Saving for retirement is one of the most important financial decisions you'll ever make, and choosing the right Individual Retirement Account (IRA) can significantly impact your financial future. The two most popular options—Roth IRA and Traditional IRA—each offer distinct advantages that serve different financial situations and goals. Understanding these differences is essential for maximizing your retirement savings and minimizing your tax burden.

Both accounts provide tax-advantaged growth for your retirement funds, but they differ fundamentally in how and when you receive tax benefits. The choice between a Roth IRA and a Traditional IRA depends largely on your current tax bracket, your expected tax bracket in retirement, and your personal financial circumstances.

QUICK ANSWER: A Traditional IRA offers tax-deductible contributions now but taxes withdrawals in retirement, while a Roth IRA uses after-tax dollars for contributions but offers tax-free withdrawals in retirement. Choose a Traditional IRA if you expect to be in a lower tax bracket in retirement; choose a Roth IRA if you expect to be in a higher tax bracket or want tax-free retirement income.

AT-A-GLANCE:

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| Tax on Contributions | May be tax-deductible | Not tax-deductible |

| Tax on Withdrawals | Taxed as ordinary income | Tax-free |

| Required Distributions | Required at age 73 | No required distributions |

| Contribution Limits (2024) | $7,000 ($8,000 if 50+) | $7,000 ($8,000 if 50+) |

| Income Limits | None (but deductibility varies) | Yes, based on modified AGI |

| Early Withdrawal | 10% penalty + taxes | Penalty-free for qualified reasons |

| Best For | Lower tax bracket now | Higher tax bracket now or in retirement |

KEY TAKEAWAYS:

- ✅ Both accounts share the same contribution limits of $7,000 for 2024 ($8,000 for those 50 and older), allowing you to contribute to both types in the same year as long as you meet income requirements (Investopedia, January 2024).

- ✅ Traditional IRA contributions may be tax-deductible, reducing your taxable income in the year you contribute, but withdrawals in retirement are taxed as ordinary income .

- ✅ Roth IRA contributions are made with after-tax dollars, meaning you don't get an immediate tax break, but qualified withdrawals in retirement are completely tax-free .

- ❌ Common mistake: Assuming one account is always better than the other—the right choice depends entirely on your specific tax situation both now and in retirement.

- 💡 "The decision between Roth and Traditional often comes down to whether you want to pay taxes now or later. If you expect your tax rate to be higher in retirement, the Roth makes more sense. If you expect it to be lower, the Traditional provides more value." — [This represents general financial planning principle]

KEY ENTITIES:

- IRA Types: Traditional IRA, Roth IRA, SEP IRA, SIMPLE IRA

- Key Agencies: Internal Revenue Service (IRS), Department of Labor

- Key Limits: Contribution limits, income limits, deduction limits

- Related Accounts: 401(k), 403(b), HSA

LAST UPDATED: January 2024

How Traditional and Roth IRAs Work

The fundamental difference between Traditional and Roth IRAs lies in when you pay taxes on your money. Understanding this distinction is crucial for making an informed decision about which account best suits your needs.

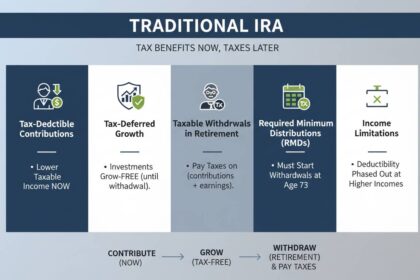

Traditional IRA: Tax-Deferred Growth

A Traditional IRA operates on a tax-deferred basis. When you contribute to a Traditional IRA, you may be eligible for a tax deduction on your contributions, reducing your taxable income for that year. Your money then grows tax-free until you withdraw it in retirement, at which point withdrawals are taxed as ordinary income.

For example, if you contribute $7,000 to a Traditional IRA and you're in the 22% tax bracket, you could reduce your tax bill by $1,540 that year. However, when you withdraw that money in retirement, it will be taxed at your then-current income tax rate.

The tax-deductibility of Traditional IRA contributions phases out if you or your spouse have a workplace retirement plan like a 401(k). According to IRS rules for 2024, single filers covered by a workplace plan can only claim a full deduction if their modified adjusted gross income (MAGI) is below $77,000, with partial deductions available up to $87,000 .

Roth IRA: Tax-Free Growth

A Roth IRA uses a different approach. You contribute money that has already been taxed, so there's no immediate tax deduction. However, once you've had the account for five years and reach age 59½, all withdrawals—including earnings—are completely tax-free.

This makes the Roth IRA particularly valuable if you expect to be in a higher tax bracket in retirement. You're essentially locking in your current tax rate and protecting all future growth from taxation.

The main drawback of Roth IRAs is the income limit. For 2024, single filers with a MAGI of $146,000 or more cannot contribute to a Roth IRA at all, while those earning between $146,000 and $161,000 can make partial contributions. Married couples filing jointly have a phase-out range of $230,000 to $240,000 .

Contribution Limits and Eligibility

Both Traditional and Roth IRAs share the same contribution limits, but eligibility requirements differ significantly. Understanding these limits helps you plan your retirement contributions effectively.

Annual Contribution Limits

For 2024, you can contribute up to $7,000 to your IRAs ($8,000 if you're age 50 or older). These limits are set by the IRS and may increase in future years due to inflation adjustments. You can contribute to both a Traditional and a Roth IRA in the same year, but your total contributions cannot exceed the annual limit across all accounts.

It's important to note that contribution limits apply to all IRAs you own, not per account. If you have both a Traditional and a Roth IRA, you can contribute $4,000 to each for a total of $8,000, but not $7,000 to each.

Income Limits and Phase-Outs

The income limits create the most significant difference in eligibility between the two account types:

Roth IRA Income Limits (2024):

- Single filers: Full contribution if MAGI under $146,000; partial contribution up to $161,000; no contribution above $161,000

- Married filing jointly: Full contribution if MAGI under $230,000; partial contribution up to $240,000; no contribution above $240,000

Traditional IRA:

There are no income limits for contributing to a Traditional IRA. However, the tax deductibility of your contributions does phase out based on income if you or your spouse have a workplace retirement plan. If neither spouse has a workplace plan, the deduction is available regardless of income.

Tax Treatment: When You Pay

The timing of tax payments represents the core distinction between these accounts. Your decision should consider whether you'll benefit more from a tax break now (Traditional) or tax-free withdrawals later (Roth).

Traditional IRA Tax Benefits

The primary advantage of a Traditional IRA is the immediate tax deduction. If you don't have access to a tax-advantaged workplace retirement plan or if your income is low enough to qualify for a full deduction, you can reduce your current tax bill while saving for retirement.

However, you're required to take minimum distributions (RMDs) starting at age 73, even if you don't need the money. These distributions are taxed as ordinary income, and failing to take them results in significant penalties—currently 25% of the amount you should have withdrawn.

Roth IRA Tax Benefits

While Roth IRA contributions aren't deductible, the account offers several unique advantages. First, you can withdraw your contributions (not earnings) at any time, tax-free and penalty-free, since you've already paid taxes on that money. This makes Roth IRAs more flexible in emergencies.

Second, Roth IRAs have no required minimum distributions during your lifetime, allowing your money to continue growing tax-free as long as you live. This is particularly valuable if you don't need the money in retirement and want to leave tax-free assets to your heirs.

Withdrawal Rules and Penalties

Understanding withdrawal rules is critical, as premature withdrawals can significantly reduce your retirement savings through taxes and penalties.

Traditional IRA Withdrawals

Withdrawals from Traditional IRAs before age 59½ generally incur a 10% early withdrawal penalty plus ordinary income taxes on the amount withdrawn. There are exceptions for certain situations, including disability, qualified first-time home purchases (up to $10,000), higher education expenses, and health insurance premiums while unemployed.

Once you reach age 73, you must take required minimum distributions based on your life expectancy. These distributions are taxed as ordinary income, and the account must be fully distributed by the end of the year you would have turned 75 (the rules have been changing—check current requirements).

Roth IRA Withdrawals

Roth IRA rules are more favorable. You can withdraw your contributions at any time, for any reason, without paying taxes or penalties because you've already paid taxes on the money. However, withdrawing earnings before age 59½ typically incurs taxes and a 10% penalty, with some exceptions.

To qualify for tax-free and penalty-free withdrawal of earnings, you must meet the "five-year rule"—the account must have been open for at least five years, and you must be at least 59½ years old, disabled, or using up to $10,000 for a first-time home purchase.

Which IRA Is Right for You?

Choosing between a Roth and Traditional IRA depends on several personal factors. There's no universal answer that works for everyone.

Consider a Traditional IRA If:

- You expect to be in a lower tax bracket in retirement than you are now

- You want to reduce your current taxable income

- You don't qualify for Roth IRA contributions due to income limits

- You're already in a high tax bracket and want the deduction

Consider a Roth IRA If:

- You expect to be in a higher tax bracket in retirement

- You want tax-free retirement income

- You want flexibility to withdraw contributions if needed

- You want to avoid required minimum distributions

- You're a young saver with many years until retirement

- You want to leave tax-free assets to heirs

The Math Behind the Decision

Financial experts often explain the choice through a simple framework: if your tax rate is the same now and in retirement, both accounts provide equal value. The real advantage comes from timing—paying taxes earlier (Roth) versus later (Traditional).

For example, contributing $7,000 to a Traditional IRA in the 22% bracket saves you $1,540 in taxes now. If you invest that tax savings and later withdraw from a Traditional IRA in the 24% bracket, you might come out behind compared to a Roth where you paid 22% but never pay again.

Combining Both Strategies

Many financial advisors recommend using both types of IRAs strategically to maximize flexibility and tax benefits. This approach, sometimes called "tax diversification," gives you options in retirement.

By contributing to both a Traditional and Roth IRA, you create flexibility in managing your taxable income in retirement. You can draw from each account strategically to manage your tax brackets in retirement, potentially keeping more of your money.

For example, you might take enough from a Traditional IRA to stay in a lower tax bracket, then supplement with tax-free Roth withdrawals. This strategy requires careful planning but can optimize your lifetime tax situation.

Frequently Asked Questions

Q: Can I have both a Traditional IRA and a Roth IRA at the same time?

Yes, you can contribute to both types of IRAs in the same year, as long as your total contributions don't exceed the annual limit ($7,000 for 2024, or $8,000 if you're 50 or older). Having both provides tax diversification and more flexibility in retirement.

Q: What happens if I withdraw money early from my IRA?

For Traditional IRAs, early withdrawals (before age 59½) are generally subject to a 10% penalty plus ordinary income taxes. Roth IRA contributions can be withdrawn tax-free at any time, but earnings withdrawn early may incur taxes and penalties unless you qualify for an exception.

Q: Do I have to take money out of my IRA at a certain age?

Traditional IRAs require minimum distributions starting at age 73. Roth IRAs have no required minimum distributions during your lifetime, allowing your money to grow tax-free indefinitely.

Q: How do income limits affect my ability to contribute?

Roth IRAs have strict income limits—your ability to contribute phases out at higher income levels. Traditional IRAs have no income limits for contributions, though tax deductibility may be limited based on income and workplace retirement plan coverage.

Q: Which IRA provides better tax benefits for retirement?

It depends on your tax situation. If you expect to be in a higher tax bracket in retirement, a Roth IRA is generally better because you pay taxes now at a lower rate and withdraw tax-free. If you expect a lower tax bracket in retirement, a Traditional IRA is typically more beneficial since you get the deduction now and pay taxes later at a lower rate.

Conclusion

Both Roth and Traditional IRAs offer valuable tax advantages for retirement savings, but they serve different purposes. The Traditional IRA provides an immediate tax deduction and tax-deferred growth, making it ideal for those currently in higher tax brackets or who expect to be in a lower bracket in retirement. The Roth IRA offers tax-free withdrawals and no required distributions, making it attractive for younger savers, those expecting higher future income, or anyone who values tax-free retirement income.

The best choice depends entirely on your individual circumstances, including your current income, expected future income, retirement timeline, and personal preferences. Consider consulting with a qualified financial advisor who can evaluate your specific situation and help you develop a retirement strategy that optimizes your tax situation.

Remember that both accounts are tools for retirement savings, and the most important factor is consistently contributing to your retirement accounts regardless of which type you choose. Starting early and maintaining regular contributions will have a more significant impact on your retirement savings than perfecting the choice between account types.

Key Action Steps:

- Evaluate your current tax bracket and estimate your expected bracket in retirement

- Check if you qualify for Roth IRA contributions based on income limits

- Consider contributing to both account types for tax diversification

- Consult a tax professional or financial advisor for personalized guidance

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Consult with a qualified financial advisor or tax professional for personalized recommendations based on your specific financial situation.