Understanding how money grows over time is one of the most important financial concepts anyone can learn. Compound interest, often called the "eighth wonder of the world" by financial experts, represents the mechanism through which your money generates earnings on top of earnings. This comprehensive guide explains exactly how does compound interest work, why it matters for your financial future, and how you can harness its power to build wealth.

What Is Compound Interest?

Compound interest is the interest calculated on both the initial principal and the accumulated interest from previous periods. Unlike simple interest, which is computed only on the original amount of money, compound interest allows your earnings to snowball over time. This fundamental difference is what makes compounding such a powerful wealth-building tool.

When you deposit money into a savings account or invest in certain financial instruments, you earn interest on your balance. With compound interest, that interest gets added to your principal, meaning that in the next compounding period, you earn interest on a larger amount. This cycle continues, creating an exponential growth pattern that accelerates over time.

The frequency of compounding periods can vary significantly. Some accounts compound annually, meaning interest is calculated and added once per year. Others compound quarterly, monthly, or even daily. The more frequently interest compounds, the faster your money grows, assuming all other factors remain equal.

Financial advisors consistently emphasize that understanding compound interest is essential for anyone looking to build long-term wealth. "Compound interest is the foundation of successful investing," says Sarah Mitchell, a certified financial planner based in Chicago. "It's the mechanism that transforms modest regular contributions into substantial nest eggs over decades."

The Formula Behind Compound Interest

To fully grasp how does compound interest work, it helps to understand the mathematical formula that drives this process. The standard compound interest formula is:

A = P(1 + r/n)^(nt)

Where:

- A = the future value of the investment or loan

- P = the principal investment amount

- r = annual interest rate (as a decimal)

- n = number of times interest compounds per year

- t = number of years the money is invested

This formula reveals why starting early is so crucial. Even small differences in your starting age or contribution amounts can lead to dramatically different outcomes over long periods.

For example, consider an initial investment of $10,000 earning 7% annual interest over 30 years. With annual compounding, the formula would calculate: $10,000 × (1 + 0.07/1)^(1×30) = $76,122.55. The same investment with monthly compounding would yield: $10,000 × (1 + 0.07/12)^(12×30) = $81,164.86. While the difference may seem modest initially, it becomes more pronounced with larger principal amounts and longer time horizons.

Understanding this formula empowers you to make informed decisions about where to place your money and what returns you might realistically expect. Many online calculators are available to help visualize these calculations, but knowing the underlying mathematics provides valuable context.

How Does Compound Interest Work Over Time?

The true power of compound interest becomes most apparent when examining its effects over extended periods. The growth trajectory follows a curve that starts gradually but accelerates dramatically in later years. This phenomenon is sometimes called the "miracle of compounding."

To illustrate, imagine investing $5,000 annually into an account earning 8% interest. After 10 years, your total contributions would be $50,000, but your account balance would be approximately $78,227—meaning you earned $28,227 in interest. After 20 years, your balance would grow to approximately $247,115, with interest accounting for nearly $147,000 of that total. By year 30, your balance would reach approximately $612,000, with interest comprising roughly $462,000 of that amount.

This progression demonstrates why time is the most critical factor in compounding. The earlier you start investing, the more time your money has to grow. Waiting even a few years can significantly impact your final results.

The concept works equally in reverse when dealing with debt. Credit cards and loans that use compound interest can cause balances to grow substantially if minimum payments are not maintained. This is why understanding how does compound interest work is crucial for managing both investments and debts effectively.

Compound Interest vs. Simple Interest

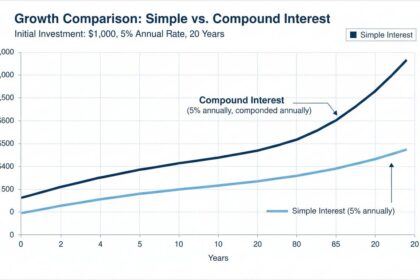

To fully appreciate compound interest, it's helpful to contrast it with simple interest. The distinction between these two calculation methods can mean thousands of dollars over time.

Simple interest is calculated only on the original principal amount. For instance, a $10,000 investment at 5% simple interest would earn $500 annually, totaling $2,500 in interest over five years. The balance would remain at $12,500 throughout the entire period.

Compound interest, by contrast, calculates interest on both principal and accumulated interest. Using the same $10,000 at 5% compounded annually, the first year would earn $500, the second year would earn $525 (5% of $10,500), and so forth. After five years, the total interest earned would be approximately $2,762, resulting in a balance of $12,762.

The difference may appear small in these examples, but it becomes substantial over longer periods and with larger amounts. For a $100,000 investment at 6% over 25 years, simple interest would generate $150,000 in total interest, while compound interest would generate approximately $329,000—more than double.

Most savings accounts, certificates of deposit, and investment vehicles use some form of compound interest. Always verify the compounding frequency when evaluating financial products, as this directly affects your returns.

Examples of Compound Interest in Real Life

Compound interest manifests in numerous financial products and situations that consumers encounter regularly. Understanding these applications helps you recognize opportunities to benefit from compounding.

Savings Accounts: Traditional savings accounts typically offer compound interest, usually compounded daily or monthly. While interest rates have been historically low in recent years, these accounts provide a safe place to earn modest returns while maintaining liquidity.

Certificates of Deposit (CDs): CDs offered by banks and credit unions often provide higher interest rates than regular savings accounts. These time deposits typically compound interest on a monthly or annual basis, with penalties for early withdrawal.

Retirement Accounts: 401(k) plans and Individual Retirement Accounts (IRAs) benefit enormously from compound interest. The tax-advantaged nature of these accounts allows investments to grow faster than in taxable accounts. Employer matching contributions further accelerate this growth.

Stock Market Investments: While not technically compound interest, stock market returns compound through capital appreciation and dividend reinvestment. Reinvesting dividends to purchase additional shares creates a compounding effect similar to interest earned on savings.

Education Savings: 529 plans and Coverdell accounts for education expenses grow through compound interest, helping families accumulate funds for future educational costs.

Factors That Affect Compound Interest

Several key variables determine how effectively your money compounds over time. Understanding these factors allows you to optimize your financial strategy.

Interest Rate: The annual interest rate or rate of return is perhaps the most obvious factor. Higher rates lead to faster growth, though higher returns typically come with increased risk. Finding the right balance between safety and growth potential is essential.

Time Horizon: As demonstrated earlier, time is the most powerful variable in the compounding equation. Starting investments early, even with smaller amounts, often produces better results than starting later with larger contributions.

Compounding Frequency: The number of times interest is calculated and added annually affects growth. Daily compounding produces the highest returns, followed by monthly, quarterly, and annually. Many online tools can help you compare different compounding frequencies.

Regular Contributions: Adding money to your investments consistently amplifies the compounding effect. Each new contribution itself begins compounding, creating multiple compounding cycles working simultaneously.

Taxes and Fees: Investment fees and taxes can significantly reduce your effective returns. Tax-advantaged accounts like IRAs and 401(k)s allow your money to compound more efficiently by deferring or eliminating annual tax obligations.

Tips to Maximize Compound Interest

Implementing strategies to maximize the power of compound interest can substantially improve your long-term financial outcomes.

Start Early: The single most effective strategy is to begin investing as soon as possible. Even starting five or ten years earlier can result in significantly larger balances at retirement.

Be Consistent: Regular contributions, whether monthly or annually, keep the compounding cycle working. Automated contributions remove the temptation to skip payments and ensure steady growth.

Reinvest Earnings: Rather than spending interest or dividend payments, reinvest them to keep the compounding cycle active. Many brokerage accounts offer automatic dividend reinvestment programs.

Seek Competitive Rates: Regularly evaluate whether your savings and investment accounts are offering competitive rates. Moving money to better-paying accounts can accelerate growth without increasing risk.

Minimize Fees: High investment fees eat into your returns and reduce compounding's effectiveness. Choose low-cost index funds and ETFs when possible, and compare fee structures across financial products.

Let Time Work: Resist the urge to tap into long-term investments for short-term needs. Maintaining consistent time horizons allows compounding to work its magic.

Conclusion

Compound interest represents one of the most powerful forces in personal finance. Whether you're saving for retirement, building an emergency fund, or paying down debt, understanding how does compound interest work fundamentally changes how you approach money management. The exponential growth it creates can transform modest, consistent efforts into substantial wealth over time.

The key takeaways are straightforward: start investing early, be consistent with contributions, seek competitive rates, and minimize fees. By implementing these principles, you position yourself to benefit from compounding rather than become victim to it when dealing with debt. The mathematics of compound interest are relentless but predictable—your financial decisions determine whether they work for you or against you.

Frequently Asked Questions

How does compound interest differ from simple interest?

Simple interest is calculated only on the original principal amount, while compound interest is calculated on both the principal and the accumulated interest. This means compound interest grows faster over time because you earn interest on your interest.

How often does compound interest typically compound?

Compounding frequency varies by financial product. Savings accounts often compound daily or monthly, while CDs may compound monthly or annually. The more frequent the compounding, the faster your money grows.

Can compound interest work against me?

Yes, compound interest can work against you when you have debts like credit card balances. Unpaid balances accumulate interest on interest, causing debt to grow rapidly if minimum payments aren't made. This is why paying off high-interest debt quickly is financially advantageous.

How long does it take for compound interest to significantly increase my money?

The impact of compound interest becomes more noticeable over periods of 10 years or more. While short-term growth may seem modest, the exponential curve means that most of the growth occurs in later years, making long-term investing crucial.

What is the best account type for benefiting from compound interest?

Tax-advantaged retirement accounts like 401(k)s and IRAs are often the best vehicles for compound growth because they allow your money to grow without annual tax withdrawals. High-yield savings accounts and CDs are good options for safer, more liquid savings.

How do I calculate compound interest for my specific situation?

You can use the formula A = P(1 + r/n)^(nt) to calculate compound interest, or use one of many free online calculators that allow you to input your principal, interest rate, compounding frequency, and time horizon to see projected growth.