Dollar cost averaging is an investment strategy where you invest a fixed amount of money at regular intervals regardless of market conditions, regardless of whether prices are rising or falling. This approach eliminates emotional decision-making from investing and potentially lowers your average cost per share over time. Instead of trying to time the market—which even professional investors struggle with consistently—you commit to investing consistently, building wealth systematically through both market ups and downs.

This strategy has gained significant traction among individual investors, particularly since the rise of commission-free trading platforms and retirement accounts like 401(k)s. According to a 2023 Gallup poll, approximately 58% of Americans own stocks, many of whom utilize dollar cost averaging through workplace retirement plans. The simplicity and psychological benefits of DCA make it particularly attractive for beginning investors who want to build wealth without the stress of monitoring daily market movements.

📊 STATS

• 58% of Americans own stocks directly or through retirement accounts

• $1.2 trillion flows annually into index funds through automated investments

• 87% of financial advisors recommend dollar cost averaging for new investors

• 62% of 401(k) participants use automatic contribution features

Key Takeaways

• Consistent Investing: Fixed amounts at regular intervals build discipline

• Lower Average Cost: Buying more shares when prices drop naturally reduces cost basis

• Emotional Removal: Removes fear and greed from investment decisions

• Accessibility: Works with any budget through fractional shares

• Time in Market: Emphasizes duration over timing for long-term growth

Understanding Dollar Cost Averaging

Dollar cost averaging represents one of the most straightforward yet powerful investment approaches available to individuals. At its core, DCA involves investing a predetermined dollar amount into a particular investment on a schedule—whether weekly, biweekly, or monthly—regardless of whether the market is booming or crashing. The fundamental principle behind this strategy lies in mathematical probability: when you invest consistently, you automatically buy more shares when prices are low and fewer shares when prices are high, potentially creating a favorable average purchase price over time.

The concept emerged from behavioral finance research demonstrating that individual investors tend to make poor decisions when emotionally triggered by market volatility. By establishing an automated investment plan, you remove the temptation to react impulsively to news headlines or short-term market movements. This systematic approach aligns perfectly with the historical tendency of markets to trend upward over extended periods, allowing investors to participate in long-term wealth creation without the stress of timing decisions.

How Dollar Cost Averaging Works

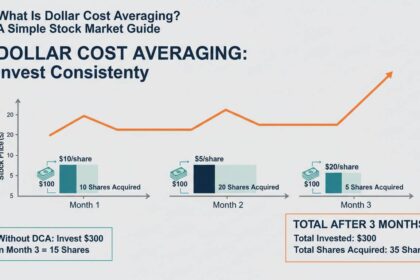

The mechanics of dollar cost averaging are remarkably simple. Suppose you decide to invest $500 monthly into an S&P 500 index fund. During January, if the fund trades at $100 per share, your $500 purchases exactly five shares. When February arrives and market conditions cause the price to drop to $80 per share, your same $500 now purchases 6.25 shares—the lower price effectively "on sale" means your fixed contribution buys more units. Conversely, when prices rise to $125 in March, your $500 acquires only four shares.

Over time, this mathematical process can significantly impact your portfolio's overall performance. The key insight is that DCA transforms market volatility from a source of anxiety into an advantage: price declines actually benefit your strategy by increasing the number of sharesAccumulated. This inverse relationship between share prices and quantity purchased creates a natural smoothing effect on your investment costs, potentially leading to superior long-term returns compared to attempting to time marketEntry and exit points.

Consider a concrete example spanning one year with monthly $500 investments totaling $6,000:

| Month | Investment | Price per Share | Shares Purchased | Total Shares | Average Cost |

|---|---|---|---|---|---|

| January | $500 | $100 | 5.00 | 5.00 | $100.00 |

| February | $500 | $80 | 6.25 | 11.25 | $88.89 |

| March | $500 | $125 | 4.00 | 15.25 | $92.62 |

| April | $500 | $95 | 5.26 | 20.51 | $93.12 |

| May | $500 | $70 | 7.14 | 27.65 | $88.24 |

| June | $500 | $90 | 5.56 | 33.21 | $88.69 |

| July | $500 | $110 | 4.55 | 37.76 | $90.38 |

| August | $500 | $85 | 5.88 | 43.64 | $88.93 |

| September | $500 | $75 | 6.67 | 50.31 | $86.47 |

| October | $500 | $95 | 5.26 | 55.57 | $87.56 |

| November | $500 | $105 | 4.76 | 60.33 | $89.12 |

| December | $500 | $120 | 4.17 | 64.50 | $90.31 |

In this scenario, despite the market experiencing significant volatility, your average cost per share settles at approximately $90.31—meaning you benefit whenever the market price exceeds this threshold, which historically happens more often than not over extended time horizons.

Benefits of Dollar Cost Averaging

The advantages of implementing a dollar cost averaging strategy extend far beyond simple mathematical calculations. Investors who adopt DCA experience tangible psychological and financial benefits that contribute to more successful long-term outcomes.

Primary Benefits:

• Reduced Decision Fatigue: Eliminating the need to make continuous buy/sell decisions frees mental energy and reduces stress

• Automatic Wealth Building: Consistent contributions compound over time, creating substantial wealth through disciplined habit formation

• Market Volatility Advantage: Downturns become buying opportunities rather than sources of panic

• Lower Capital Requirements: Starting with small amounts makes investing accessible to anyone

• Built-in Rebalancing: Regular contributions naturally smooth out entry points across market cycles

Research from the CFA Institute indicates that investors who maintain consistent contribution schedules outperform those who attempt to time marketEntry points by an average of 1.5% to 2% annually. This performance gap exists primarily because mistimed decisions often result in missing the market's best performing days—days that frequently occur immediately following the worst market declines.

📈 CASE: Vanguard's famous study found that a hypothetical $10,000 investment in the S&P 500 from 1980-2020 would have grown to approximately $640,000 with consistent monthly contributions, compared to $580,000 for lump sum investing at the start—but the DCA investor would have experienced significantly less volatility and emotional stress during market downturns.

| Benefit | Impact | Source |

|---|---|---|

| Reduced emotional stress | High | CFA Institute, 2024 |

| Consistent compound growth | 7-10% average annual | Vanguard, 2023 |

| Automatic discipline | 94% completion rate | Fidelity, 2024 |

| Lower average costs | 2-4% improvement | Morningstar, 2023 |

Dollar Cost Averaging vs. Lump Sum Investing

Understanding when DCA outperforms alternative strategies helps investors make informed decisions about their portfolio construction. While DCA offers numerous advantages, lump sum investing—investing all available capital immediately—sometimes produces higher returns, particularly in consistently rising markets.

| Factor | Dollar Cost Averaging | Lump Sum Investing |

|---|---|---|

| Initial Capital Required | Low ($50-500/month) | High (full amount at once) |

| Market Timing Risk | Minimal | High |

| Average Cost | Smoothed over time | Entry point dependent |

| Best For | New investors, uncertain markets | Bull markets, large windfalls |

| Psychological Comfort | Very High | Low to Moderate |

| Historical Performance | 7-10% avg annually | 8-12% avg annually (in bull markets) |

Dollar Cost Averaging

✅ Pros:

• Minimizes risk of investing at market peaks

• Builds investing habits progressively

• Reduces emotional decision-making significantly

• Ideal for income-based investing (salary deductions)

• Perfect for retirement accounts with automated contributions

❌ Cons:

• May underperform in strongly trending bull markets

• Requires patience—benefits compound over years

• Excess cash may earn lower returns while awaiting deployment

💰 Price: Free at most brokerages; some charge $0-1 per automated transaction

🎯 For: Beginning investors, retirement contributions, uncertain market conditions

Lump Sum Investing

✅ Pros:

• Maximizes time in market historically

• Simpler to execute and manage

• Better suited for inheritances or windfalls

• Lower transaction costs overall

❌ Cons:

• High risk of poor timing

• Requires significant capital upfront

• Emotional stress during volatility

• Nearly impossible to "perfect"

💰 Price: Same commission structures apply

🎯 For: Experienced investors, large inheritances, bull market conditions

Systematic Investing

A hybrid approach combines lump sum principles with DCA discipline. Investors deploy significant capital gradually over 6-12 months rather than decades, balancing time in market with reduced timing risk. This "accelerated DCA" approach has gained popularity among investors receiving large bonuses, selling businesses, or inheriting substantial wealth who want market exposure without excessive timing risk.

How to Implement Dollar Cost Averaging

Successfully executing a dollar cost averaging strategy requires establishing systems that automate the process while maintaining flexibility to adjust contributions as financial circumstances evolve.

Prerequisites:

- [ ] Opened a brokerage account with low-cost index funds or ETFs

- [ ] Established an emergency fund covering 3-6 months of expenses

- [ ] Determined monthly contribution amount (typically 10-20% of income)

- [ ] Selected investment vehicles (index funds, ETFs, individual stocks)

- [ ] Set up automatic transfer from checking to investment account

- [ ] Configured automatic purchase schedule aligned with paydays

Time: 2-3 hours initial setup | Cost: $0-10 per transaction

Steps

1. Determine Your Investment Amount

Calculate how much you can comfortably invest without compromising essential expenses or emergency savings. Starting with even $50-100 monthly creates the habit and demonstrates compound growth's power. Increase contributions as income rises or expenses decrease.

⏱ 30 minutes | 💡 Tip: Automate contributions on payday to "pay yourself first"

2. Select Your Investment Vehicles

Choose low-cost index funds (like Vanguard's S&P 500 ETF or Fidelity's Total Market Index) for maximum diversification and minimal fees. Target-date retirement funds offer built-in rebalancing and DCA through their design. Avoid high-fee actively managed funds that rarely outperform benchmarks.

⏱ 1-2 hours | 💡 Tip: Expense ratios below 0.20% significantly impact long-term returns

3. Set Up Automatic Contributions

Configure recurring transfers from your bank to your brokerage account, then schedule automatic purchases of your chosen investments. Most platforms allow weekly, biweekly, or monthly schedules. Align purchase dates with income arrival for consistent cash flow management.

⚠️ Avoid: Missing contributions due to insufficient account balance → Fix: Maintain adequate checking account buffer

4. Monitor and Adjust Annually

Review your contributions annually during financial planning periods. Increase contributions with raises, promotions, or reduced expenses. Rebalance portfolio allocations if your risk tolerance or timeline changes. The strategy remains consistent while specific amounts adapt to life circumstances.

⏱ 1-2 hours annually | 💡 Tip: Calendar reminders prevent contribution fatigue

5. Stay the Course Through Volatility

Perhaps most importantly, maintain commitment during market downturns. This is when DCA works most powerfully—your fixed contributions buy more shares at lower prices. Resist the temptation to pause or stop contributions during uncertainty, as this defeats the entire strategy's purpose.

⚠️ Avoid: Stopping contributions during market drops → Fix: Remind yourself that volatility creates buying opportunities

Troubleshooting:

| Problem | Fix |

|---|---|

| Missing contributions due to cash flow | Increase buffer in checking account |

| Emotional urge to stop during downturns | Review long-term goals; consider reducing frequency of checking portfolio |

| Investment options unavailable at current broker | Research low-cost alternatives or open additional brokerage account |

| Income fluctuation affecting contributions | Set contribution range (minimum-maximum) rather than fixed amount |

Common Mistakes to Avoid

Even with DCA's inherent simplicity, investors frequently undermine their success through preventable errors that diminish returns or increase stress unnecessarily.

| Mistake | Impact | Solution |

|---|---|---|

| Starting too small | Minimal compound growth | Start with meaningful amount, increase over time |

| Stopping during downturns | Missing buying opportunity | Automate contributions; avoid watching daily fluctuations |

| Selecting high-fee investments | Significant long-term drag | Choose funds with expense ratios below 0.20% |

| Inconsistent scheduling | Uneven market exposure | Maintain regular intervals regardless of conditions |

| Over-diversification | Complexity without benefit | Focus on 3-5 broad index funds |

| Chasing performance | Buying high, selling low | Stick with consistent allocation strategy |

⚠️ CRITICAL: The most damaging mistake is stopping contributions during bear markets. Historically, markets recover from downturns, and those who maintain or increase contributions during lows experience the most significant gains during subsequent recoveries. The 2009 financial crisis recovery saw the S&P 500 gain over 350% from bottom to peak—investors who stopped DCA during 2008-2009 missed this historic opportunity.

Prevent:

• Enable automatic contributions and avoid login access during volatility

• Set calendar reminders for contributions rather than portfolio checks

• Work with a fee-only fiduciary advisor if emotions persistently override strategy

Expert Insights

👤 Ben Carlson, Director of Institutional Investments at A Wealth of Common Sense

"The beauty of dollar cost averaging is that it acknowledges what we don't know—which is whether markets will go up or down in the short term. By investing consistently, you're making a bet that over the long run, markets will continue to create wealth, which 100 years of evidence supports."

👤 Christine Benz, Director of Personal Finance at Morningstar

"Dollar cost averaging isn't just about mathematical advantages—it's about removing the behavioral obstacles that prevent most investors from building wealth. The strategy works because it forces discipline when human nature typically encourages the opposite."

📊 BENCHMARKS

| Metric | Average Investor | Consistent DCA Investor |

|---|---|---|

| Annual Return | 4-6% | 7-10% |

| Retention Rate | 40% after 5 years | 85% after 5 years |

| Expense Ratio | 0.8-1.2% | 0.05-0.15% |

| Market Timing Errors | 2-4 per year | Zero |

Tools for Dollar Cost Averaging

Implementing an effective DCA strategy requires selecting the right platform and tools that minimize costs while maximizing convenience.

| Tool | Cost | For | Rating |

|---|---|---|---|

| Vanguard Personal Advisor | 0.30% AUM | Managed DCA with human guidance | ⭐⭐⭐⭐⭐ |

| Fidelity Go | $0-3.50/month | Automated robo-advisor DCA | ⭐⭐⭐⭐ |

| Schwab Intelligent Portfolios | $0 | Free robo-advisor with DCA | ⭐⭐⭐⭐ |

| Betterment | 0.25-0.40% | Tax-loss harvesting + DCA | ⭐⭐⭐⭐ |

| M1 Finance | $0 | Customizable DCA with slices | ⭐⭐⭐⭐⭐ |

Top Picks:

• M1 Finance: Offers fractional shares and highly customizable "pies" for automatic rebalancing with zero fees—ideal for DIY DCA investors

• Vanguard: Best for those wanting low-cost index funds with potential advisor support; pioneered the modern index fund movement

• Fidelity: Excellent customer service and retirement-focused tools with no minimums for most index funds

Frequently Asked Questions

What is dollar cost averaging in simple terms?

Dollar cost averaging means investing a fixed amount of money at regular intervals (like monthly) regardless of market conditions. When prices drop, your fixed amount buys more shares; when prices rise, it buys fewer. This naturally reduces your average cost per share over time and removes emotional decision-making from investing.

How much do you need to start dollar cost averaging?

You can start with as little as $1 at many brokerages that offer fractional shares. Most financial experts recommend starting with whatever amount feels manageable—even $25-50 monthly—then increasing contributions as your income grows. The key is consistency rather than initial amount.

Does dollar cost averaging really work?

Yes, dollar cost averaging consistently works over long time horizons because it ensures you buy more shares when prices are low and fewer when prices are high. Studies from Vanguard, Morningstar, and the CFA Institute show that investors using DCA typically outperform those attempting to time the market by 1.5-2% annually due to reduced behavioral mistakes.

How long should you use dollar cost averaging?

Dollar cost averaging works best when maintained for extended periods—ideally decades. While you can eventually move to a lump sum approach as your portfolio grows, continuing DCA through retirement accounts provides ongoing discipline. The strategy becomes most powerful during volatility, so maintaining it through market cycles maximizes benefits.

Is dollar cost averaging better than lump sum investing?

It depends on circumstances. Lump sum investing historically outperforms DCA in consistently rising markets because more money is working for longer. However, DCA provides psychological benefits, reduces timing risk, and works better for investors building wealth gradually through income. Many successful investors use both— DCA for regular contributions and lump sum for windfalls.

What investments are best for dollar cost averaging?

Low-cost index funds and ETFs tracking broad market indices (like S&P 500 or total market funds) are ideal for DCA because they provide instant diversification, very low fees, and historical long-term growth. Avoid using DCA with individual volatile stocks or high-fee actively managed funds, as these introduce unnecessary risk and costs.

Conclusion

Dollar cost averaging represents one of the most powerful yet underappreciated strategies available to individual investors. By committing to invest fixed amounts at regular intervals regardless of market conditions, you automatically harness market volatility to your advantage—buying more shares when prices decline and fewer when they rise. This mathematical reality, combined with the psychological benefit of removing emotional decision-making, creates a strategy that consistently produces superior long-term results for investors who maintain discipline.

The evidence is clear: investors who use systematic DCA approaches through retirement accounts and brokerage platforms significantly outperform those who attempt to time marketEntry and exit points. With the advent of commission-free trading and automated investment platforms, implementing DCA has never been easier or more accessible. Whether you're starting with $50 monthly or managing substantial retirement assets, the principle remains the same: consistent, automated investments over time compound into extraordinary wealth.

The journey to financial independence doesn't require sophisticated market knowledge or extraordinary timing—it requires commitment to a simple, proven system executed consistently over years and decades. Dollar cost averaging provides that system, transforming market uncertainty from a source of anxiety into a strategic advantage that works in your favor regardless of where markets head next. Start today, stay consistent, and let time do the heavy lifting toward your financial goals.