The question of when to start investing has one answer backed by decades of financial research: as soon as possible. While it may seem counterintuitive—particularly when you're just starting your career or managing student debt—the mathematical power of compound interest means that every year you delay costs you significantly in potential wealth accumulation. The difference between starting at age 25 versus age 35 can represent hundreds of thousands of dollars by retirement, even with identical contribution amounts. This isn't speculation; it's arithmetic.

Financial advisors consistently emphasize that time in the market beats timing the market, and the data supports this fundamental principle. Understanding why early investing matters, what barriers prevent people from starting, and how to overcome those obstacles can transform your financial trajectory. The goal of this article is to provide a comprehensive framework for determining when you're ready to begin investing and why waiting—even for what feels like valid reasons—typically costs more than starting now.

The Mathematics of Time: Why Early Investing Matters

Compound interest works by earning returns on your returns, creating exponential growth over time. When you invest money in the stock market, your principal generates earnings, and those earnings then generate their own earnings. This snowball effect accelerates dramatically over decades, making early investment periods disproportionately valuable compared to later ones.

📊 THE COST OF DELAYING INVESTMENTS

| Starting Age | Monthly Investment | Years Invested | Total Contributions | Value at Age 65 (7% return) |

|---|---|---|---|---|

| 25 | $300 | 40 | $144,000 | $745,179 |

| 30 | $300 | 35 | $126,000 | $508,604 |

| 35 | $300 | 30 | $108,000 | $338,449 |

| 40 | $300 | 25 | $90,000 | $219,064 |

| 45 | $300 | 20 | $72,000 | $137,287 |

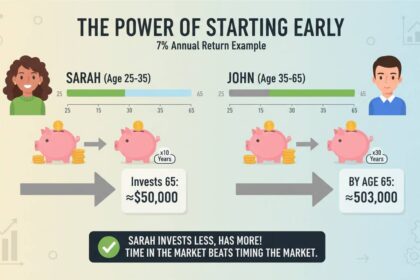

This table illustrates a critical point: the difference between starting at 25 versus 35—waiting just 10 years—results in over $400,000 less at retirement, despite only $18,000 less in total contributions. The cost of waiting compounds annually, making each year of delay increasingly expensive.

Research from J.P. Morgan's Annual Guide to Retirement confirms that investor behavior, particularly starting early, accounts for a significant portion of retirement success. Their analysis shows that a hypothetical $10,000 investment made at age 25 would grow to approximately $76,000 by age 65 at a 7% annual return, but that same $10,000 invested at age 35 would grow to only $38,000—a 50% reduction in final value from a 10-year delay.

Breaking Down the Barriers to Start

Despite the clear mathematical advantages of early investing, many Americans postpone starting. Understanding these barriers is the first step toward overcoming them. The most common reasons people give for not investing include insufficient income, fear of losing money, lack of financial knowledge, and the belief that they need a large sum to begin.

Income and Cash Flow Concerns

Many potential investors believe they need substantial income to begin investing. This misconception prevents millions from starting earlier than necessary. The reality is that most brokerage firms now offer fractional shares and low or no minimum investment accounts, allowing individuals to begin with as little as $5 or $10 per month. Employer-sponsored retirement plans often allow contributions as low as 1% of salary, with many companies matching a percentage of those contributions.

The 2023 Fidelity Investments Investor Insights Study found that 67% of Americans who invest started with amounts under $1,000, and nearly one-third began with less than $500. These figures demonstrate that waiting until you have substantial savings is unnecessary—starting small and increasing contributions over time is both common and effective.

Fear and Risk Perception

Market volatility creates legitimate anxiety for new investors. Watching account balances fluctuate can be unsettling, particularly for those who haven't experienced market cycles. However, this fear often leads to precisely the wrong behavior: selling during downturns and missing subsequent recoveries.

The S&P 500 has delivered positive returns in approximately 75% of all calendar years since 1928, according to data compiled by NYU Stern Professor Aswath Damodaran. While past performance doesn't guarantee future results, this historical context suggests that investors who remain committed through market fluctuations have historically been rewarded. Starting to invest during uncertain times—while uncomfortable—can actually be advantageous because you're purchasing assets at lower prices, positions that benefit when markets eventually recover.

Knowledge and Confidence Gaps

Financial literacy remains a significant barrier, with many Americans feeling unprepared to make investment decisions. However, the proliferation of low-cost index funds, robo-advisors, and educational resources has dramatically lowered the knowledge barrier to entry. You don't need to become an expert in individual stocks, technical analysis, or complex derivatives to build wealth through investing.

Index funds, which pool investor money to track a broad market segment like the S&P 500, provide instant diversification and historically match market returns with minimal effort. For most beginning investors, a simple three-fund portfolio containing U.S. stocks, international stocks, and bonds offers a complete, low-maintenance investment strategy. The rise of robo-advisors like Betterment and Wealthfront has further simplified the process by automatically rebalancing portfolios and optimizing tax efficiency based on individual goals and risk tolerance.

Investment Vehicles: Where to Start

Choosing where to invest depends on your specific circumstances, including income level, employment status, and financial goals. Several account types offer distinct advantages depending on your situation.

Employer-Sponsored Retirement Accounts

401(k) plans, available through employers, represent the most accessible entry point for many workers. These accounts offer tax advantages—traditional 401(k) contributions reduce taxable income now, while Roth contributions allow tax-free growth and withdrawals in retirement. Most significantly, many employers match a portion of employee contributions, effectively providing free money that immediately compounds.

The maximum contribution limit for 401(k) plans in 2024 is $23,000 for those under 50, with catch-up contributions of an additional $7,500 allowed for those 50 and older. Even contributing enough to capture the full employer match—often 3% to 6% of salary—provides immediate returns that dwarf most other investment opportunities.

Individual Retirement Accounts

IRAs offer additional tax-advantaged investing options outside employer plans. Traditional IRAs provide tax-deferred growth with contributions potentially tax-deductible depending on income and workplace plan access. Roth IRAs offer tax-free growth and qualified withdrawals, though contributions are made with after-tax dollars. In 2024, individuals can contribute up to $7,000 to IRAs ($8,000 for those 50 and older).

For those without access to employer-sponsored retirement plans, IRAs represent the primary tax-advantaged investment vehicle. Even those with 401(k) options may benefit from contributing to IRAs as well, as they offer additional space for tax-advantaged growth beyond employer plan limits.

Taxable Brokerage Accounts

Once you've maximized tax-advantaged accounts, taxable brokerage accounts offer flexibility for goals beyond retirement. These accounts don't have contribution limits or withdrawal restrictions, making them ideal for building wealth for intermediate goals like purchasing a home, funding education, or achieving financial independence before traditional retirement age.

Common Investment Mistakes to Avoid

Beginning investors face several pitfalls that can significantly impact long-term returns. Understanding these mistakes helps you avoid them.

❌ WAITING FOR THE "RIGHT TIME"

Market timing—attempting to buy at market bottoms and sell at peaks—is practically impossible for individual investors. Research from the financial analysis firm DALBAR consistently shows that individual investors underperform market benchmarks by significant margins, primarily due to emotional decision-making during volatility. The "right time" to invest is whenever you have money you won't need immediately and a long time horizon.

❌ OVERCONCENTRATING IN INDIVIDUAL STOCKS

While picking winning stocks can generate substantial returns, the risk of permanent capital loss from a few bad investments is significant. Diversification through index funds or ETFs provides broad market exposure while minimizing the impact of any single company's performance on your overall portfolio.

❌ IGNORING EXPENSE RATIOS

Investment costs compound over time, quietly eating into returns. A fund with a 1% annual expense ratio might seem insignificant, but over 30 years, it can reduce your portfolio value by 20% or more compared to a low-cost alternative. Index funds from providers like Vanguard, Fidelity, and Schwab often charge less than 0.10% annually, making cost an insignificant factor in fund selection.

❌ CHANGING STRATEGIES FREQUENTY

Switching investment strategies based on short-term performance or market conditions disrupts the compounding process. Staying invested through market cycles, maintaining consistent contributions, and periodically rebalancing provides better long-term results than constant adjustment.

Building Your Investment Foundation

Starting your investment journey requires several practical steps. First, establish an emergency fund of three to six months of expenses in a high-yield savings account. This prevents the need to sell investments during market downturns to cover unexpected expenses. Second, ensure you're contributing enough to your employer-sponsored retirement plan to capture the full match—this provides an immediate return that outweighs almost any other consideration.

Third, automate your investments through systematic contribution programs. Setting up automatic transfers from your checking account to your investment accounts removes the friction of manual investing and ensures consistent contributions regardless of market conditions. Research from Vanguard indicates that investors who automate their contributions save more consistently and achieve better outcomes than those who invest manually.

Finally, increase your contributions as your income grows. A common guideline is to increase your savings rate by 1% with each salary increase, maintaining your existing lifestyle while accelerating wealth building. This "pay yourself first" approach ensures that investing remains a priority rather than an afterthought.

The Bottom Line: Start Now, Start Small

The evidence is unambiguous: the best time to start investing is as soon as possible, regardless of how much you can contribute initially. The mathematical power of compound interest means that even modest amounts invested early will likely exceed larger amounts invested later. Waiting for ideal market conditions, more income, or greater knowledge almost always costs more than starting now with imperfect information.

Start with whatever amount feels manageable—even $50 or $100 per month. Contribute to tax-advantaged accounts first, particularly to capture employer matches. Maintain a long-term perspective through market fluctuations, and resist the urge to make dramatic changes based on short-term market movements. Your future self will thank you for starting today rather than waiting for circumstances that may never arrive.

Frequently Asked Questions

What's the minimum amount needed to start investing?

You can start investing with very little money. Many brokerage firms offer accounts with no minimum deposit requirements, and fractional shares allow you to purchase portions of expensive stocks or funds with just a few dollars. Some apps even allow investments as small as $1. The key is starting, regardless of amount.

Should I pay off debt before starting to invest?

This depends on the interest rate of your debt. High-interest debt like credit cards should typically be prioritized, as the guaranteed "return" from eliminating that debt exceeds most investment returns. However, low-interest debt (such as student loans below 5% or mortgages) doesn't necessarily require full repayment before investing, especially if your employer offers matching contributions in a 401(k).

Is it safe to invest during economic uncertainty?

Market timing is extremely difficult to execute successfully. Historically, markets have recovered from every downturn, and investors who continued contributing during uncertain periods have been rewarded. If you have a long time horizon (10+ years), investing during uncertain times can actually be advantageous because you're buying assets at lower prices.

How much of my income should I invest?

A common guideline is the 50/30/20 rule: 50% for needs, 30% for wants, and 20% for savings and investments. However, the most important step is capturing any employer 401(k) match, which provides an immediate 50% to 100% return on those contributions. After that, aim to increase your savings rate gradually until you're investing 15% to 20% of your income for retirement.

What's the difference between stocks and bonds for beginners?

Stocks represent ownership in companies and generally offer higher returns over long periods with more volatility. Bonds represent loans to governments or corporations and typically provide lower returns with less fluctuation. For young investors with long time horizons, stock-heavy portfolios are generally recommended, with bonds added as you approach goals like retirement.