The relationship between interest rates and the stock market is one of the most fundamental dynamics in finance. When the Federal Reserve adjusts interest rates, it sets off a chain reaction that ripples through every sector of the stock market—from growth technology stocks to dividend-paying utilities. Understanding this connection isn't just for Wall Street professionals; it's essential knowledge for any investor looking to make informed decisions about their portfolio.

This guide breaks down exactly how interest rate changes influence stock prices, which sectors feel the impact most acutely, and how you can position your investments to weather rate fluctuations. Whether you're managing a 401(k), building a stock portfolio, or simply want to understand the economic forces shaping your financial future, this comprehensive overview provides the insights you need.

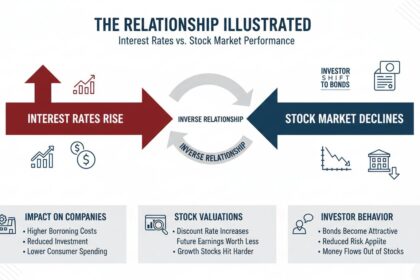

The Fundamental Connection Between Interest Rates and Stock Values

At its core, the stock market values companies based on the future cash flows those companies will generate. Interest rates serve as the discount rate applied to those future cash flows—a technical concept that has very real implications for your portfolio.

When interest rates rise, the discount rate increases, which means future earnings are worth less in today's dollars. This causes stock prices to decline, particularly for companies whose value is heavily weighted toward earnings far in the future. Growth stocks, which promise substantial returns years down the line, suffer the most when rates climb.

Conversely, when interest rates fall, the discount rate decreases, making future earnings more valuable today. This pushes stock prices higher, especially for growth companies that will generate the bulk of their profits in later years.

The Federal Reserve's benchmark federal funds rate serves as the foundation for all other interest rates in the economy. As of January 2025, the Fed has maintained rates in the 4.25%-4.50% range following an aggressive hiking cycle that began in March 2022 (Federal Reserve Economic Data, January 2025). Understanding where rates are and where they're heading is crucial for timing your investment decisions.

How Federal Reserve Rate Decisions Ripple Through the Stock Market

The Federal Reserve doesn't set stock prices directly, but its monetary policy decisions create the conditions that determine valuations. Here's how the transmission mechanism works:

Direct Impact on Borrowing Costs: When the Fed raises rates, borrowing becomes more expensive for businesses. Companies carrying significant debt see their interest expenses increase, which compress profit margins and can reduce earnings growth. This is particularly challenging for capital-intensive industries like manufacturing, utilities, and real estate.

Impact on Consumer Spending: Higher interest rates mean higher costs for mortgages, auto loans, and credit cards. As consumers face increased borrowing costs, they often reduce spending. Companies that depend on consumer discretionary spending—from retailers to travel companies—can see revenues decline as a result.

Currency and International Effects: Higher U.S. interest rates attract foreign capital seeking better returns, strengthening the dollar. While this helps companies with international operations (by making foreign earnings worth more in dollar terms), it hurts multinational corporations that sell products abroad because their goods become more expensive for overseas customers.

The Fed typically signals rate changes well in advance through official statements and Federal Reserve Chair Jerome Powell's press conferences. Savvy investors watch these signals carefully. According to research from the National Bureau of Economic Research , the stock market often begins pricing in rate changes months before the actual Fed decision, making it crucial to anticipate rather than react.

Sector-by-Sector Analysis: Winners and Losers in a High-Rate Environment

Not all stocks respond equally to interest rate changes. Understanding which sectors benefit and which suffer helps you build a more resilient portfolio.

sectors that Struggle with Higher Interest Rates

| Sector | Challenge | Why It Matters |

|---|---|---|

| Technology/Growth | Higher discount rates | Future earnings worth less; expensive valuations compress |

| Real Estate | Higher mortgage rates | Fewer people buy homes; REIT revenues pressured |

| Utilities | Debt burden; rate sensitivity | Capital-intensive with high leverage; dividend yields less attractive |

| Consumer Discretionary | Reduced spending | Credit costs rise; consumers delay major purchases |

| Financial Services (Banks) | Mixed impact | Higher rates boost lending income but can reduce loan demand |

Technology stocks typically experience the most dramatic sell-offs during rate-hike cycles because their valuations rely heavily on earnings expected years in the future. The NASDAQ Composite fell 32% during the 2022 rate-hiking cycle—its worst year since 2008 (Yahoo Finance Historical Data, December 2022).

Real estate investment trusts (REITs) face dual pressure: higher rates increase their borrowing costs while simultaneously making real estate purchases less attractive to buyers. The Vanguard Real Estate ETF (VNQ) declined over 25% in 2022.

Sectors that Benefit from Higher Interest Rates

| Sector | Opportunity | Why It Works |

|---|---|---|

| Banks and Financial Institutions | Higher net interest margin | Banks earn more on loans; deposit rates rise more slowly |

| Industrials | Economic resilience plays | Often overlooked; benefit from infrastructure spending |

| Energy | Inflation hedge | Commodity prices often rise with rates; strategic importance |

| Healthcare | Defensive characteristics | Consistent demand regardless of economic conditions |

Banks historically outperform during rate-hike cycles because they can charge more for loans while their deposit costs rise more slowly. The KBW Bank Index rose 35% during the 2015-2018 hiking cycle despite broader market volatility (Keefe, Bruyette & Woods, December 2018).

Energy stocks often benefit because oil and gas prices tend to rise during periods of economic strength that precede rate hikes. Additionally, energy companies frequently have strong cash flows that become more valuable when discount rates increase.

The Discount Rate Effect: Why Today's Earnings Matter More

The mathematical relationship between interest rates and stock prices can be expressed through the discounted cash flow (DCF) model. While this sounds technical, understanding the basic principle helps you make better investment decisions.

Here's the simplified logic: A company expected to earn $100 five years from now is worth less when interest rates are 5% than when they're 2%. At a 2% discount rate, that $100 five years from now is worth about $90.70 today. At a 5% discount rate, it's worth only $78.35—a 14% reduction in present value.

This effect compounds across a company's entire stream of future earnings. For growth companies expected to generate the bulk of their profits 10, 15, or 20 years from now, even small rate increases can dramatically affect valuations.

The price-to-earnings (P/E) ratio—the most commonly cited stock valuation metric—implicitly reflects market expectations about interest rates. When rates fall, investors accept higher P/E ratios because future earnings are more valuable. When rates rise, P/E ratios typically compress.

Research from Goldman Sachs (2024) found that every 1 percentage point increase in the 10-year Treasury yield correlates with approximately a 15-20% compression in tech sector valuations, controlling for earnings growth.

Historical Examples: How the Stock Market Has Reacted to Rate Changes

The 2022 Rate Hiking Cycle

The most recent example of rates affecting the market provides valuable lessons. The Federal Reserve raised rates from near-zero in March 2022 to 5.25-5.50% by July 2023—the most aggressive tightening cycle since the 1980s.

The market response was severe but uneven:

- S&P 500: Fell 19.4% in 2022 (worst year since 2008)

- NASDAQ Composite: Dropped 32.5%, entering bear market territory

- Treasury bonds: Lost 13% (worst year on record)

- Gold: Gained 0.4% (served as inflation hedge)

However, the recovery was equally instructive. By late 2023 and into 2024, as investors began anticipating rate cuts, the market rallied sharply. The S&P 500 gained 24% in 2023 and another 23% in 2024, reaching new all-time highs (S&P Dow Jones Indices, December 2024).

The 2018 Rate Hike Cycle

In 2018, the Fed raised rates four times amid strong economic growth. The S&P 500 declined 6.2% in Q4 2018, leading the Fed to pause rate hikes in 2019. Following the pivot, the market surged 29% in 2019.

This demonstrates a key pattern: markets often recover quickly once it becomes clear the Fed has finished raising rates.

The 1995 "Soft Landing" Scenario

Perhaps the most celebrated Fed achievement came in 1995-1996, when then-Chair Alan Greenspan engineered a "soft landing"—raising rates enough to contain inflation without triggering a recession.

The S&P 500 rose 37% in 1995 despite rate increases, because the economy remained strong and investors believed the Fed had achieved the delicate balance. This scenario remains the模板 for what markets hope the current cycle can achieve.

How to Position Your Portfolio When Interest Rates Change

Understanding how interest rates affect stocks is only half the battle. Here's how to translate that knowledge into investment decisions:

During Rate-Hike Cycles

-

Reduce exposure to long-duration growth stocks: Focus on companies with proven cash flows today rather than promises of future earnings.

-

Consider financial sector stocks: Banks typically benefit from higher net interest margins.

-

Maintain defensive positions: Healthcare and consumer staples companies tend to hold up better because people need their products regardless of economic conditions.

-

Review fixed-income allocations: As rates rise, bond yields become more attractive. Consider increasing allocation to short-duration bonds, which are less sensitive to rate changes.

-

Hold cash strategically: Higher rates mean cash yields are more competitive. Money market funds and high-yield savings accounts offer returns not seen in decades.

During Rate-Cut Cycles

-

Reallocate to growth stocks: Lower rates make future earnings more valuable, benefiting growth and technology companies.

-

Reduce bank exposure: While banks may initially benefit from rate cuts, prolonged low rates compress net interest margins.

-

Consider real estate: REITs often rally as borrowing costs decline.

-

Review bond allocations: Falling rates mean existing bonds with higher yields appreciate in value.

Common Mistakes Investors Make Around Interest Rate Changes

Mistake #1: Reacting Too Late

Many investors wait until after the Fed announces a rate change to adjust their portfolio. By then, markets have typically already priced in the move. The Federal Reserve's Federal Reserve Beige Book and official statements provide advance signals—pay attention to the direction of policy, not just the announcement itself.

Mistake #2: Overreacting to Short-Term Volatility

The stock market has historically recovered from every rate-hiking cycle. Panic selling during volatility locks in losses and misses subsequent rebounds. Staying invested while making thoughtful adjustments typically outperforms trying to time the market.

Mistake #3: Ignoring the Signal in Bond Yields

The 10-year Treasury yield often provides clues about market expectations. When yields spike, it signals the market expects higher rates ahead. When yields fall, it suggests rate cuts are anticipated. These signals can help you position ahead of Fed actions.

Mistake #4: Chasing Dividend Yield Blindly

When rates rise, dividend yields become more attractive relative to bonds—but not all dividend stocks are equal. Companies maintaining dividends while cutting capital expenditures may be signaling financial weakness. Focus on dividend sustainability, not just yield.

Frequently Asked Questions

How do interest rate hikes affect my 401(k)?

Interest rate hikes typically cause your 401(k) to decline in the short term because stock prices fall. However, the impact varies significantly based on your allocation. If you're heavily weighted toward growth stocks, you'll see more dramatic declines. If you hold a mix of stocks, bonds, and defensive sectors, your portfolio will be more resilient. The key is to maintain a long-term perspective—historically, markets have recovered from every rate-hiking cycle.

Should I move my money to bonds when interest rates rise?

While bonds become more attractive as yields rise, moving entirely to bonds carries risks. If rates continue rising, bond prices fall. Additionally, stocks have historically outperformed bonds over longer periods. A balanced approach—gradually increasing bond allocation as rates rise, but maintaining stock exposure for long-term growth—typically serves investors best.

Which stocks perform best during high interest rate periods?

Financial sector stocks (particularly banks), energy companies, and healthcare companies often perform relatively well during high-rate periods. These sectors either benefit directly from higher rates (banks) or have business models less sensitive to interest rate changes (healthcare, energy). Avoid long-duration growth stocks and highly leveraged companies during rate-hike cycles.

How quickly does the stock market respond to interest rate changes?

The stock market typically begins pricing in rate changes before the Federal Reserve's official announcement. Research from the Chicago Booth Journal suggests markets respond most dramatically in the 24-48 hours surrounding Fed announcements, but pre-announcement positioning often accounts for much of the movement. This is why anticipating rate direction is more valuable than reacting to announcements.

What is the Federal Reserve's target interest rate currently?

As of January 2025, the Federal Reserve maintains its benchmark federal funds rate in the 4.25%-4.50% range. This follows a series of rate hikes from 2022-2023 and subsequent pauses throughout 2024. The Fed has signaled it will monitor economic data carefully before making further adjustments, emphasizing its data-dependent approach to monetary policy.

Should I buy stocks before or after interest rate changes?

Trying to time rate changes is extremely difficult and often counterproductive. Rather than speculating on Fed decisions, focus on building a diversified portfolio that can weather various rate environments. If you have a long investment horizon, maintaining consistent contributions (dollar-cost averaging) during volatility typically produces better results than attempting to time entry and exit points.

Conclusion: Navigating Interest Rates in Your Investment Strategy

The relationship between interest rates and the stock market is complex but predictable. Rate increases compress valuations, particularly for growth stocks, while rate cuts fuel market rallies. The Federal Reserve's monetary policy decisions create the environment in which your investments either thrive or struggle.

The most successful investors don't try to predict Fed moves perfectly. Instead, they build portfolios resilient enough to handle various rate scenarios. They maintain diversification across sectors, balance stocks with bonds appropriate for their risk tolerance and time horizon, and stay focused on long-term goals rather than short-term fluctuations.

As we move through 2025, the Fed's path remains data-dependent. Inflation trends, employment figures, and economic growth will guide their decisions. By understanding how interest rates affect stock valuations—and positioning your portfolio accordingly—you can make informed decisions that serve your financial goals regardless of where rates ultimately land.

Remember: the stock market has weathered every rate cycle in history. Those who maintain discipline and think long-term are best positioned to benefit when the cycle inevitably turns.

This article is for educational purposes and does not constitute financial advice. Consult a licensed financial advisor for investment decisions tailored to your specific circumstances.