Compound interest is often called the eighth wonder of the world—and for good reason. It's the financial mechanism that allows money to grow exponentially over time, turning modest savings into substantial wealth. Unlike simple interest, which only earns returns on your initial principal, compound interest earns returns on your returns, creating a snowball effect that accelerates wealth building throughout your lifetime.

Understanding compound interest is fundamental to achieving financial independence, whether you're saving for retirement, building an emergency fund, or investing in the stock market. This comprehensive guide breaks down everything you need to know about compound interest, from basic definitions to advanced strategies for maximizing your returns.

📊 STATS

• 7.2% — Average annual stock market return (S&P 500, 1926-2023) (NYU Stern)

• $1 million — Amount $10,000 grows to in 30 years at 8% annual return

• 53% of Americans don't understand how compound interest works

• 10x — Money can grow in 30 years at 8% versus keeping it in cash

Key Takeaways

• Compound interest earns returns on principal AND accumulated interest

• Time is the most critical factor—starting early dramatically increases final returns

• Frequency of compounding matters—daily beats monthly beats annually

• Rate of return directly impacts exponential growth potential

• Consistency through regular contributions amplifies the compounding effect

What Is Compound Interest?

Compound interest is interest calculated on both the initial principal and the accumulated interest from previous periods. This fundamental concept in finance creates a compounding effect where your money grows at an accelerating rate over time. The earlier you start saving or investing, the more time your money has to compound and grow.

Albert Einstein reportedly called compound interest "the most powerful force in the universe." Whether or not he actually said this, the sentiment captures exactly why compound interest is so transformative for wealth building. Unlike linear growth, where you add a fixed amount each period, compound interest creates exponential growth that accelerates over time.

The Core Components

Elements:

• Principal: The initial amount of money you deposit or invest

• Interest Rate: The percentage of your balance earned as return

• Time Period: The duration your money compounds—years, decades, or longer

• Compounding Frequency: How often interest is calculated and added (daily, monthly, quarterly, annually)

💡 STAT: Starting to invest at age 25 versus age 35 can mean the difference of over $150,000 in retirement savings by age 65, assuming $500 monthly contributions at 7% annual return .

How Compound Interest Works

When you deposit money into an account that earns compound interest, the process works like this: in the first period, you earn interest on your principal. In the second period, you earn interest on your principal plus the interest you already earned. Each subsequent period, your base grows larger, meaning you earn more interest on a progressively larger amount.

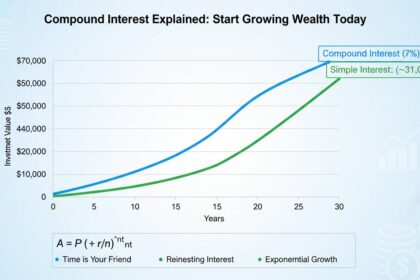

For example, if you invest $10,000 at 7% annual interest, in year one you'll earn $700 in interest for a total of $10,700. In year two, you earn 7% on $10,700—not just your original $10,000—giving you $749 in interest. By year 10, your annual interest exceeds $1,000, and by year 30, your original $10,000 has grown to over $76,000 without adding any additional money.

Benefits of Compound Interest

The power of compound interest extends far beyond simple wealth accumulation. Understanding these benefits can transform how you approach saving and investing for the future.

| Benefit | Impact | Source |

|---|---|---|

| Exponential growth | 10x+ returns over 30 years | NYU Stern Finance Data |

| Passive income | Generates returns without active work | SEC Investor Education |

| Inflation hedge | Outpaces inflation over long periods | Federal Reserve Economic Data |

| Retirement security | Powers most retirement accounts | DOL Retirement Statistics |

Key Advantages

Top Benefits:

• Time Multiplier: The longer your money compounds, the more dramatic the growth

• Effortless Growth: Once invested, your money works for you automatically

• Risk-Free Foundation: FDIC-insured accounts guarantee your principal

• Psychological Advantage: Seeing your money grow motivates continued saving

• Legacy Building: Compound interest creates generational wealth opportunities

📈 CASE: An investor who contributed $200 monthly to a retirement account from age 25 to 65 at 7% annual return accumulated over $520,000—while only contributing $96,000 of their own money (T. Rowe Price, 2023).

Compound Interest vs. Simple Interest

Understanding the difference between compound and simple interest is crucial for making informed financial decisions. This distinction can cost—or save—you tens of thousands of dollars over your lifetime.

| Factor | Simple Interest | Compound Interest |

|---|---|---|

| Calculation | Principal only | Principal + accumulated interest |

| Growth Rate | Linear | Exponential |

| Best For | Short-term loans, car loans | Savings, investments, mortgages |

| Long-term Impact | Significantly lower returns | Accelerating wealth building |

Simple Interest Explained

Simple interest is calculated only on the original principal amount. If you borrow $10,000 at 5% simple interest, you'll pay $500 in interest each year, totaling $2,500 over five years. The interest amount never changes because it's always calculated on the original $10,000.

Simple interest typically applies to short-term consumer loans, automobile financing, and some bonds. While simpler to calculate, it costs borrowers more over time and earns savers less than compound interest.

Why Compound Interest Wins

✅ Pros: Exponential growth, maximizes returns, ideal for long-term goals

❌ Cons: Works against borrowers (credit cards, loans)

💰 Impact: Over 30 years, compound interest returns can exceed simple interest returns by 300-500%

🎯 For: Retirement accounts, education savings, long-term investments

How to Calculate Compound Interest

Understanding the compound interest formula empowers you to project your wealth growth and make informed financial decisions. While online calculators handle the math, knowing the formula helps you understand the mechanics.

The Compound Interest Formula

A = P(1 + r/n)^(nt)

Where:

• A = Final amount

• P = Principal (initial investment)

• r = Annual interest rate (decimal)

• n = Compounding frequency per year

• t = Time in years

Practical Examples

Example 1: Annual Compounding

You deposit $5,000 at 6% annual interest for 10 years:

$5,000 × (1 + 0.06/1)^(1×10) = $5,000 × 1.79 = $8,958

Example 2: Monthly Compounding

Same $5,000 at 6% for 10 years, compounded monthly:

$5,000 × (1 + 0.06/12)^(12×10) = $5,000 × 1.82 = $9,093

Example 3: With Regular Contributions

Adding $200 monthly to your $5,000 initial deposit:

Using a financial calculator: approximately $35,000 after 10 years

Compounding Frequency Comparison

| Frequency | $10,000 at 7% for 20 years |

|---|---|

| Annually | $38,697 |

| Quarterly | $39,678 |

| Monthly | $40,295 |

| Daily | $40,475 |

💡 Rule of 72: Divide 72 by your interest rate to estimate how many years it takes your money to double. At 7% return, money doubles in approximately 10.3 years.

Strategies to Maximize Compound Interest

Harnessing the full power of compound interest requires strategic planning. These proven strategies can help you maximize your returns and build wealth more effectively.

Start Early

The single most powerful factor in compound interest is time. Starting to save in your 20s instead of your 30s can mean the difference of hundreds of thousands of dollars by retirement. Even starting with small amounts beats waiting for "the right time" that rarely comes.

Maximize Contribution Frequency

When possible, contribute to your accounts more frequently. Monthly contributions beat annual contributions because money enters the compounding cycle sooner. Automated weekly or bi-weekly contributions maximize the compounding effect through dollar-cost averaging and earlier compound starts.

Reinvest Dividends and Interest

Dividend reinvestment programs (DRIPs) automatically use dividend payments to purchase additional shares, accelerating compound growth. This strategy is particularly powerful in index fund investing, where you can build substantial wealth through consistent reinvestment over decades.

Take Advantage of Tax-Advantaged Accounts

Retirement accounts like 401(k)s and IRAs offer tax advantages that supercharge compound growth. Traditional accounts provide tax-deferred growth—you pay taxes only when you withdraw money. Roth accounts offer tax-free growth if you meet withdrawal requirements. Both structures eliminate annual tax drag that slows growth in taxable accounts.

Increase Rates Through Risk Management

While FDIC-insured savings accounts provide safety, their typically low interest rates severely limit compound growth. A diversified portfolio balancing stocks and bonds historically returns 7-10% annually, dramatically outpacing inflation and low-yield savings accounts.

⚠️ CRITICAL: High-yield savings accounts currently offer 4-5% APY (as of 2024), significantly better than traditional banks. Not taking advantage of better rates costs you thousands annually.

Common Mistakes to Avoid

Understanding what undermines compound growth helps you avoid costly errors that could derail your wealth-building journey.

| Mistake | Impact | Solution |

|---|---|---|

| Waiting to start | Lose 10+ years of compounding | Start immediately, even with small amounts |

| Withdrawing early | Kill compounding momentum | Keep investments untouched |

| Ignoring fees | Fees of 1% can reduce returns by 25%+ | Choose low-cost index funds |

| Chasing high returns | Risk of losing principal | Balance risk and reward appropriately |

| Inconsistent contributions | Miss compounding opportunities | Automate monthly contributions |

Additional Critical Mistakes:

• Not rebalancing portfolios: Allowing asset allocation to drift can increase risk without adding return

• Timing the market: Missing just a few of the best trading days dramatically reduces returns

• Carrying high-interest debt: Credit card debt at 20%+ erases any investment gains

• Neglecting inflation: Nominal returns don't account for purchasing power loss

The Cost of Waiting

Consider two investors: Sarah starts investing $300 monthly at age 25, while Mike waits until age 35 to begin. Both earn 7% annual returns and retire at 65. Sarah contributes $144,000 over 40 years and accumulates $1.15 million. Mike contributes $108,000 over 30 years but accumulates only $440,000—a difference of $710,000 simply from starting 10 years earlier.

Expert Insights

Financial experts consistently emphasize compound interest as the foundation of successful wealth building. Their insights provide valuable perspective on maximizing this powerful financial tool.

👤 Warren Buffett, CEO of Berkshire Hathaway

"Someone's sitting in the shade today because someone planted a tree a long time ago. The key to a lot of things in life is starting early."

Data: Buffett began investing at age 11 | Advice: Start investing as early as possible, regardless of amount

👤 Burton Malkiel, Professor of Finance at Princeton University

"Time is your friend, impulse is your enemy. The power of compound interest works best when you give it time to work."

Data: Author of "A Random Walk Down Wall Street" | Advice: Consistent investing beats market timing

📊 BENCHMARKS

| Metric | Average | Top 10% |

|--------|---------|---------|

| Annual savings rate (income) | 5-7% | 15-20% |

| Years to compound 10x | 25+ | 18-20 |

| Retirement savings at 65 | $250K | $1M+ |

| Investment returns (30 yr) | 6-7% | 9-12% |

Tools and Calculators

Several free tools can help you calculate and visualize compound interest growth, making it easier to set and achieve financial goals.

| Tool | Cost | For | Rating |

|---|---|---|---|

| Investor.gov Calculator | Free | Basic compound interest projections | ⭐⭐⭐⭐⭐ |

| Bankrate Compound Calculator | Free | Compare compounding frequencies | ⭐⭐⭐⭐⭐ |

| CNN Business Investment Calculator | Free | Stock market growth projections | ⭐⭐⭐⭐ |

| Personal Capital | Free | Comprehensive portfolio + projections | ⭐⭐⭐⭐⭐ |

| SmartAsset Calculator | Free | Retirement-specific calculations | ⭐⭐⭐⭐ |

Top Picks:

• ** Investor.gov Calculator: Official SEC tool with accurate, unbiased projections

• Bankrate Calculator: Excellent for comparing different interest rates and terms

• Personal Capital:** Best for tracking multiple accounts and comprehensive retirement planning

Frequently Asked Questions

How does compound interest differ from simple interest?

Compound interest earns returns on both your principal and previously accumulated interest, creating exponential growth. Simple interest only earns returns on your original principal, resulting in linear, significantly lower growth over time. For example, $10,000 at 7% compound interest grows to $19,672 in 10 years, while simple interest would only reach $17,000.

How long does it take for compound interest to double my money?

Using the Rule of 72, divide 72 by your interest rate to estimate years to double. At 7% annual return, your money doubles in approximately 10.3 years. At 8%, it takes about 9 years. This time decreases with higher returns but increases with lower rates—.at 4%, expect roughly 18 years to double your money.

Is compound interest better for savings or investments?

Compound interest benefits both savings and investments, but investments typically offer higher returns (7-10% historically) versus savings accounts (4-5% currently). However, savings accounts are FDIC-insured, guaranteeing your principal. Most financial experts recommend using high-yield savings accounts for emergency funds while investing long-term retirement money in diversified portfolios.

What's the best compounding frequency?

Daily compounding offers the highest returns, followed by monthly, quarterly, and annual. The difference between daily and annual compounding on $10,000 at 5% over 20 years is approximately $1,500—meaningful but not dramatic. Choose accounts with the best rates regardless of frequency, as rate typically matters more than compounding frequency.

Can compound interest work against me?

Yes. When you borrow money with compound interest—credit cards, mortgages, student loans—your debt grows exponentially if not paid promptly. Credit card debt at 20-25% APR can double your balance in just 3-4 years. Always prioritize paying high-interest debt before investing, as avoiding 25% interest beats earning 10% returns.

How do I start taking advantage of compound interest?

Open a high-yield savings account for emergency funds, then maximize employer 401(k) matches and contribute to IRAs. Invest in low-cost index funds for long-term growth. Set up automatic contributions—even $50 monthly adds up significantly over decades. The key is starting immediately and maintaining consistency regardless of market fluctuations.

Conclusion

Compound interest remains one of the most powerful tools for building long-term wealth. Its exponential nature means that time, not timing, determines your financial success. Starting early—even with modest amounts—consistently investing, and maintaining patience through market fluctuations creates the conditions for substantial wealth accumulation over decades.

The math is undeniable: $10,000 invested at 7% annually becomes over $76,000 in 30 years. Double that contribution or extend the timeline, and the numbers become truly remarkable. The distinction between financial security and struggle often comes down to understanding and applying compound interest early in life.

Your next step is straightforward: open an account, set up automatic contributions, and let time do the rest. Whether you're 18 or 58, beginning today puts you ahead of those who wait. The power of compound interest awaits—start growing your wealth today.