Imagine receiving a check from a company you own a piece of—simply because you held onto your investment. That's essentially how dividends work. For investors seeking consistent returns without selling their shares, dividends represent a powerful mechanism for building wealth over time. This guide breaks down everything you need to know about dividends, from the basic mechanics to strategies for maximizing your passive income.

What Are Dividends?

A dividend is a portion of a company's profits distributed directly to its shareholders. When a corporation earns money, its board of directors decides whether to reinvest those profits back into the business or share them with investors. Dividends are that sharing mechanism—a cash payment (or sometimes stock) awarded to people who own shares in the company.

Not all companies pay dividends. Growth-focused companies like Amazon and Google historically reinvest their profits to expand operations, while established corporations in industries like utilities, banking, and consumer goods often distribute regular dividends. The payment is voluntary; companies can reduce or eliminate dividends if financial conditions change, though dividend cuts are typically viewed negatively by investors.

Dividends represent tangible returns on your investment beyond any potential stock price appreciation. If you own 100 shares of a company paying a $1 per share dividend, you receive $100 simply for holding those shares through the payment date.

How Dividends Actually Work

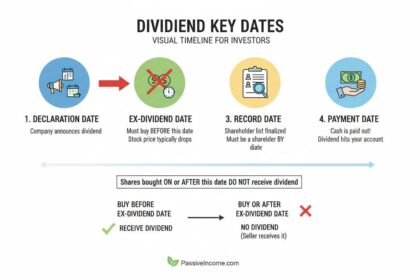

The dividend process follows a specific timeline with several key dates every investor should understand.

Declaration Date: The day the company's board announces the dividend, including the amount and payment schedule. This is when you first learn a dividend is being issued.

Ex-Dividend Date (Ex-Date): This is the critical deadline. If you purchase shares on or after this date, you won't receive the upcoming dividend. Conversely, if you own shares before the ex-date, you're entitled to the payment. The ex-date typically occurs about two business days before the record date.

Record Date: The date the company determines which shareholders are eligible to receive the dividend. Your brokerage must have you listed as the owner by this date.

Payment Date: The actual day when dividends are distributed to eligible shareholders. This usually happens 2-4 weeks after the declaration date.

Understanding these dates matters because stock prices often drop by approximately the dividend amount on the ex-date—reflecting that the stock no longer includes the upcoming payment. This creates opportunities for traders but doesn't fundamentally change the value proposition for long-term investors.

Types of Dividends

Companies can distribute dividends in several forms, though cash is most common.

Cash Dividends: The straightforward approach—companies send shareholders a check or deposit funds directly into brokerage accounts. Most dividend investors prefer this format for the flexibility it provides.

Stock Dividends: Instead of cash, shareholders receive additional shares of the company. A 5% stock dividend means you gain 5% more shares, though the price per share typically adjusts accordingly. This increases your ownership stake without requiring additional investment.

Special Dividends: One-time payments, often resulting from unusual circumstances like asset sales or exceptionally profitable years. These aren't expected to continue and shouldn't form the basis of income planning.

Qualified vs. Non-Qualified Dividends: The tax treatment differs based on how long you've held the stock. Qualified dividends receive lower capital gains tax rates, while non-qualified dividends are taxed as regular income. Holding shares for more than 60 days before the ex-date typically qualifies them for preferential treatment.

Understanding Dividend Yield and Payout Ratios

Dividend yield expresses the annual dividend as a percentage of the stock's current price. If Company A pays $4 annually in dividends and trades at $100 per share, the yield is 4%. A $50 stock paying the same $4 dividend yields 8%—meaning you earn more income per dollar invested.

The formula is straightforward: Annual Dividend Per Share ÷ Stock Price × 100 = Dividend Yield

However, yield alone tells an incomplete story. A high yield might indicate an undervalued stock or, alarmingly, a company struggling with financial difficulties. Context matters significantly.

The payout ratio reveals what percentage of earnings a company uses for dividends. A 60% payout ratio means 60% of profits go to shareholders while 40% remains reinvested. Generally, payout ratios below 60% suggest sustainability, while ratios above 80% may signal vulnerability during economic downturns.

| Metric | What It Tells You | Healthy Range |

|---|---|---|

| Dividend Yield | Income return on investment | 2-5% typically sustainable |

| Payout Ratio | Dividend sustainability | Below 60% preferred |

| Dividend Growth | Company strength over time | Consistent annual increases |

The Power of Dividend Reinvestment (DRIP)

Dividend reinvestment programs automatically use dividend payments to purchase additional shares, compounding your returns over time. This seemingly simple mechanism creates exponential growth potential.

Consider an initial $10,000 investment in a company paying 4% annual dividends with 5% annual stock price appreciation. After 20 years without reinvesting, your investment grows to approximately $26,000. With dividend reinvestment, that same initial investment grows to roughly $38,000—a difference of nearly 50%.

The mathematics works because each reinvested dividend purchases more shares, which then generate their own dividends. Over decades, this snowball effect dramatically increases your total return. Many brokerage firms and dividend reinvestment plans (DRIPs) offer this feature commission-free.

Benefits of Dividend Investing

Dividend investing offers several advantages that make it attractive for building long-term wealth.

Passive Income Stream: Once you build a substantial portfolio, dividends can provide meaningful income without selling assets. Many retirees use dividend portfolios to supplement Social Security and pensions.

Lower Volatility: Dividend-paying stocks tend to be less volatile than growth stocks. During market downturns, investors often gravitate toward reliable dividend payers, providing price support.

Inflation Hedge: Companies that consistently increase dividends often outpace inflation. The "Dividend Aristocrats"—companies that have increased dividends for 25+ consecutive years—typically raise payments faster than inflation rates.

Psychological Discipline: Regular dividend payments encourage holding investments long-term rather than chasing short-term trades. The cash distributions provide tangible returns while waiting for capital appreciation.

Historical data supports dividend strategy effectiveness. Between 1930 and 2023, dividends contributed approximately 40% of the total returns in the S&P 500. During the 2008 financial crisis, dividend-paying stocks outperformed non-payout stocks by roughly 10 percentage points in the subsequent recovery.

Risks and Important Considerations

Dividend investing isn't without risks that beginners must understand.

Dividend Cuts: Companies can reduce or eliminate dividends during economic downturns. During the 2020 pandemic, dozens of companies suspended dividends, demonstrating that payouts aren't guaranteed. Financial health analysis helps identify sustainable dividend payers.

Interest Rate Sensitivity: When interest rates rise, dividend-paying stocks often decline as investors shift to safer fixed-income investments. Conversely, falling rates typically boost dividend stocks.

Overconcentration Risk: Focusing too heavily on high-yield sectors (like utilities or real estate investment trusts) exposes your portfolio to industry-specific downturns. Diversification across sectors provides crucial protection.

Tax Implications: Non-qualified dividends are taxed as ordinary income, which may be higher than capital gains rates. Tax-advantaged accounts like IRAs and 401(k)s shelter dividend income from immediate taxation.

How to Start Investing in Dividend Stocks

Building a dividend portfolio requires a systematic approach.

Step 1: Define Your Goals. Determine whether you want immediate income, long-term growth, or a combination. Younger investors might prioritize dividend growth (increasing payments over time), while retirees often need higher current yields.

Step 2: Open a Brokerage Account. Look for brokerages offering commission-free stock trading and dividend reinvestment options. Major platforms like Fidelity, Schwab, and Vanguard all provide these features.

Step 3: Start with Index Funds. Dividend-focused index funds provide instant diversification. The Vanguard Dividend Appreciation ETF (VIG) and iShares Select Dividend ETF (DVY) offer broad exposure to quality dividend payers.

Step 4: Research Individual Stocks. For those wanting to pick specific companies, analyze financial health metrics: consistent earnings, manageable debt levels, and sustainable payout ratios. Look for companies with "dividend champions"—at least 25 years of consecutive dividend increases.

Step 5: Build Gradually. Dollar-cost averaging—investing fixed amounts regularly—reduces timing risk. Reinvest dividends automatically to accelerate compounding.

Step 6: Monitor and Adjust. Review your portfolio quarterly, checking that companies maintain healthy payout ratios and continue growing dividends. Remove companies showing signs of financial distress.

Frequently Asked Questions

How much money do I need to start investing in dividends?

You can start with any amount. Many brokerages allow purchasing fractional shares, meaning you can invest $50 or $100 in dividend-paying stocks. Some DRIP programs require minimum initial investments as low as $10. Starting early matters more than starting big—time compounds your returns.

Are dividends guaranteed every quarter?

No, dividends are not guaranteed. Companies can reduce or eliminate dividends at any time. While blue-chip dividend stocks with long histories of payments are more reliable, no dividend is absolutely safe. Focus on companies with strong balance sheets and sustainable payout ratios to minimize this risk.

What's the difference between dividend yield and dividend growth?

Dividend yield measures current income relative to stock price—a 4% yield means $4 in annual dividends per $100 invested. Dividend growth tracks annual increases in the dividend amount itself. Growth-focused investors often prefer companies raising dividends consistently, even with lower initial yields, because rising payments compound significantly over time.

Can I live off dividend income?

Yes, it's possible to generate meaningful income through dividends, but it requires substantial capital. A $1 million portfolio yielding 4% produces $40,000 annually. Building such a portfolio typically takes decades of consistent investing, though the combination of dividend payments and reinvestment accelerates the process. Many retirees use dividend income as a supplement to other retirement sources.

Do I have to pay taxes on dividends?

Yes, dividends are generally taxable. Qualified dividends receive preferential capital gains tax rates (0%, 15%, or 20% depending on your income). Non-qualified dividends are taxed as ordinary income. Holding dividend stocks in tax-advantaged accounts like IRAs or 401(k)s defers or eliminates these tax obligations.

How often are dividends paid?

Most U.S. companies pay dividends quarterly, though some pay monthly, semi-annually, or annually. The payment schedule affects your cash flow planning. Monthly dividend stocks exist but are less common—often coming from real estate investment trusts (REITs) or closed-end funds.

Conclusion

Dividends represent one of the most reliable paths to building passive income through investing. By understanding how dividends work—the key dates, types, yields, and payout metrics—you can make informed decisions about building a dividend portfolio aligned with your financial goals. Start with low-cost index funds for diversification, reinvest dividends to maximize compounding, and gradually add individual quality companies as your knowledge expands. The magic of dividend investing lies in patience: consistent contributions and time create substantial wealth that cash payments alone cannot achieve.