Return on investment (ROI) stands as one of the most critical metrics in finance and business decision-making. At its core, ROI measures the profitability of an investment by comparing the gain or loss generated relative to its cost. Whether you're evaluating a marketing campaign, assessing real estate purchases, or analyzing stock performance, understanding how to calculate ROI provides the foundation for making informed financial decisions. The basic ROI formula—subtracting the cost of investment from the current value, dividing by the cost, and multiplying by 100 to express as a percentage—offers a universal language for comparing investment opportunities across different asset classes and time horizons.

Key Insights

- ROI expresses profitability as a percentage, making comparison across different investments possible

- The formula works for any investment type but requires consistent measurement of costs and returns

- Annualized ROI adjusts for investments held for different time periods

- Simple ROI calculations can overlook important factors like taxes, inflation, and opportunity costs

Why ROI Matters in Financial Decision-Making

ROI serves as a universal metric that allows investors, business owners, and managers to evaluate the efficiency and profitability of their investments. According to a 2023 survey by the Financial Planning Association, 87% of financial advisors use ROI as a primary metric when recommending investment strategies to clients. This widespread adoption stems from ROI's simplicity and versatility—a single percentage figure communicates whether an investment has created or destroyed value.

The importance of ROI extends beyond individual investment decisions. Corporations utilize ROI metrics to allocate capital effectively, with the Harvard Business Review reporting in 2022 that companies with strong ROI measurement practices achieved 23% higher returns on capital compared to those without formalized evaluation processes. Business owners apply ROI calculations to determine which projects deserve funding, while marketing teams measure campaign effectiveness through return on advertising spend—a specialized ROI application that Google estimates drives over $200 billion in annual digital advertising spending globally.

Beyond profitability assessment, ROI facilitates goal-setting and performance benchmarking. When you calculate ROI consistently, you establish a baseline for evaluating future investments and can track whether your decision-making improves over time. This data-driven approach reduces reliance on intuition and emotional investing, replacing it with measurable criteria that can be analyzed, compared, and optimized.

The Basic ROI Formula Explained

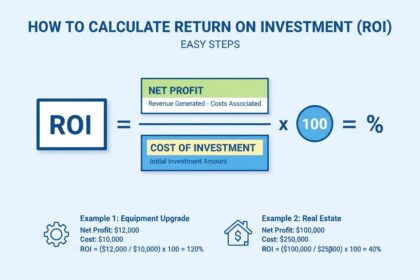

The fundamental ROI formula requires only two inputs: the current value of the investment and the original cost. The mathematical expression appears as:

ROI = ((Current Value - Cost) / Cost) × 100

Breaking down each component reveals why this formula works effectively:

Current Value represents what the investment is worth today, including any distributions received such as dividends, interest payments, or rental income. For a stock, this equals the current market price plus dividends collected. For real estate, it includes the property's current market value plus any rental income earned minus expenses.

Cost encompasses the total amount invested, including the purchase price and any associated expenses such as transaction fees, maintenance costs, or improvement expenses. Accurate cost tracking proves essential—understating costs inflates ROI artificially, while overstating costs understates true performance.

The resulting percentage indicates how much profit or loss the investment generated relative to its cost. A positive ROI indicates profitability, while a negative ROI signals that the investment lost money. For example, an ROI of 25% means the investment generated profits equal to 25% of the original cost—in other words, you received $1.25 for every $1 invested.

This straightforward calculation provides immediate insight into investment performance. However, the simplicity that makes ROI valuable also creates limitations, particularly when comparing investments held for different time periods or requiring different capital commitments.

Step-by-Step ROI Calculation Examples

Example 1: Stock Investment

Imagine you purchased 100 shares of a company at $50 per share, paying a $10 commission. After holding the stock for two years, it trades at $65 per share, and you received $2 per share in dividends during the holding period.

Calculating ROI:

- Initial investment: (100 × $50) + $10 = $5,010

- Final value: (100 × $65) + (100 × $2) = $6,700

- Profit: $6,700 - $5,010 = $1,690

- ROI: ($1,690 / $5,010) × 100 = 33.7%

This 33.7% return represents your total profit over the two-year holding period, combining both capital appreciation and dividend income.

Example 2: Small Business Investment

Consider investing $50,000 in a small business that generates $15,000 in annual profit. After three years, you sell the business for $55,000.

Calculating ROI:

- Initial cost: $50,000

- Total profits received: $15,000 × 3 = $45,000

- Final sale value: $55,000

- Total return: $45,000 + $55,000 = $100,000

- ROI: (($100,000 - $50,000) / $50,000) × 100 = 100%

Your initial $50,000 investment doubled in value over three years, generating a 100% total ROI, or approximately 33.3% annually when annualized.

Example 3: Marketing Campaign

A company spends $10,000 on a digital advertising campaign that generates $35,000 in sales attributed to the campaign.

Calculating ROI:

- Campaign cost: $10,000

- Revenue generated: $35,000

- Profit: $35,000 - $10,000 = $25,000

- ROI: ($25,000 / $10,000) × 100 = 250%

This 250% ROI indicates the marketing investment produced $2.50 in revenue for every dollar spent—a strong return that supports expanded advertising budgets.

Annualized ROI: Accounting for Different Time Periods

Simple ROI calculations work well when comparing investments held for identical periods. However, most investors encounter opportunities with varying holding periods, making direct comparison problematic. An investment generating 50% ROI over five years outperforms one generating 25% ROI over one year, yet simple ROI suggests the opposite. Annualized ROI corrects this distortion by expressing returns as an annual percentage rate.

Annualized ROI Formula:

Annualized ROI = ((1 + Total ROI)^(1/Years) - 1) × 100

Using the previous examples:

Three-Year Business Investment:

- Total ROI: 100%

- Years: 3

- Annualized ROI = ((1 + 1.00)^(1/3) - 1) × 100 = ((2)^0.333 - 1) × 100 = 26% annually

Five-Year Investment at 50% Total Return:

- Total ROI: 50%

- Years: 5

- Annualized ROI = ((1 + 0.50)^(1/5) - 1) × 100 = ((1.50)^0.20 - 1) × 100 = 8.4% annually

The annualization formula uses compound interest mathematics, reflecting how investment returns compound over time. This approach aligns with how financial institutions present returns, enabling meaningful comparisons across investments with different holding periods.

The Internal Rate of Return (IRR) provides an even more sophisticated approach, accounting for the timing and size of cash flows throughout the investment period. While IRR calculations require financial calculators or software, they offer superior accuracy for investments with irregular cash flows.

Common ROI Calculation Mistakes to Avoid

Even experienced investors frequently make errors that distort ROI calculations, leading to poor decision-making. Understanding these pitfalls helps ensure your calculations provide accurate insight.

Mistake #1: Ignoring All Costs

Many investors calculate ROI using only the purchase price while overlooking transaction fees, maintenance expenses, or ongoing holding costs. A mutual fund with a 1% annual expense ratio significantly underperforms gross returns. Always include every cost associated with acquiring, holding, and disposing of an investment.

Mistake #2: Mismeasuring Returns

Investors sometimes count only capital appreciation while forgetting income distributions. A rental property showing modest appreciation may generate excellent returns when including rental income. Similarly, stock returns require adding dividends to price gains for accurate measurement.

Mistake #3: Using Ending Value Without Adjusting for External Factors

Simple ROI calculations don't account for inflation or changes in purchasing power. An investment returning 10% annually during a period of 8% inflation actually provides minimal real return. For long-term investments, consider calculating real ROI by adjusting returns for inflation rates.

Mistake #4: Comparing Incommensurate Investments

Comparing ROI across investments with vastly different risk profiles misleads decision-making. A savings account offering 4% ROI and a stock portfolio generating 8% ROI aren't equivalent—the stock carries substantially higher risk. Always consider risk-adjusted returns when evaluating investment choices.

| Mistake | Impact | Solution |

|---|---|---|

| Ignoring costs | Inflates apparent returns | Track all expenses comprehensively |

| Missing income | Understates total returns | Include all distributions |

| Ignoring inflation | Overstates purchasing power gains | Calculate real returns |

| Ignoring risk | Misleading comparisons | Consider risk-adjusted metrics |

ROI Applications Across Different Contexts

Real Estate Investment

Real estate ROI calculations require careful attention to both appreciation and ongoing income. Beyond purchase price and sale proceeds, investors must account for mortgage interest, property taxes, insurance, maintenance, property management fees, and periods of vacancy. The Cap Rate (Capitalization Rate) provides a standardized metric for comparing rental properties: Cap Rate = Net Operating Income / Property Value.

For residential real estate, the return on investment in real estate calculations typically include both equity buildup from mortgage payments and appreciation, creating a more complex picture than simple rental yield.

Marketing and Advertising

Marketing ROI has become increasingly sophisticated with digital advertising. Return on Ad Spend (ROAS) represents a specialized marketing ROI metric: ROAS = Revenue from Ads / Cost of Ads. A business spending $5,000 on advertising that generates $20,000 in attributed sales achieves a 4:1 ROAS, equivalent to 300% ROI when calculated as ((Revenue - Cost) / Cost).

The distinction between marketing ROI and attribution accuracy remains critical. Tracking which marketing channels actually drive conversions requires proper analytics implementation, without which ROI calculations reflect guesswork rather than measurable performance.

Business Investments and Projects

Capital budgeting decisions rely heavily on ROI calculations, typically expressed as expected return on investment. Businesses evaluate potential projects by estimating costs, projecting revenues, and calculating expected ROI. The payback period—how long until an investment recovers its initial cost—complements ROI analysis, providing insight into both profitability and liquidity risk.

Beyond Basic ROI: When to Use Alternative Metrics

While ROI serves as an invaluable starting point, certain situations require additional or alternative metrics for complete investment analysis.

Return on Equity (ROE) measures profitability relative to shareholder equity, revealing how effectively a company uses investor capital. Warren Buffett frequently emphasizes ROE when evaluating businesses, preferring companies generating consistent returns above 15% on equity.

Return on Assets (ROA) assesses how efficiently management employs total assets to generate profits, useful for comparing companies within the same industry regardless of financing structure.

Net Present Value (NPV) accounts for the time value of money by discounting future cash flows to present dollars. For long-term investments with cash flows spanning many years, NPV provides more accurate profitability assessment than simple ROI.

Cash-on-Cash Return measures annual pre-tax cash flow relative to total cash invested, commonly used in real estate where mortgage financing creates leverage effects that distort simple ROI calculations.

Each metric serves specific purposes—the key lies in selecting appropriate measurements for your particular decision context rather than relying exclusively on any single calculation.

Frequently Asked Questions

What is a good ROI percentage?

A "good" ROI depends heavily on the investment type, associated risks, and current market conditions. Historically, the stock market has returned approximately 7-10% annually after inflation. Real estate typically aims for 8-12% total annual returns. Riskier investments like small business ventures or startup equity require proportionally higher potential returns to compensate for elevated failure risk—many investors seek 25%+ returns for such speculative investments.

How do I calculate ROI if I have multiple investments?

To calculate ROI for a portfolio containing multiple investments, aggregate all costs and all returns across the portfolio, then apply the standard ROI formula. For example, if you hold three stocks with total costs of $30,000 and combined current value of $38,000, your portfolio ROI equals (($38,000 - $30,000) / $30,000) × 100 = 26.67%.

Can ROI be negative?

Yes, ROI can be negative when an investment loses money. A negative ROI simply indicates that the current value falls below your total investment cost. For instance, if you invest $1,000 in stock and it's now worth $800, your ROI equals (($800 - $1,000) / $1,000) × 100 = -20%.

What is the difference between ROI and ROE?

ROI measures return on an investment relative to its total cost, applicable to any investment type. ROE (Return on Equity) specifically measures return relative to shareholder equity in a business, revealing how effectively management uses investor capital. A company might have strong ROI while generating modest ROE if significant debt financing amplifies returns on the smaller equity base.

How do I annualize ROI for less than one year?

To annualize ROI for periods less than one year, apply the formula: Annualized ROI = ((1 + Total ROI)^(365/Days) - 1) × 100. For example, a 10% return over six months (182 days) annualizes to ((1.10)^(365/182) - 1) × 100 = approximately 21.2% annually.

Does ROI account for taxes?

No, basic ROI calculations do not automatically incorporate taxes. Investment returns can be significantly reduced by capital gains taxes, income taxes on dividends or interest, and property taxes. For accurate after-tax ROI, subtract estimated tax costs from gains before calculating the return percentage.

Conclusion

Mastering ROI calculations empowers you to evaluate investment opportunities systematically, compare alternatives objectively, and track portfolio performance over time. The fundamental formula—((Current Value - Cost) / Cost) × 100—provides immediate insight into any investment's profitability, while annualized calculations enable fair comparison across different holding periods. Remember that ROI represents only one piece of the investment analysis puzzle; combining ROI with risk assessment, cash flow analysis, and appropriate alternative metrics creates comprehensive evaluation frameworks for sound financial decision-making.

As you apply these calculations to your investments, maintain discipline in tracking all costs, measuring returns comprehensively, and annualizing returns for time-appropriate comparisons. Whether you're evaluating a marketing campaign, analyzing real estate opportunities, or assessing stock performance, consistent application of proper ROI methodology will improve your investment outcomes over time.