Compound interest is one of the most fundamental concepts in finance. For American investors looking to build long-term wealth, understanding how it works can significantly impact financial growth. This guide covers the mechanics, benefits, and practical applications of compound interest in investing.

Understanding Compound Interest

Compound interest is interest calculated on both your initial principal and the accumulated interest from previous periods. Unlike simple interest, which applies only to the original amount, compound interest allows your money to grow exponentially over time.

The process works through interest on interest. As your investment grows, each new calculation includes a larger base amount, creating a compounding effect that accelerates wealth accumulation. This principle underlies many investment strategies and retirement planning approaches used by Americans across all income levels.

The Securities and Exchange Commission considers understanding compound interest essential for anyone pursuing financial independence through investing. The mechanism works the same whether you're dealing with savings accounts, bonds, stocks, or retirement accounts.

The Mathematics Behind Compound Interest

The formula for compound interest uses several variables: the principal amount (P), the annual interest rate (r), the number of times interest compounds per year (n), and the time period in years (t). The formula is A = P(1 + r/n)^(nt), where A represents the final amount.

Here's a practical example. If you invest $10,000 at 7% annual interest compounded annually, your investment grows to $10,700 after one year. After ten years, it reaches approximately $19,672 without adding any money. After 30 years, the $10,000 transforms into roughly $76,123—far more than simple interest would produce.

Compounding frequency matters. Accounts that compound monthly or daily generate higher returns than those compounding annually, though the difference becomes most noticeable over longer periods.

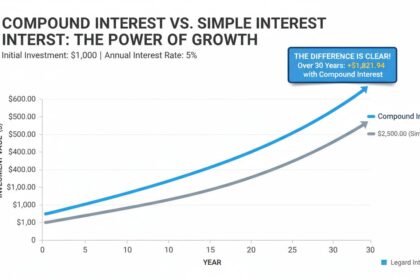

Compound Interest Versus Simple Interest

Simple interest calculates returns only on the principal amount. Your earnings remain constant throughout the investment period. If you invest $10,000 at 5% simple interest annually, you earn exactly $500 each year. After ten years, you have $15,000—your original $10,000 plus $5,000 in total interest.

Compound interest produces progressively larger interest payments over time. Using the same $10,000 at 5% compounded annually, you earn $500 in the first year, $525 in the second (5% of $10,500), and $551.25 in the third (5% of $10,525). The differences seem small at first but accumulate dramatically over decades.

This distinction matters most for long-term investors. Financial advisors often note that compound interest's true power emerges over periods of 10, 20, or 30 years. The exponential growth curve means most of your investment's growth occurs in the later years, rewarding patience.

Why Compound Interest Matters for Long-Term Investors

Compound interest plays a crucial role in building retirement savings. For Americans with 401(k) plans or Individual Retirement Accounts (IRAs), the compound growth of these tax-advantaged accounts determines much of their retirement security. Data from the Investment Company Institute shows that average 401(k) balances for those approaching retirement have grown substantially, largely due to decades of compound growth.

Tax-advantaged retirement accounts amplify compound interest's effects because you don't pay taxes on gains until withdrawal. This allows your entire balance to compound uninterrupted by annual tax obligations. Roth versions of these accounts offer tax-free growth entirely.

Beyond retirement accounts, compound interest benefits anyone willing to invest consistently over time—whether funding a college education through a 529 plan or building an emergency fund in a high-yield savings account.

Real-World Examples of Compound Interest at Work

Consider two investors starting at age 25. Investor A contributes $200 monthly to an account earning 7% average annual returns until age 65. Investor B waits until age 35 to begin the same contribution, continuing until age 65. Investor A accumulates approximately $402,000. Investor B reaches only about $173,000—a difference of more than $229,000.

This example demonstrates the critical importance of starting early. The additional decade of compound growth creates nearly $230,000 in extra value from the same monthly contribution. Time, not just money, drives compound interest's power.

Another example involves reinvested dividends. When dividend-paying stocks are held in accounts that automatically reinvest dividends, shareholders acquire additional shares that themselves generate dividends. Over decades, this dramatically increases total returns.

Factors Affecting Compound Interest Growth

Several variables determine how effectively compound interest works in your favor. The interest rate or rate of return is the most obvious—higher rates produce faster growth. However, you must balance expected returns against risks, as higher-return investments typically carry greater volatility.

The investment timeline creates perhaps the most dramatic impact. Compound interest requires time to generate meaningful results. Short-term investors often see minimal benefits compared to those with multi-decade horizons. This is why financial professionals emphasize starting early and maintaining consistent contributions regardless of market conditions.

Inflation represents another critical consideration. While compound interest grows your nominal balance, inflation erodes purchasing power over time. Investments must earn returns exceeding inflation rates to produce genuine growth.

Investment Vehicles That Utilize Compound Interest

Many investment products harness compound interest. Certificates of deposit (CDs) provide guaranteed returns with compound interest calculated regularly. High-yield savings accounts offer compound interest, though rates fluctuate.

Bonds represent another common vehicle. When bondholders reinvest coupon payments, they benefit from compound interest. Municipal bonds, corporate bonds, and Treasury securities all operate on this principle.

Stock investments achieve compound growth through dividend reinvestment and capital appreciation. The historical average annual return of the S&P 500 has exceeded 10% over very long periods. Index funds and exchange-traded funds (ETFs) provide diversified exposure to this growth with minimal fees.

Retirement accounts—traditional and Roth IRAs plus 401(k) plans—represent the most tax-efficient vehicles for compound growth. These accounts allow investments to grow tax-deferred or tax-free, maximizing the compounding effect.

Potential Pitfalls and Considerations

Compound interest can work against you with debt. Credit card balances that compound monthly can quickly spiral into unmanageable levels. Paying off high-interest debt typically precedes aggressive investing.

Fees and expenses significantly reduce compound growth. Investment management fees, expense ratios, and advisory costs all diminish returns. Low-cost index funds have gained popularity because minimal fees allow more of your returns to compound over time.

Market volatility presents another challenge. While historical stock market returns have produced excellent compound growth, individual periods may experience significant losses. Investors who panic and sell during downturns forfeit compound growth that would have occurred during recovery.

Conclusion

Compound interest remains one of the most powerful tools available for investors seeking financial security. By understanding how interest on interest creates exponential growth, you can make decisions that maximize long-term wealth accumulation. Starting early, maintaining consistent contributions, and holding investments for extended periods produces the most favorable outcomes. While compound interest cannot guarantee success or protect against all risks, it provides a foundational principle that has helped generations of Americans build sustainable wealth.

Frequently Asked Questions

What is compound interest in investing?

Compound interest in investing means earning interest on both your initial investment and on interest that has already been added to your balance. This creates a snowball effect where your money grows exponentially over time.

How does compound interest differ from simple interest?

Simple interest calculates returns only on the original principal, keeping earnings constant. Compound interest calculates returns on the principal plus accumulated interest, producing progressively larger returns and significantly higher final values over long periods.

How long does it take for compound interest to work effectively?

Compound interest typically becomes significantly impactful over 10 years or more. Most of the effect occurs in the later years of an investment, making long-term holding essential.

What investment accounts offer compound interest?

Many vehicles offer compound interest: high-yield savings accounts, CDs, bonds, dividend-paying stocks, and tax-advantaged retirement accounts like 401(k)s and IRAs. Return rates and compounding frequency vary by product.

How can I maximize compound interest benefits?

Start investing as early as possible, maintain consistent contributions regardless of market conditions, choose investments with favorable after-fee returns, hold investments for extended periods, and minimize fees while avoiding high-interest debt.

Does compound interest work in all market conditions?

Compound interest works mathematically regardless of market conditions, but actual returns vary based on market performance. In declining markets, portfolio value may decrease even though the principle remains intact. Patient investors who maintain positions through market cycles generally benefit from compound growth over extended periods.