Compound interest is one of the most important concepts in personal finance and investing. It's the mechanism by which interest earns interest, creating a snowball effect that can grow wealth significantly over time. Understanding how it works is essential for anyone building long-term financial security.

Understanding Compound Interest

Compound interest is interest calculated on the initial principal of a deposit or loan, plus all of the accumulated interest from previous periods. Unlike simple interest, which is computed only on the principal amount, compound interest takes into account the interest that has already been earned or charged, making your money work harder for you.

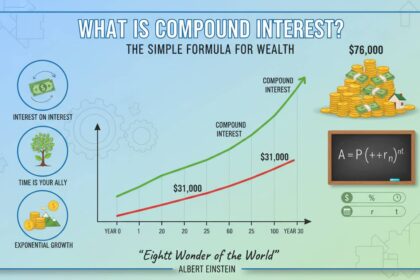

The formula for calculating compound interest is A = P(1 + r/n)^(nt), where:

- A is the future value of the investment

- P is the principal investment amount

- r is the annual interest rate expressed as a decimal

- n is the number of times interest compounds per year

- t is the number of years the money remains invested

This formula explains why starting early is so advantageous: the longer your money compounds, the more substantial the eventual returns.

Here's a practical example. If you invest $10,000 in an account earning 7% annual interest compounded annually, that investment will grow to approximately $19,672 after ten years, $38,697 after twenty years, and nearly $76,123 after thirty years—without adding a single additional dollar to the principal.

Simple Interest vs. Compound Interest

To appreciate compound interest fully, it helps to understand how it differs from simple interest. Simple interest is calculated using only the original principal amount. If you deposited $10,000 at a 7% simple interest rate, you would earn $700 per year, totaling $7,000 in interest over ten years, bringing your total to $17,000.

Compound interest accelerates wealth because each period's interest is calculated on the growing balance rather than just the original principal. Using the same $10,000 at 7% compounded annually, you would earn $700 in the first year, but $749 in the second year, $801 in the third, and so forth. Over ten years, compound interest would yield approximately $9,672 in total interest, compared to $7,000 with simple interest. The difference becomes more pronounced over longer time periods and higher interest rates.

This distinction matters for borrowers too. Credit cards and many loans use compound interest, which is why carrying a balance can lead to rapidly escalating debt.

The Rule of 72

The Rule of 72 is a quick way to estimate how long it takes for an investment to double at a given interest rate. Divide 72 by the annual interest rate to estimate the years required to double your money. At a 6% annual return, an investment would double in approximately twelve years. At an 8% return, the doubling time shrinks to nine years.

This rule helps visualize the power of compound interest without complex calculations. It also shows why small differences in annual returns can produce dramatically different long-term outcomes. An investor earning 6% versus 8% annually may seem like a minor difference, but over thirty years, that 2% gap could mean the difference between doubling money four times versus five times.

You can also use the Rule of 72 in reverse. If you want to double your money in ten years, you would need an annual return of approximately 7.2%.

How Compound Interest Benefits Long-Term Investors

The true power of compound interest emerges over extended time periods, making it essential for retirement planning. Tax-advantaged retirement accounts such as 401(k) plans and IRAs harness compound interest to help Americans build retirement savings.

Consider the impact of consistent contributions combined with compound returns. A thirty-year-old who invests $500 monthly in an account earning an average 7% annual return would contribute $180,000 over twenty-five years but accumulate approximately $405,000 by age fifty-five. The $225,000 difference represents compound interest working for the investor.

Employer-sponsored 401(k) plans often include matching contributions, providing guaranteed returns that compound tax-deferred. This combination of compound interest, employer matching, and tax advantages creates a powerful wealth-building tool. Starting early—even with smaller amounts—typically produces superior results compared to beginning larger investments later in life.

Dividend reinvestment programs demonstrate another application of compound interest. When investors use dividend payments to purchase additional shares, those new shares generate their own dividends, creating a compounding cycle. Many dividend-focused mutual funds and ETFs automate this process.

Compound Interest Works Against Borrowers Too

While compound interest helps investors build wealth, it works just as effectively against borrowers. Credit card debt is the most common example, with many cards compounding interest daily or monthly at annual rates exceeding 20%.

The mathematics of compound debt can quickly become overwhelming. A $5,000 credit card balance at 20% annual interest, with no payments made, would grow to approximately $12,909 after five years and $33,445 after ten years. This reality underscores why paying more than the minimum payment on high-interest debt matters.

Mortgages and auto loans typically use amortization schedules where early payments go primarily toward interest rather than principal. Understanding this structure helps borrowers make informed decisions about extra payments. By paying additional amounts toward principal, borrowers can reduce total interest paid over the life of the loan.

Student loans, another significant source of debt for millions of Americans, also use compound interest structures. Federal student loans have fixed interest rates, but private student loans may carry variable rates that can increase over time.

Strategies to Maximize Compound Interest

Investors can take several steps to maximize compound interest benefits:

Start investing as early as possible, even with small amounts. The compound effect requires time to work, making early participation the most significant advantage.

Maintain consistent contributions regardless of market conditions. Dollar-cost averaging—investing fixed amounts at regular intervals—takes advantage of market fluctuations by purchasing more shares when prices are low and fewer when prices are high.

Reinvest all returns rather than spending interest or dividend payments. Reinvestment amplifies the compounding cycle. Many brokerage accounts offer automatic dividend reinvestment programs.

Seek accounts with favorable interest rates and low fees. Small differences in annual returns—such as 0.5% or 1%—can produce meaningful differences in long-term outcomes. High fees eat into returns and reduce the effective compound growth rate.

Consider tax-advantaged accounts that allow investments to grow tax-deferred or tax-free. Traditional IRAs and 401(k) plans provide tax-deferred growth, while Roth versions offer tax-free growth on qualified withdrawals.

A Brief History

The concept of compound interest dates back to ancient civilizations. Roman law originally prohibited compound interest, viewing it as exploitative, though merchants found ways around these restrictions. Medieval and Renaissance thinkers debated the morality of interest lending, eventually establishing the framework for modern banking.

Benjamin Franklin famously used compound interest to build lasting legacies. He left stipulations in his will that funded libraries and hospitals in Philadelphia and Boston, demonstrating how compound interest could multiply charitable intentions over generations.

Frequently Asked Questions

What is compound interest in simple terms?

Compound interest is interest calculated on both the original principal and the accumulated interest from previous periods. Your interest earns its own interest, creating exponential growth over time rather than linear growth.

How is compound interest different from simple interest?

Simple interest is calculated only on the original principal amount, while compound interest is calculated on the principal plus all previously earned interest. This makes compound interest significantly more powerful for investments and more dangerous for debt.

How do I calculate compound interest?

The basic formula is A = P(1 + r/n)^(nt), where A is the future value, P is the principal, r is the annual interest rate, n is the number of times interest compounds per year, and t is the number of years. Online calculators make this process much easier.

How long does it take for compound interest to double my money?

Using the Rule of 72, divide 72 by your annual interest rate. At a 7% return, your money doubles approximately every 10.3 years. At 10%, it doubles approximately every 7.2 years.

Is compound interest always beneficial?

Compound interest works for investors but against borrowers. While it helps savings and investments grow, it also causes debt to escalate quickly if not managed properly.

What is the best way to benefit from compound interest?

Start investing early, contribute consistently, reinvest all returns, minimize fees, and use tax-advantaged accounts. Time is the most critical factor—early participation is the most powerful strategy for building long-term wealth.