Investors looking for a disciplined way to build wealth often hear about dollar cost averaging. This investment approach has become more popular recently as market swings have made both new and experienced investors think twice about how they put money to work. Understanding what dollar cost averaging means, along with its pros and cons, can help you decide whether it fits your financial plans.

Understanding Dollar Cost Averaging

Dollar cost averaging means investing a fixed amount of money at regular intervals, no matter what's happening in the market. Instead of trying to buy shares at the "perfect" moment, you keep buying regardless of whether prices are up or down. When prices drop, your fixed amount buys more shares. When prices rise, it buys fewer. Over time, this usually results in a lower average cost per share than trying to time the market.

Financial advisors started promoting this approach during the mid-20th century as a way to help regular people invest in the stock market without needing deep expertise or a lot of money upfront. The typical setup involves automatic contributions from a paycheck or bank account into a diversified portfolio, usually monthly. Set it up once and let it run—that's the basic idea.

Research from financial institutions has shown that dollar cost averaging works well when markets bounce around. When stock prices swing significantly, your fixed purchases grab varying amounts of shares, which smooths out how those highs and lows affect your portfolio. This appeals to investors who get nervous during downturns or who prefer a more cautious approach to stocks.

How Dollar Cost Averaging Works

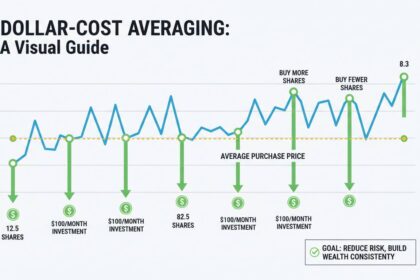

The mechanics are simple. You decide on a fixed dollar amount to invest regularly—say, $500 every month. You keep buying shares at those intervals regardless of whether the market is climbing or falling. Over time, you accumulate shares at different prices, creating an average cost basis that usually beats trying to guess when to jump in.

Here's a practical example. Say you commit to investing $1,000 in a particular stock each month for six months. In month one, the stock trades at $50, so your $1,000 buys 20 shares. In month two, the price drops to $40, and your $1,000 buys 25 shares. In month three, prices climb to $80, so you only get 12.5 shares. By the end of six months, your average cost per share comes in lower than simply averaging the six monthly prices.

Most brokerages now let you set up automatic purchases without lifting a finger. You can schedule recurring buys of individual stocks, ETFs, or index funds. Many retirement accounts—401(k)s and IRAs—work the same way, which is why dollar cost averaging has become a staple of retirement planning for millions of people.

Benefits of Dollar Cost Averaging

The main advantage is that it removes the temptation to time the market. Even professionals can't consistently predict where prices are heading, so trying to buy at the "right" moment usually backfires. With dollar cost averaging, you sidestep the emotional traps of FOMO buying at peaks and panic selling at bottoms.

The discipline it creates matters too. Because purchases happen automatically, you keep investing whether the market looks great or terrible. This consistency prevents you from derailing your long-term plan based on short-term moves. Research has shown that investors who make sporadic, emotion-driven decisions often end up doing worse than those who stick to a systematic approach.

You also don't need much money to start. Unlike lump sum investing, which requires a big pile of cash upfront, dollar cost averaging lets you begin with modest monthly contributions. Over years, compound growth turns those regular contributions into meaningful portfolios. Patience pays off.

Another benefit is natural diversification through time. Rather than putting all your money in at once, you spread purchases across different market conditions and price levels. This temporal diversification cuts down on the risk of badly timed entries and gives you a more balanced average purchase price.

Potential Drawbacks to Consider

Dollar cost averaging isn't perfect. One issue is opportunity cost when markets keep climbing. If stocks rise steadily over years, you'll be buying at progressively higher prices, which can mean lower returns than investing a lump sum early.

Transaction costs matter too, especially if your brokerage charges per trade. While many platforms now offer commission-free trading, some still do, and those fees add up over dozens of small purchases. Check your brokerage's fee structure before setting up a dollar cost averaging plan.

The strategy also requires real patience. It's a long-term game, and bailing out during extended downturns can leave you with losses or missing out on recoveries. Keeping your hands off during bear markets is harder than it sounds—even when staying the course would work out fine.

And dollar cost averaging doesn't guarantee profits or protect against losses in a falling market. It lowers your average cost during volatility, but if your investments keep dropping for years, you can still lose money. Proper asset allocation and diversification still matter.

Dollar Cost Averaging vs. Lump Sum Investing

This is one of the most common debates in investing. Lump sum means putting all your money in at once, right away, so your entire portfolio starts earning returns immediately. In a rising market, this usually beats dollar cost averaging because more money gets to work sooner.

Research from financial institutions suggests lump sum investing tends to outperform over the long run, mainly because stocks have historically gone up over time. But that historical edge doesn't account for how hard it feels psychologically to dump a big chunk of money into the market.

Your choice depends on your situation and risk tolerance. If you come into a large sum—inheritance, sale of property, bonus—you have to decide whether to deploy it all at once or gradually. If you have strong feelings about market timing, or if you'd lose sleep worrying about a lump sum investment, dollar cost averaging might feel better even if it costs some expected returns.

Most financial planners suggest avoiding market timing altogether. Instead, think about how much volatility you can handle, whether you need returns early, and how well you'll sleep during downturns when choosing between these approaches.

Implementing a Dollar Cost Averaging Strategy

Start by figuring out your goals and how much you can afford to invest regularly. Look at your monthly budget, existing bills, and emergency savings first. Most advisors suggest keeping three to six months of expenses in an accessible savings account before putting money into stocks.

Pick your investments next. Index funds and ETFs give you instant diversification, which is why they're popular for dollar cost averaging. You get broad market exposure without researching individual companies. If you prefer picking your own stocks, stick with financially stable companies that have solid fundamentals—this reduces the risk of permanent losses.

Automating contributions is the key to staying consistent. Most brokerages let you schedule purchases so they happen on autopilot. Set up automatic transfers from your checking account, and your investments keep going whether you're busy, distracted, or tempted to skip a month.

Review your portfolio periodically even with a systematic approach. Your contribution amounts should evolve as your income changes. Check whether your asset allocation still matches your goals. Rebalance annually to keep your risk level where you want it.

Expert Insights on DCA

Financial professionals generally regard dollar cost averaging as a solid tool for long-term wealth building. Research from major financial institutions shows that investors who keep contributing consistently through market cycles tend to outperform those who try to time entry and exit points. The discipline of systematic investing removes the emotional decisions that usually hurt results.

Certified Financial Planner professionals often recommend dollar cost averaging to clients who feel anxious about market swings. It provides a structure that prevents reactive choices during stressful periods. Once you set up predetermined amounts and schedules, the habit builds over years into real portfolio growth.

Retirement planning specialists emphasize consistent contributions to employer-sponsored accounts. The auto-enrollment features in modern 401(k) plans essentially use dollar cost averaging, helping employees save for retirement without needing to understand investing. This workplace setup has brought the strategy to millions of workers.

Conclusion

Dollar cost averaging works as a proven way to build wealth through steady, disciplined investing. By buying shares at regular intervals no matter what the market does, you can lower your average cost per share while avoiding emotional mistakes. It may not always beat lump sum investing in rising markets, but its simplicity, accessibility, and psychological benefits make it a good fit for many people.

The key is sticking with it. Investors who maintain their contribution schedules through market ups and downs—and resist the urge to quit during downturns—set themselves up for long-term success. Pair it with proper asset allocation, diversified investments, and occasional portfolio check-ins, and dollar cost averaging can form the foundation for reaching your financial goals.

Frequently Asked Questions

What is dollar cost averaging in stocks?

Dollar cost averaging is an investment strategy where you invest a fixed amount of money at regular intervals, such as monthly, regardless of market conditions. This approach automatically buys more shares when prices are low and fewer shares when prices are high, potentially lowering your average cost per share over time.

Does dollar cost averaging guarantee profits?

No, dollar cost averaging does not guarantee profits or protect against losses. While it can reduce average costs during volatile periods, you can still lose money if your investments decline persistently. The strategy is designed to minimize timing risks rather than eliminate investment risk entirely.

How often should I make dollar cost averaging investments?

Most investors choose monthly contributions, which aligns well with pay schedules. However, weekly, bi-weekly, or quarterly intervals also work. Pick whatever matches your cash flow and preferences.

Is dollar cost averaging better than lump sum investing?

Not necessarily. Research generally shows that lump sum investing outperforms dollar cost averaging in consistently rising markets because your money begins working sooner. However, dollar cost averaging offers psychological benefits and reduces the risk of poor timing, making it preferable for investors who struggle with market volatility.

How much money do I need to start dollar cost averaging?

You can begin with relatively small amounts. Many brokerages let you start with as little as $1 per share or have no minimum investment requirements for certain funds. Consistency matters more than the initial amount.

Can I use dollar cost averaging with any type of investment?

Yes, dollar cost averaging works with individual stocks, mutual funds, exchange-traded funds, and index funds. The strategy is particularly effective with diversified investments that provide broad market exposure, as this reduces company-specific risks while capturing overall market growth over time.