Cryptocurrency taxation remains one of the most complex areas for US investors, with the Internal Revenue Service treating digital assets as property rather than currency. Understanding how to report your crypto transactions accurately can mean the difference between compliance and costly penalties.

This guide walks you through the essential steps for reporting cryptocurrency taxes, from identifying taxable events to filling out the required forms. Whether you're a casual investor or an active trader, you'll find actionable guidance to navigate this evolving tax landscape with confidence.

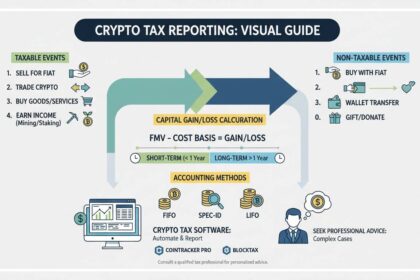

Understanding Cryptocurrency and Taxable Events

The IRS classifies cryptocurrency as property, meaning every transaction that results in a gain or loss triggers potential tax consequences. This classification, established in IRS Notice 2014-21 and reinforced in subsequent guidance, requires taxpayers to report crypto activities similar to how they would report stock or real estate transactions.

Not every cryptocurrency transaction qualifies as a taxable event. Understanding the distinction between taxable and non-taxable events forms the foundation of accurate reporting.

Taxable events include:

- Selling cryptocurrency for US dollars

- Trading one cryptocurrency for another (such as exchanging Bitcoin for Ethereum)

- Using cryptocurrency to purchase goods or services

- Receiving cryptocurrency as income from mining, staking, or rewards

- Gifting cryptocurrency exceeding the annual exclusion limit

Non-taxable events include:

- Purchasing cryptocurrency with US dollars and holding it

- Transferring cryptocurrency between your own wallets

- Donating cryptocurrency to qualified charitable organizations

- Gifting cryptocurrency up to the annual exclusion amount ($18,000 per recipient in 2024)

The distinction matters because many new cryptocurrency investors mistakenly believe that only cashing out to fiat currency triggers taxation. In reality, any exchange of value—whether to another cryptocurrency or to goods and services—can create a taxable event requiring reporting.

Calculating Your Capital Gains and Losses

Once you've identified your taxable events, calculating the capital gain or loss for each transaction becomes the next critical step. The calculation follows the same methodology used for traditional securities: proceeds minus cost basis equals gain or loss.

Cost Basis Methods

Your cost basis represents what you paid for the cryptocurrency, including any fees associated with the purchase. Several methods exist for calculating cost basis, and the method you choose affects your tax outcome.

First-in, first-out (FIFO) assumes you sell your oldest holdings first. This method often results in higher capital gains during bull markets because older coins typically cost less. Last-in, first-out (LIFO) sells your newest purchases first, which can minimize gains during rising markets but may trigger losses. Specific identification allows you to select which specific coins to sell, offering maximum control over tax outcomes but requiring detailed record-keeping.

Short-Term vs. Long-Term Gains

The holding period determines whether your gains receive short-term or long-term capital gains treatment. Assets held for one year or less generate short-term gains, taxed at ordinary income tax rates ranging from 10% to 37% depending on your income bracket. Assets held longer than one year qualify for long-term capital gains rates of 0%, 15%, or 20%.

For example, if you bought Bitcoin at $30,000 and sold it six months later at $45,000, the $15,000 gain qualifies as short-term capital gains. If you held that same Bitcoin for two years before selling, the same $15,000 gain would receive long-term capital gains treatment, potentially reducing your tax liability significantly.

Calculating Losses

Cryptocurrency investments that have decreased in value generate capital losses that can offset gains from other investments. If your total capital losses exceed your capital gains, you can offset up to $3,000 of ordinary income annually, with any remaining losses carried forward to future tax years.

This loss-harvesting strategy requires careful planning. Selling losing positions to offset gains makes sense, but remember that repurchasing the same or substantially identical cryptocurrency within 30 days triggers wash sale rules that disallow the tax loss deduction.

Required Tax Forms and Reporting

The IRS requires specific documentation when reporting cryptocurrency transactions. Understanding which forms you need and how to complete them ensures compliance and avoids potential audits.

Schedule D and Form 8949

Schedule D (Capital Gains and Losses) serves as the primary form for reporting cryptocurrency capital gains and losses. Before completing Schedule D, most taxpayers must first complete Form 8949 (Sales and Other Dispositions of Capital Assets), which details each individual transaction.

Form 8949 requires you to list every taxable cryptocurrency transaction, including the description of the asset, date acquired, date sold, proceeds, cost basis, and gain or loss. For active traders with hundreds or thousands of transactions, this requirement creates substantial administrative burden, which is why many investors use specialized cryptocurrency tax software.

Reporting Mining and Staking Income

Receiving cryptocurrency through mining or staking operations generates ordinary income at the fair market value of the coins on the day you received them. This income gets reported on Schedule 1 (Additional Income and Adjustments to Income) as "Other income" and also requires tracking the cost basis for potential capital gains when you eventually sell.

For example, if you mine Ethereum worth $5,000 in 2024, you report $5,000 as ordinary income on Schedule 1. If you later sell that Ethereum for $7,000, you report a $2,000 capital gain ($7,000 proceeds minus $5,000 cost basis).

Form 1099 Requirements

Cryptocurrency exchanges are not currently required to issue Form 1099 to customers for most transactions, though this could change with future IRS guidance. However, if you receive cryptocurrency as payment for goods or services from a business that issues Form 1099, you must report that income.

Record-Keeping Best Practices

Maintaining accurate records throughout the year simplifies tax reporting and protects you if the IRS questions your filings. The burden of proof falls on taxpayers, meaning you must demonstrate the accuracy of your reported transactions.

Essential Documentation

For each cryptocurrency transaction, maintain records showing the date and time of the transaction, the amount and type of cryptocurrency involved, the US dollar value at the time of the transaction, the purpose or reason for the transaction, and the wallet addresses or exchange account information.

This documentation becomes particularly important when calculating cost basis for transactions involving multiple purchases at different prices. Without clear records, determining which specific coins you sold—and their corresponding cost basis—becomes extremely difficult.

Tools and Software

Cryptocurrency tax software platforms aggregate transaction data from multiple exchanges and wallets, automatically calculating cost basis and generating the forms needed for filing. Popular options include CoinTracker, Koinly, and CryptoTaxCalculator. These platforms connect directly to exchange APIs, reducing manual entry errors and ensuring comprehensive transaction records.

However, software tools require accurate input data. Before tax season, verify that all transactions appear correctly and that cost basis calculations match your expectations. Discrepancies between exchange records and your tax software can create problems, so reconcile these records regularly.

Special Considerations for Different Investor Types

Your tax situation varies depending on how actively you trade cryptocurrency and whether you receive it as income.

Casual Investors

If you occasionally buy cryptocurrency and hold it for long periods, your tax obligations remain relatively straightforward. Report capital gains when you sell, and maintain records of your purchase price and date. Long-term capital gains rates likely apply to most of your transactions if you hold for more than one year.

Active Traders

Frequent traders face more complex reporting requirements. The IRS allows active traders to mark their cryptocurrency trading as a business activity, potentially allowing deductions for expenses and requiring reporting on Schedule C (Profit or Loss from Business) rather than Schedule D. This election requires substantial trading activity and should be discussed with a tax professional.

DeFi and NFT Transactions

Decentralized finance (DeFi) and non-fungible token (NFT) transactions create unique tax challenges. Lending your cryptocurrency to DeFi protocols generates taxable income. Swapping tokens on decentralized exchanges may trigger capital gains even when no fiat currency changes hands. NFT creators face ordinary income tax on primary sales and capital gains on resale royalties.

Common Mistakes to Avoid

Several frequent errors can trigger IRS attention or result in overpaying taxes.

Failing to Report All Transactions

The IRS has increased scrutiny on cryptocurrency reporting, and failure to report all transactions can trigger audits and penalties. Even transactions where you lost money must be reported to capture the tax loss deduction.

Ignoring Crypto-to-Crypto Trades

Many taxpayers mistakenly believe only selling cryptocurrency for cash triggers taxes. In reality, trading one cryptocurrency for another constitutes a taxable disposal, requiring you to calculate and report the capital gain or loss.

Inaccurate Cost Basis

Using incorrect purchase prices or failing to account for transaction fees in your cost basis results in incorrect gain calculations. Exchange records may not always match your actual cost basis, so maintain independent verification.

Forgetting About Income Events

Receiving airdrops, forks, or staking rewards creates taxable income at the fair market value on the date of receipt. Many investors overlook these events, leading to underreporting.

Frequently Asked Questions

Do I have to pay taxes on cryptocurrency if I didn't sell it?

No, simply holding cryptocurrency does not trigger taxation. Taxes arise when you dispose of cryptocurrency through selling, trading, or using it to make purchases. The disposal event creates a taxable moment where you must calculate any capital gain or loss based on the change in value from when you acquired the crypto.

What happens if I don't report my cryptocurrency transactions?

Failure to report cryptocurrency transactions can result in IRS penalties, including a 20% penalty for negligence or substantial understatement of income, and potentially criminal prosecution for intentional tax evasion. The IRS has been increasing enforcement efforts around cryptocurrency reporting, making compliance increasingly important.

Can I deduct my cryptocurrency losses?

Yes, capital losses from cryptocurrency investments can offset capital gains from other investments. If your losses exceed your gains, you can deduct up to $3,000 against ordinary income annually, with remaining losses carried forward to future tax years. This makes tax-loss harvesting a legitimate strategy for managing your overall tax liability.

How do I report cryptocurrency on my tax return?

Report cryptocurrency capital gains and losses on Schedule D and Form 8949. Report cryptocurrency received as income (from mining, staking, or payments) on Schedule 1 as "Other income." Specialized cryptocurrency tax software can help organize your transactions and generate the required forms.

Are cryptocurrency donations tax-deductible?

Yes, donating cryptocurrency to qualified charitable organizations can provide a double tax benefit. You receive a deduction for the fair market value of the donated crypto, and you avoid recognizing capital gains that would have resulted from selling the cryptocurrency. This makes charitable giving of appreciated cryptocurrency often more tax-efficient than selling and donating cash.

What records do I need to keep for cryptocurrency taxes?

Maintain records showing the date of each transaction, the amount of cryptocurrency involved, the US dollar value at the time of the transaction, the purpose of the transaction, and records of your original purchase price. Keep these records for at least seven years in case of IRS audit.

Conclusion

Navigating cryptocurrency taxation requires attention to detail and ongoing record-keeping throughout the year. Understanding taxable events, calculating capital gains and losses accurately, and filing the proper forms ensures compliance with IRS requirements while potentially minimizing your tax liability.

The tax landscape for cryptocurrency continues evolving, with the IRS implementing stricter reporting requirements and increased enforcement. Staying informed about changes and maintaining thorough records positions you for successful tax filing each year.

While this guide provides foundational knowledge for reporting cryptocurrency taxes, tax situations vary significantly based on individual circumstances. Consulting with a qualified tax professional who understands cryptocurrency taxation can help you optimize your tax strategy and ensure compliance with all applicable regulations.

Disclaimer: This article provides general informational content about cryptocurrency taxation and should not be considered tax advice. Tax laws are subject to change and vary based on individual circumstances. Consult with a licensed tax professional for personalized guidance regarding your specific situation.