Blockchain technology has emerged as one of the most transformative innovations of the digital age, fundamentally changing how we think about data storage, security, and transactions. Originally developed as the underlying technology for cryptocurrencies like Bitcoin, blockchain has evolved into a versatile solution with applications spanning finance, healthcare, supply chain management, and beyond. Understanding what blockchain technology is and how it works becomes increasingly important for businesses, developers, and everyday users navigating our increasingly digital world. This comprehensive guide explores the fundamental concepts behind blockchain, examines its technical mechanisms, and highlights its real-world applications and implications for the future.

Understanding the Basics of Blockchain

At its core, blockchain is a distributed ledger technology that records transactions across multiple computers in a way that makes the records extremely difficult to alter retroactively. The term "blockchain" derives from its structural nature: data is stored in blocks that are chained together chronologically, creating an immutable and transparent record of all transactions. Each block contains three key elements: data, a hash of the block, and the hash of the previous block. The hash functions as a digital fingerprint, while the connection to the previous block creates the "chain" that ensures security and integrity.

Unlike traditional databases managed by a single central authority, blockchain operates on a decentralized network of computers called nodes. This decentralization eliminates the need for intermediaries like banks or governments to verify transactions, instead relying on cryptographic algorithms and consensus mechanisms to maintain trust among participants. According to the blockchain analytics firm Chainalysis, over 100 million people worldwide use cryptocurrency wallets, demonstrating the growing adoption of blockchain-based systems.

The concept was first introduced in 2008 by an individual or group using the pseudonym Satoshi Nakamoto, who published the Bitcoin whitepaper describing a "peer-to-peer electronic cash system." Since then, blockchain technology has expanded far beyond cryptocurrency, with enterprises and governments exploring its potential for various applications. The global blockchain market is projected to reach $1.2 trillion by 2030, according to estimates from market research firms, highlighting the significant economic impact this technology continues to generate.

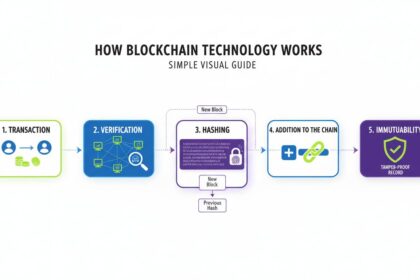

How Blockchain Technology Works

The functioning of blockchain can be broken down into several interconnected processes that work together to create a secure and transparent system. Understanding these mechanisms provides insight into why blockchain is considered revolutionary for digital transactions and data management.

Transaction Initiation and Validation

When a user initiates a transaction on a blockchain network, whether sending cryptocurrency, recording data, or executing a smart contract, the transaction is broadcast to the network of nodes. Each node receives the transaction and verifies its validity by checking cryptographic signatures and ensuring the sender has sufficient resources. This validation process varies depending on the blockchain's consensus mechanism, but it fundamentally ensures that only legitimate transactions are added to the ledger.

In proof-of-work systems like Bitcoin, miners compete to solve complex mathematical puzzles to validate transactions and create new blocks. This energy-intensive process secures the network by making it computationally expensive to attack. Alternatively, proof-of-stake systems like Ethereum, which completed its major upgrade in 2022, select validators based on the amount of cryptocurrency they hold and are willing to "stake" as collateral. These mechanisms represent different approaches to achieving consensus in a decentralized network, each with its own trade-offs regarding security, scalability, and energy consumption.

Block Creation and Chain Addition

Once transactions are validated, they are grouped together into a candidate block. The mining or validation process then produces a unique cryptographic hash for this block, which becomes part of the blockchain's permanent record. In proof-of-work systems, finding this hash requires significant computational effort, while proof-of-stake systems assign the right to create blocks to randomly selected validators.

When a block is successfully created and added to the chain, it becomes visible to all participants in the network. Each node maintains a complete copy of the blockchain, ensuring transparency and redundancy. If any single node attempts to alter historical records, the hash of the affected block would change, breaking the chain connection and alerting the network to the tampering attempt. This immutability represents one of blockchain's most valuable properties for applications requiring permanent and tamper-proof records.

Smart Contracts and Programmable Blockchain

Beyond simple transaction recording, modern blockchain platforms support "smart contracts," which are self-executing programs stored on the blockchain that automatically enforce predefined rules when specific conditions are met. Ethereum, launched in 2015, pioneered this functionality and remains the dominant platform for decentralized applications and smart contract development.

Smart contracts enable a wide range of automated processes, from decentralized finance applications that facilitate lending and trading without traditional banks to supply chain systems that automatically verify product authenticity and track movement. According to data from DappRadar, decentralized applications processed over $100 billion in transactions during 2022, demonstrating the growing economic activity powered by smart contracts. These programmable elements transform blockchain from a simple ledger into a versatile computational platform capable of automating complex business logic.

Types of Blockchain Networks

Not all blockchains operate identically, and understanding the different types helps contextualize their various applications and limitations. The distinction between public, private, and consortium blockchains represents fundamental choices about accessibility, control, and decentralization.

Public blockchains, such as Bitcoin and Ethereum, are completely open networks where anyone can participate by running node software, validating transactions, or mining blocks. These networks offer maximum decentralization and security through broad participation but often face challenges with scalability and transaction speed. Private blockchains, conversely, restrict participation to invited members, offering faster transactions and greater control for enterprise users but sacrificing the decentralization that characterizes public networks.

Consortium blockchains represent a middle ground, where multiple organizations share governance responsibilities and validate transactions. These networks are particularly popular in enterprise applications where multiple stakeholders need to share data and coordinate processes while maintaining some degree of decentralization. Major companies including IBM, Walmart, and Maersk have developed consortium blockchain solutions for supply chain management, financial services, and trade logistics, demonstrating the practical enterprise adoption of this technology.

Real-World Applications and Use Cases

Blockchain technology finds application across numerous industries, with use cases ranging from financial services to healthcare, entertainment, and government operations. These implementations demonstrate both the versatility of blockchain and the challenges of adoption at scale.

In financial services, blockchain enables faster and cheaper cross-border payments, with companies like Ripple processing millions of transactions daily for banks and payment providers. The World Bank estimates that remittances cost an average of 6.8% globally, highlighting the potential for blockchain to reduce friction and expenses in international money transfers. Decentralized finance platforms also challenge traditional banking by offering lending, borrowing, and trading services without intermediaries, though regulatory uncertainty remains a significant factor for growth.

Supply chain management represents another major application area, where blockchain's ability to create transparent and immutable records helps verify product origins, ensure ethical sourcing, and prevent fraud. Walmart's implementation of blockchain for food traceability reduced the time needed to track produce from days to seconds, demonstrating tangible efficiency gains. Similarly, luxury goods manufacturers use blockchain to authenticate products and combat counterfeiting, while pharmaceutical companies explore the technology for drug supply chain verification.

Healthcare organizations leverage blockchain to securely share patient data across providers while maintaining privacy and data integrity. The ability to create unified, tamper-proof medical records improves care coordination and reduces administrative costs. Government agencies in various countries are also experimenting with blockchain for land registries, voting systems, and identity management, though widespread implementation remains limited by technical and regulatory challenges.

Benefits and Challenges of Blockchain Technology

Blockchain offers several compelling advantages over traditional data management systems, but it also presents significant challenges that affect adoption and implementation. A balanced understanding of both aspects helps stakeholders make informed decisions about incorporating blockchain into their operations.

The primary benefits include enhanced security through cryptographic protection and decentralization, increased transparency as all participants can view transaction history, improved efficiency by eliminating intermediaries and automating processes, and reduced costs through peer-to-peer transactions. Blockchain also enables new business models and revenue streams, particularly in digital asset management and decentralized applications.

However, scalability remains a fundamental challenge, as public blockchains often process far fewer transactions per second than traditional payment networks. Bitcoin handles approximately 7 transactions per second, while Visa processes thousands. Energy consumption, particularly in proof-of-work systems, raises environmental concerns that have prompted shifts toward more sustainable alternatives. Regulatory uncertainty also creates risks, as governments worldwide grapple with how to classify and regulate blockchain-based assets and applications. Additionally, user experience challenges and the complexity of managing cryptographic keys have hindered mainstream adoption.

The Future of Blockchain Technology

The trajectory of blockchain technology points toward continued evolution and increasing integration into everyday digital infrastructure. Ongoing research and development address current limitations while expanding capabilities, with layer-2 solutions, interoperability protocols, and energy-efficient consensus mechanisms representing key areas of progress.

Major technology companies and governments are investing heavily in blockchain capabilities, with the United States, European Union, and China all launching initiatives to develop national blockchain strategies. Enterprise adoption continues to accelerate, with over 80% of executives surveyed by Deloitte in 2023 indicating that blockchain integration would likely reach mainstream adoption within a decade.

The convergence of blockchain with other emerging technologies like artificial intelligence and the Internet of Things creates new possibilities for automated, secure, and transparent digital ecosystems. As standards mature and regulatory frameworks develop, blockchain is poised to become a foundational component of digital infrastructure, transforming how individuals and organizations transact, share data, and establish trust in an increasingly connected world.

Frequently Asked Questions

What is blockchain technology in simple terms?

Blockchain technology is a distributed digital ledger that records transactions across many computers in a way that makes the records nearly impossible to change retroactively. Think of it as a shared, transparent notebook where everyone can see what's written, but no one can erase or alter previous entries without detection.

How does a blockchain transaction work?

When someone initiates a transaction, it gets broadcast to a network of computers called nodes. These nodes verify the transaction using cryptographic algorithms. Once verified, the transaction is grouped with other transactions into a "block," which is then added to the existing chain of blocks in chronological order. This process is secured through consensus mechanisms like proof-of-work or proof-of-stake.

What is the difference between Bitcoin and blockchain?

Bitcoin is a cryptocurrency, while blockchain is the underlying technology that makes Bitcoin possible. Blockchain is the infrastructure that records transactions, while Bitcoin is one specific application of that technology. Many other cryptocurrencies and applications use blockchain for purposes beyond digital money.

Is blockchain secure?

Yes, blockchain is considered highly secure due to its decentralized nature and cryptographic protections. Each block contains a unique digital fingerprint and is connected to the previous block, making it extremely difficult to alter historical records. However, the security also depends on the specific implementation and the consensus mechanism used.

What are smart contracts?

Smart contracts are self-executing programs stored on a blockchain that automatically enforce predefined rules when specific conditions are met. For example, a smart contract could automatically release payment once a shipment is confirmed, eliminating the need for intermediaries like banks or lawyers.

What industries use blockchain technology?

Blockchain is used across many industries including finance (banking, payments, trading), supply chain management, healthcare, real estate, government, entertainment, and insurance. Major companies like Walmart, IBM, JPMorgan, and Microsoft have implemented blockchain solutions for various business processes.