In today's volatile markets, investors are always looking for strategies that build wealth over time without requiring perfect timing or a finance degree. Dollar cost investing—also called dollar cost averaging or DCA—has become one of the most common approaches for people who want to participate in the financial markets without the stress of guessing when to buy or sell. This method takes most of the emotion out of investing and gives you a systematic way to put money into assets regardless of whether the market is up or down. If you're an experienced investor or just starting out, understanding how this strategy works could make a real difference in your financial future.

Understanding Dollar Cost Investing

Dollar cost investing means putting a fixed amount of money into the market at regular intervals—say, $200 every month—no matter what's happening with prices. Instead of trying to time the market by buying low and selling high, you simply stick to your schedule. You might buy shares of a stock, an index fund, or an ETF on the same day each month, rain or shine.

Here's why this works: when prices are high, your fixed amount buys fewer shares. When prices are low, the same amount buys more shares. Over time, this naturally brings down your average cost per share. It's a way of smoothing out the bumps without having to predict what the market will do next.

This is different from lump sum investing, where you throw a big chunk of money into the market all at once, hoping you've picked a good time.

Vanguard's research suggests dollar cost investing has performed about as well as—or sometimes better than—trying to time the market. That makes sense: markets tend to reward patience and consistency over speculation. The strategy became really popular during the 20th century as 401(k) plans and similar retirement accounts spread, giving workers an easy way to invest a little from each paycheck.

How Dollar Cost Investing Works

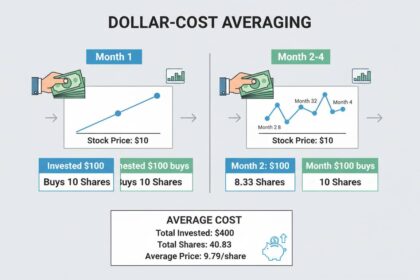

The mechanics are simple but effective. Say you invest $500 monthly into an index fund. In month one, if shares cost $50 each, your $500 buys 10 shares. In month two, if the price drops to $40, your $500 buys 12.5 shares. In month three, if the price jumps to $60, you only get about 8.33 shares.

What happens over time is that your average cost per share ends up lower than the simple average of the share prices—because you automatically bought more when things were cheap. This effect builds up over years or decades, which is exactly how most people approach retirement savings.

Most brokerages make this easy to set up. You can schedule automatic recurring contributions that happen on autopilot, so you never have to think about it or stress over when to buy. This also keeps you from making emotional decisions when the market swings.

If you have a 401(k), you're probably already doing this without even realizing it. Your contributions come out of your paycheck automatically and get invested according to your choices. IRAs work the same way—you can set up automatic transfers and forget about them.

Benefits of Dollar Cost Investing

The biggest perk isn't just the math—it's the peace of mind. Trying to time the market means predicting the future, and even professionals can't do that consistently. With dollar cost investing, you skip all that stress. You just invest on schedule and let the strategy do its work.

The strategy also turns market volatility into an advantage instead of a threat. When prices drop, you're automatically buying more shares. When the market recovers, your extra shares mean your portfolio bounces back faster. You're essentially "buying the dip" without having to summon the courage to invest when everyone else is scared.

Another big advantage is how accessible it is. You don't need thousands of dollars to get started. Many platforms let you begin with just a few dollars per month. Starting early—even with small amounts—can make a huge difference over time thanks to compound growth. Someone who starts investing at 25 versus 35 could end up with hundreds of thousands of dollars more by retirement, just from that extra decade of compounding.

There's also a tax angle. When you use dollar cost investing inside tax-advantaged accounts like IRAs or 401(k)s, your money grows tax-deferred or tax-free, which makes the strategy even more powerful over the long haul.

Potential Drawbacks to Consider

Dollar cost investing isn't perfect for every situation. One common criticism is that it can underperform during long bull markets. When prices keep climbing for years—as they did for much of the 2010s—investing a lump sum upfront would have given you better returns, since your money had more time to grow.

Transaction costs can add up too, especially if your brokerage charges per trade. Even small fees, repeated monthly for decades, become meaningful. The good news is most major platforms now offer commission-free trading, so this is less of an issue than it used to be.

There's also an opportunity cost to consider. If you're holding cash while slowly drip-feeding it into the market, you might be missing out on better returns elsewhere—especially when interest rates are high. More advanced investors sometimes keep a balance between dollar cost investing and holding liquid cash for opportunities that pop up.

Finally, this strategy requires discipline. If you start contributing regularly but then panic and stop during a downturn, you lose the main benefit. You have to be able to keep going when your account balance is shrinking, which is harder than it sounds.

Dollar Cost Investing vs. Lump Sum Investing

This is one of the most common debates in personal finance. Lump sum means investing everything you have right now, not spreading it out. The argument for lump sum is that markets generally go up over time, so the sooner your money is in, the more it can grow. Studies suggest lump sum beats dollar cost averaging about two-thirds of the time.

But there's a catch: those studies usually assume you already have a big pile of cash to invest. Most people don't—they earn money gradually through their jobs. Also, the studies often ignore how emotionally difficult it is to pick the "wrong" time to invest. The stress and regret from bad timing can mess with your decisions long-term.

For most people, a hybrid approach makes sense. If you get a windfall—inheritance, bonus, proceeds from selling a house—you could dollar cost that money over 12 to 24 months instead of investing it all at once. That gives you some protection from bad timing while still getting most of your money invested fairly quickly.

The right choice depends on your situation: how much money you have, how stable your income is, and how comfortable you are with risk.

Getting Started with Dollar Cost Investing

Getting started is straightforward. First, open an account with a brokerage that offers low-cost index funds or ETFs and has automatic investment features. Fidelity, Schwab, Vanguard, and Robinhood all work, each with different strengths.

Next, decide how much to contribute and how often. The exact amount matters less than consistency. Whether it's $50 a month or $500, just pick something realistic and stick with it. Many advisors suggest contributing enough to get your full 401(k) match first, then increasing from there as your income grows.

Think about your asset allocation too. Spreading your money across stocks, bonds, and some international exposure helps manage risk. Target-date funds are a simple option—they automatically adjust your mix as you get closer to retirement. Or you can build your own portfolio with a few low-cost index funds.

Finally, commit to ignoring the day-to-day noise. Check your portfolio once a year, not daily. The real payoff comes decades from now, not next month. If you can stay the course through crashes and booms, dollar cost investing can be a reliable way to build long-term wealth.

Conclusion

Dollar cost investing is one of the simplest, most proven ways to build wealth over time. By investing fixed amounts regularly, you remove emotional decision-making from the equation and let market volatility work for you. It's not always the highest-returning strategy in every environment, but the consistency and psychological benefits make it especially valuable for people building wealth gradually through their careers.

The fact that it matches how most people earn money—regular paychecks—makes it a natural fit for retirement savings. Whether through an employer plan or a personal brokerage account, dollar cost investing offers a path to financial security that doesn't require you to be a market expert or have a huge pile of cash upfront. For those willing to stay consistent over decades, this approach has helped millions of Americans reach their financial goals.

Frequently Asked Questions

Is dollar cost investing only suitable for retirement accounts?

No. You can use it in any investment account—taxable brokerages, IRAs, 401(k)s, 529 plans. The mechanics are the same everywhere, though tax-advantaged accounts give you an extra boost since your gains aren't taxed each year.

How much money do I need to start?

The barrier to entry is low. Many platforms let you start with just $1 per automatic investment. There's no minimum balance required to begin building wealth through consistent contributions.

Does dollar cost investing guarantee profits?

No investment guarantees profits. Dollar cost investing typically performs well over long periods and reduces the impact of market swings, but all investments carry risk. Markets go down sometimes, and past performance doesn't predict future results.

How long should I continue dollar cost investing?

This strategy is designed for the long haul—think decades, not months. It works best when you keep contributing through multiple market cycles. Stopping during downturns defeats the whole purpose, since that's when you're buying shares at the lowest prices.

Can I combine dollar cost investing with other strategies?

Definitely. Many investors use dollar cost investing as their base approach but stay flexible for other opportunities. A hybrid strategy lets you benefit from consistent long-term accumulation while keeping some cash available for when something special comes up.

What happens if I stop contributing during a market downturn?

That essentially kills the strategy's main advantage. The whole point is buying more shares when prices are low, which speeds up your recovery when markets turn around. Pausing contributions means missing those buying opportunities and can significantly hurt your long-term returns.