QUICK ANSWER: The compound interest formula is A = P(1 + r/n)^(nt), where A is the final amount, P is your principal, r is the annual interest rate (as a decimal), n is the number of times interest compounds per year, and t is the time in years. This powerful mathematical concept allows your money to grow exponentially rather than linearly, making it the foundation of long-term wealth building.

AT-A-GLANCE:

| Component | Symbol | Description | Example |

|---|---|---|---|

| Principal | P | Initial investment | $10,000 |

| Annual Rate | r | Interest rate as decimal | 0.07 (7%) |

| Compounding | n | Times per year | 12 (monthly) |

| Time | t | Years invested | 10 years |

| Final Amount | A | Result | $20,096 |

KEY TAKEAWAYS:

- ✅ Compound interest earns interest on interest, dramatically increasing your returns over time—$10,000 at 7% becomes $20,096 in 10 years with monthly compounding

- ✅ The "Rule of 72" estimates doubling time: divide 72 by your interest rate (72 ÷ 7 = 10.3 years to double your money at 7%)

- ✅ More frequent compounding (daily > monthly > annually) yields higher returns due to interest being calculated on progressively larger amounts

- ❌ Common mistake: Ignoring compounding frequency—many calculators default to annual compounding when monthly is more realistic for most savings accounts

- 💡 Expert insight: "Compound interest is the eighth wonder of the world. He who understands it, earns it ... he who doesn't ... pays it." — Albert Einstein (attributed)

KEY ENTITIES:

- Formulas: A = P(1 + r/n)^(nt), A = Pe^(rt) (continuous compounding)

- Concepts: Principal, Interest Rate, Compounding Frequency, Time Horizon, Doubling Time

- Experts: Albert Einstein (attributed), Benjamin Franklin (pioneer of compound savings)

- Applications: Savings Accounts, Certificates of Deposit (CDs), Stock Market Investing, Retirement Accounts (401k, IRA)

LAST UPDATED: January 14, 2026

Understanding the Compound Interest Formula

Compound interest represents one of the most powerful forces in finance, yet many people misunderstand how it works or fail to maximize its potential. Unlike simple interest, which calculates returns only on your original principal, compound interest calculates returns on both your principal and previously earned interest. This seemingly small difference creates dramatically different outcomes over time.

The fundamental formula A = P(1 + r/n)^(nt) breaks down into five key components. The principal (P) represents your initial investment or loan amount—this is the foundation upon which all future growth builds. The annual interest rate (r), expressed as a decimal rather than a percentage, determines how quickly your money grows. The compounding frequency (n) represents how many times per year interest is calculated and added to your balance. Time (t), measured in years, amplifies the compounding effect exponentially. Finally, the result (A) shows your final amount after all compounding periods have elapsed.

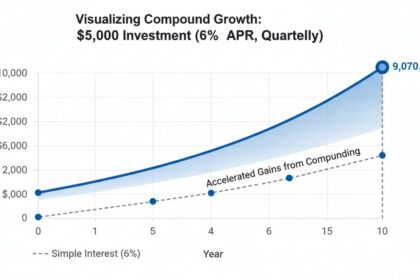

What makes compound interest so remarkable is the exponential nature of growth. In the first year, you earn interest only on your principal. By the second year, you earn interest on your principal plus the first year's interest. By year ten, you're earning interest on a substantially larger base that includes nine years of accumulated interest. This snowball effect explains why starting to save early—even with modest amounts—can outperform waiting to invest larger sums later in life.

Breaking Down Each Component of the Formula

Understanding each variable in the compound interest formula helps you make smarter financial decisions and accurately project your wealth accumulation.

Principal (P): Your initial investment forms the foundation of all compound interest calculations. Whether you're starting with $1,000 or $100,000, this amount grows untouched while interest compounds. Many people mistakenly believe they need large sums to begin investing, but starting small with consistent contributions often outperforms waiting for larger initial amounts thanks to the time value of compounding.

Annual Interest Rate (r): The interest rate significantly impacts your final returns. A difference of just 1-2% annually creates massive differences over decades. For context, the S&P 500 has historically returned approximately 7-10% annually adjusted for inflation, while high-yield savings accounts currently offer 4-5% as of early 2026. Certificates of deposit and bonds offer varying rates depending on term length and credit quality. Always convert percentage rates to decimals (7% becomes 0.07) before using them in calculations.

Compounding Frequency (n): This variable determines how often interest is calculated and added to your balance. Common options include annually (n=1), semi-annually (n=2), quarterly (n=4), monthly (n=12), and daily (n=365). More frequent compounding yields higher returns because interest begins earning its own interest sooner. The difference between annual and daily compounding might seem negligible on $1,000, but on $100,000 over 30 years, this difference amounts to thousands of dollars.

Time (t): Time is the most powerful variable in compound interest calculations. The magic of compounding requires patience—your money needs years to truly accelerate. Five years produces modest growth, while 20 or 30 years can transform modest savings into substantial wealth. This is why financial advisors emphasize starting retirement savings in your 20s rather than waiting until your 40s.

Step-by-Step Calculation Examples

Let's walk through practical examples demonstrating how the compound interest formula works in real-world scenarios.

Example 1: Initial Savings Growth

Imagine you deposit $10,000 in a high-yield savings account offering 4.5% APY, compounded monthly, for 10 years.

Using the formula: A = 10000(1 + 0.045/12)^(12×10)

- Monthly rate: 0.045 ÷ 12 = 0.00375

- Total compounding periods: 12 × 10 = 120

- Calculation: 10000 × (1.00375)^120 = $15,583.70

Your $10,000 grows to $15,583.70—a 55.8% return purely from compound interest. Without compounding (simple interest at 4.5% annually), you'd only have $14,500.

Example 2: Investment Portfolio Growth

Consider investing $50,000 in a diversified index fund with an average annual return of 8%, compounded quarterly, over 25 years.

Using the formula: A = 50000(1 + 0.08/4)^(4×25)

- Quarterly rate: 0.08 ÷ 4 = 0.02

- Total compounding periods: 4 × 25 = 100

- Calculation: 50000 × (1.02)^100 = $367,862.89

That initial $50,000 transforms into nearly $368,000—a 636% increase. The power of 25 years of compounding at 8% annually creates extraordinary wealth multiplication.

Example 3: Regular Contributions

Most people don't have $50,000 to invest upfront. Let's calculate with monthly contributions: $500 monthly into an account earning 7% annually, compounded monthly, for 30 years.

This requires a modified formula for regular contributions: FV = PMT × [((1 + r/n)^(nt) - 1) / (r/n)]

- Monthly contribution: $500

- Monthly rate: 0.07 ÷ 12 = 0.005833

- Total periods: 12 × 30 = 360

- Calculation: 500 × [((1.005833)^360 - 1) / 0.005833] = $608,018.14

Contributing just $500 monthly for 30 years produces over $608,000—your contributions total $180,000 while compound interest adds over $428,000.

The Rule of 72: Quick Mental Math

While the exact compound interest formula provides precise calculations, the Rule of 72 offers a quick mental shortcut to estimate how long it takes your money to double.

Simply divide 72 by your annual interest rate to estimate doubling time in years. At 6% annual returns, your money doubles in approximately 12 years (72 ÷ 6 = 12). At 8%, it doubles in about 9 years. This remarkably accurate rule helps you visualize exponential growth without calculators.

The Rule of 72 works because it approximates the natural logarithm relationship in compound interest calculations. While not perfectly precise, it provides sufficiently accurate estimates for financial planning conversations and quick comparisons between investment options.

You can also use the Rule of 72 in reverse: to estimate what interest rate you need to double your money in a specific timeframe. Need to double your money in 6 years? You'll need approximately 12% annual returns (72 ÷ 6 = 12).

Compound Interest in Different Investment Vehicles

Understanding how compound interest applies to various financial products helps you make better investment choices.

Savings Accounts: Traditional savings accounts offer relatively low interest rates (typically 0.01%-0.1%), meaning compound growth is slow. High-yield savings accounts, available from online banks, currently offer 4-5% APY as of early 2026, providing significantly better compound growth while maintaining FDIC insurance coverage up to $250,000.

Certificates of Deposit (CDs): CDs typically offer higher rates than regular savings accounts in exchange for locking your money for a specified period—ranging from 3 months to 5+ years. Longer terms generally offer higher rates, reflecting the reduced liquidity. Interest usually compounds monthly or annually, and early withdrawal penalties apply.

Stock Market Investments: While stocks don't offer guaranteed "interest," the overall market has historically returned approximately 7-10% annually over long periods when adjusted for inflation. These returns compound through capital appreciation and dividend reinvestment. Index funds provide broad market exposure with low fees, making them ideal vehicles for long-term compound growth.

Retirement Accounts: 401(k) and IRA accounts offer tax advantages that further enhance compound growth. Traditional accounts provide tax-deferred growth (you pay taxes upon withdrawal), while Roth accounts offer tax-free growth (you pay taxes on contributions but withdrawals are tax-free). Employer 401(k) matches essentially provide instant "interest" on your contributions, supercharging compound growth.

Bonds: Bond investments pay regular interest (coupon payments), typically semi-annually. While the principal doesn't compound internally the way savings interest does, you can reinvest bond payments to achieve compound growth. Treasury bonds, corporate bonds, and municipal bonds each offer different risk-return profiles and tax treatments.

Maximizing Compound Interest Benefits

Understanding strategies to maximize compound interest helps you build wealth faster.

Start Early: Time is your greatest ally. Someone investing $5,000 annually from age 25 to 35 (10 years of contributions) will have more money at age 65 than someone investing $5,000 annually from age 35 to 65 (30 years of contributions), assuming 7% annual returns. This counterintuitive result demonstrates the overwhelming power of early compounding.

Increase Compounding Frequency: Choose accounts that compound more frequently. Daily compounding yields more than monthly, which yields more than annual. The difference isn't enormous, but every advantage matters.

Maintain Consistent Contributions: Regular contributions dramatically accelerate wealth building. The combination of consistent investing and compound interest creates what investors call "dollar-cost averaging plus compounding"—a powerful wealth-building duo.

Reinvest All Earnings: Dividends, interest payments, and capital gains should be reinvested rather than spent. Taking profits interrupts the compounding chain and significantly reduces long-term returns.

Minimize Fees: High investment fees erode compound returns. A 1% annual fee might seem insignificant, but over 30 years on a growing portfolio, it can cost you 20-30% of your potential returns. Choose low-cost index funds and index ETFs to minimize this drag.

Frequently Asked Questions

Q: What is the basic compound interest formula?

Direct Answer: The basic compound interest formula is A = P(1 + r/n)^(nt), where A is your final amount, P is your principal (starting money), r is your annual interest rate as a decimal, n is how many times interest compounds per year, and t is the number of years.

Detailed Explanation: This formula calculates compound interest by raising the growth factor (1 + r/n) to the power of total compounding periods (nt). For example, $10,000 at 5% interest compounded monthly for one year calculates as: 10000 × (1 + 0.05/12)^(12×1) = $10,511.62. The monthly compounding adds $511.62 in interest versus $500 with simple annual interest.

Q: How do I calculate compound interest in Excel?

Direct Answer: In Excel, use the formula =P(1+r/n)^(nt) in any cell, replacing P, r, n, and t with your numbers or cell references.

Detailed Explanation: Excel offers several functions for compound interest. The basic formula above works for most scenarios. For future value with regular contributions, use =FV(r/n, n*t, -PMT, -P). Excel's EFFECT function converts nominal rates to effective annual rates. Google Sheets uses identical formulas. Remember to format cells containing results as Currency to see dollar signs and decimal places clearly.

Q: What is the difference between simple interest and compound interest?

Direct Answer: Simple interest calculates returns only on your original principal, while compound interest calculates returns on your principal plus previously earned interest.

Detailed Explanation: With simple interest at 5% on $10,000 for 3 years, you'd earn $500 annually ($10,000 × 0.05 = $500), totaling $1,500 in interest. With compound interest, year one earns $500, year two earns $525 ($10,500 × 0.05), and year three earns $551.25 ($11,025 × 0.05), totaling $1,576.25. Over longer periods or larger amounts, the difference becomes substantial—sometimes tens of thousands of dollars.

Q: How long does it take for compound interest to double my money?

Direct Answer: Use the Rule of 72: divide 72 by your annual interest rate. At 6% returns, your money doubles in approximately 12 years (72 ÷ 6 = 12).

Detailed Explanation: The Rule of 72 provides a quick, reasonably accurate estimate without complex calculations. At 8% (historical stock market average), money doubles in about 9 years. At 4% (typical high-yield savings), it takes roughly 18 years. Remember this is an approximation—the precise doubling time at 6% is 11.9 years using natural logarithms, but 72 provides a close, easy-to-remember estimate.

Q: Does compound interest work with regular monthly contributions?

Direct Answer: Yes, compound interest works powerfully with regular contributions, using the formula: FV = PMT × [((1 + r/n)^(nt) - 1) / (r/n)].

Detailed Explanation: This future value of an annuity formula calculates how much your regular contributions grow. For $500 monthly at 7% annual return compounded monthly for 30 years, you'd have over $608,000—more than triple your $180,000 in contributions. The key insight: consistent monthly contributions combined with compound interest create extraordinary long-term wealth, which is why financial advisors emphasize starting retirement savings early, even with small amounts.

Q: What is continuous compound interest?

Direct Answer: Continuous compound interest uses the formula A = Pe^(rt), where e is Euler's number (approximately 2.71828), representing the mathematical limit of infinitely frequent compounding.

Detailed Explanation: Continuous compounding represents the theoretical maximum growth possible when interest is calculated and added an infinite number of times per instant. While no actual investment compounds continuously, this formula provides an upper bound and is useful in theoretical finance and certain economic models. For most practical purposes, daily compounding comes extremely close—the difference between daily and continuous compounding on $10,000 at 5% for one year is less than a dollar.

Conclusion: Harnessing Compound Interest for Financial Growth

The compound interest formula—A = P(1 + r/n)^(nt)—represents one of mathematics' most powerful wealth-building tools. Unlike linear simple interest, compound interest creates exponential growth that accelerates over time, transforming modest savings into substantial wealth when given sufficient time to develop.

KEY ACTION STEPS:

| Timeframe | Action | Expected Outcome |

|---|---|---|

| Today (30 min) | Calculate your current savings potential using the formula | Clear picture of starting point |

| This Week (2 hrs) | Open high-yield savings account or increase 401(k) contributions | Begin compound growth immediately |

| This Month | Set up automatic monthly contributions | Ensure consistent wealth building |

| Long-term | Review and adjust portfolio annually | Optimize returns and compounding frequency |

The most critical insight from understanding compound interest is that time matters more than almost any other factor. Starting now—even with small amounts—outperforms waiting to start later with larger sums. The math is unambiguous: 30 years of compound growth on modest contributions typically exceeds 10 years of growth on larger contributions.

Your next step is to apply this formula to your specific situation. Calculate how your current savings might grow. Determine what regular contributions you can commit to. Choose accounts with favorable interest rates and compounding frequencies. Then let mathematics work in your favor over the decades ahead.

Remember: the best time to start harnessing compound interest was yesterday. The second-best time is today.