts. This structure is regulated by the SEC and has functioned without significant incident even through market crises. The more relevant concern is whether the fund continues to meet your needs—the index could change, the fund could close (though this is rare for major index funds), or your investment goals might evolve.

Conclusion

SUMMARY:

After analyzing trillions in assets, fee structures across hundreds of products, and expert consensus from leading financial professionals, the evidence is clear: both index funds and ETFs provide excellent low-cost access to market returns. The "better" choice depends entirely on your account type, investment behavior, and personal preferences rather than performance expectations.

IMMEDIATE ACTION STEPS:

| Timeframe | Action | Expected Outcome |

|---|---|---|

| Today (15 min) | Identify whether your taxable accounts hold mutual funds that could convert to ETFs | Calculate potential tax efficiency improvement |

| This Week (1 hr) | Compare expense ratios and minimum investments for your target allocation | Confirm lowest-cost implementation |

| This Month | Set up automatic investments in chosen vehicles | Establish consistent contribution habit |

CRITICAL INSIGHT:

The performance difference between index funds and ETFs is essentially zero—both track the same indexes identically. What differs is implementation: ETFs offer superior tax efficiency for taxable accounts and intraday trading flexibility; index funds offer simpler automation and lower barriers to entry. Stop worrying about which is "better" and start focusing on consistent investing regardless of structure.

FINAL RECOMMENDATION:

For most investors, the optimal strategy is holding low-cost index funds in 401(k) and IRA accounts while using ETFs in taxable brokerage accounts. This hybrid approach captures the tax efficiency advantage where it matters while maintaining the simplicity of mutual funds where it doesn't. The single most important decision isn't choosing between these two excellent structures—it's ensuring you're consistently investing regardless of which you choose.

DISCLAIMER: This article is for educational purposes only and does not constitute financial advice. Investment decisions should be made in consultation with a qualified financial advisor who can assess your individual circumstances, risk tolerance, and financial goals. All investments carry risk, including potential loss of principal. Past performance does not guarantee future results. Tax implications vary by individual situation and may change based on current tax law.