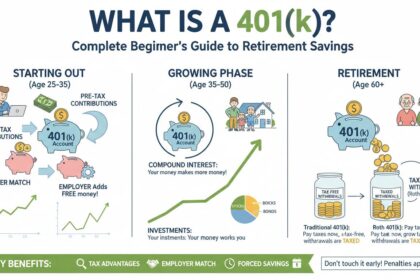

A 401k is an employer-sponsored retirement savings plan that allows workers to save and invest a portion of their paycheck before taxes are taken out. These plans represent one of the most powerful tools Americans have for building long-term wealth, offering tax advantages that can significantly accelerate retirement savings compared to regular taxable accounts.

Key Insights

- 401k plans allow pre-tax contributions that reduce taxable income

- Employers may match a portion of employee contributions

- Traditional and Roth 401k options provide different tax benefits

- 2024 contribution limits stand at $23,000 for workers under 50

- Over 60 million Americans actively participate in 401k plans

Understanding the Fundamentals of a 401k

The 401k derives its name from the section of the U.S. Internal Revenue Code that established these retirement plans. Originally created in 1978 as part of the Revenue Act, these plans revolutionized retirement savings by shifting responsibility from employers to individual workers. Unlike traditional pensions where companies guaranteed retirement payments, 401k plans put individuals in control of their financial future.

When you enroll in a 401k, a predetermined percentage of your paycheck gets deposited directly into your retirement account before taxes. This pre-tax treatment means your taxable income decreases by the amount you contribute, potentially moving you into a lower tax bracket. For example, if you earn $60,000 annually and contribute $6,000 to your 401k, you only pay taxes on $54,000 of income.

Your employer may also contribute to your account through matching. Many companies offer to match a percentage of your contributions, typically ranging from 3% to 6% of your salary. This match represents free money that can dramatically increase your total retirement savings over time.

How 401k Investments Grow Over Time

The money in your 401k doesn't sit idle—it gets invested in a selection of funds you choose from options provided by your plan. These investment options typically include stock mutual funds, bond funds, target-date funds, and sometimes company stock.

The power of compound interest makes 401k accounts particularly effective for long-term retirement planning. When your investment earnings generate their own returns, those returns also begin earning returns. Over decades of saving, this compounding effect can transform modest monthly contributions into substantial retirement nest eggs.

Growth Projection Example:

| Starting Age | Monthly Contribution | Annual Return | Value at Age 65 |

|---|---|---|---|

| 25 | $300 | 7% | $610,000 |

| 25 | $500 | 7% | $1,017,000 |

| 35 | $500 | 7% | $447,000 |

| 45 | $500 | 7% | $173,000 |

This table demonstrates why starting early significantly impacts final retirement savings. Someone who begins saving at 25 accumulates nearly four times more than someone who starts at 45, even though the older contributor would need to save nearly double the monthly amount to catch up.

Traditional vs. Roth 401k: Understanding Your Options

Most employers offer two types of 401k plans: Traditional and Roth. The fundamental difference lies in when you pay taxes on your money.

Traditional 401k:

Contributions reduce your current taxable income. You pay taxes on both contributions and investment earnings when you withdraw money in retirement. Since most people are in a lower tax bracket during retirement, this deferral creates potential tax savings.

Roth 401k:

Contributions are made with after-tax dollars, meaning you pay taxes now but withdraw everything tax-free in retirement. This option proves particularly beneficial for younger workers who expect to be in a higher tax bracket during retirement.

| Feature | Traditional 401k | Roth 401k |

|---|---|---|

| Tax on Contributions | Deductible now | Paid now |

| Tax on Withdrawals | Paid in retirement | Free |

| Required Distributions | Must start at age 73 | No lifetime requirement |

| Best For | Higher tax bracket now | Lower tax bracket now |

Some employers now allow workers to contribute to both types simultaneously, providing flexibility to hedge against uncertain future tax rates.

2024 and 2025 Contribution Limits and Rules

The Internal Revenue Service sets annual contribution limits for 401k plans, adjusting these figures periodically to account for inflation.

2024 Limits:

- Standard contribution: $23,000

- Catch-up contribution (age 50+): $7,500

2025 Limits:

- Standard contribution: $23,500

- Catch-up contribution (age 50+): $7,500

Employees aged 60-63 can make additional catch-up contributions of $11,000 starting in 2025 under SECURE 2.0 Act provisions.

Total employer and employee contributions cannot exceed $69,000 for 2024 ($76,500 for those 50+). These limits ensure that tax-advantaged retirement accounts benefit workers across income levels rather than disproportionately favoring the wealthy.

Employer Matching: Maximizing Free Money

Employer matching represents one of the most valuable benefits of 401k participation, yet millions of workers fail to capture these contributions fully. Understanding your employer's matching policy can mean the difference between a comfortable retirement and financial struggle.

Common matching structures include:

Dollar-for-dollar match: Your employer matches every dollar you contribute up to a certain percentage of your salary.

Percentage match: Your employer matches a percentage of your contributions, often with a vesting schedule.

Profit sharing: Employers contribute a percentage of company profits to employee accounts regardless of employee contributions.

The absolute minimum strategy: Contribute enough to your 401k to receive your full employer match. Anything less means turning down free money. If your employer matches 3% of your salary and you contribute nothing, you're essentially rejecting a 3% raise that could grow substantially over your career.

Vesting: Understanding Your True Retirement Balance

Vesting determines when you fully own employer contributions to your 401k. While you always own your personal contributions and their earnings, employer matches may require several years of employment before becoming yours completely.

Vesting Schedems:

| Years of Service | Cliff Vesting | Graded Vesting |

|---|---|---|

| 1 Year | 0% | 20% |

| 2 Years | 0% | 40% |

| 3 Years | 100% | 60% |

| 4 Years | 100% | 80% |

| 5 Years | 100% | 100% |

If you leave your job before becoming fully vested, you forfeit the unvested portion of employer contributions. Understanding your vesting schedule helps inform career decisions and prevents unpleasant surprises when changing employers.

Common 401k Mistakes to Avoid

Many workers inadvertently sabotage their retirement savings through preventable mistakes. Learning what not to do proves equally important as understanding contribution limits and investment options.

Mistake #1: Not Enrolling in Your Plan

Approximately 30% of eligible workers fail to enroll in their employer's 401k plan. Some simply procrastinate while others believe they cannot afford contributions. Even starting with 1-2% of salary creates momentum and captures any available employer match.

Mistake #2: Selecting Too Conservative Investments

Young workers often choose overly conservative investments like bond funds or stable value accounts when they should embrace stock market growth potential. With decades until retirement, the volatility of equities presents opportunity rather than risk.

Mistake #3: Borrowing from Your 401k

While 401k loans allow borrowing against your balance, they interrupt compounding, require repayment with after-tax dollars, and become due immediately if you leave your job. Many financial advisors recommend avoiding these loans except for true emergencies.

Mistake #4: Ignoring High Fees

401k plans vary significantly in their administrative fees and investment expense ratios. High-cost funds can erode thousands of dollars from your portfolio over decades. Review your plan's fee disclosure and select low-cost index funds when available.

How to Enroll and Start Building Your 401k

Enrolling in your employer's 401k typically takes less than fifteen minutes and requires only a few decisions.

Step 1: Access Your Enrollment Portal

Your human resources department or benefits administrator provides access to your plan's enrollment website. Many employers auto-enroll new hires at a default contribution rate, which you can adjust.

Step 2: Designate Your Contribution Percentage

Decide how much of each paycheck you want to contribute. Financial experts recommend starting at minimum and gradually increasing by 1% each year until reaching 15-20% of income. Even small starting amounts compound significantly over time.

Step 3: Choose Your Investments

Select from available investment options based on your risk tolerance and timeline. Target-date funds offer an automatic solution—choose the fund with your expected retirement year, and the fund automatically adjusts its allocation over time.

Step 4: Designate Beneficiaries

Name beneficiaries who will receive your 401k assets if you pass away. This is especially important for married individuals, as spousal consent may be required to designate someone else.

When Changing Jobs: What Happens to Your 401k

Leaving an employer creates several options for your existing 401k balance:

Roll over to a new employer's plan: If your new company offers a 401k, you can transfer your old balance there while maintaining tax-deferred status.

Roll over to an Individual Retirement Account (IRA): Directing your 401k to a traditional IRA provides more investment options and typically lower fees. This option works well when you don't have access to a new employer plan.

Cash out the balance: Taking a lump sum triggers immediate taxation plus a 10% penalty if you're under age 59½. This option should generally be avoided except in dire circumstances.

Leave the money in the old plan: Many plans allow former employees to maintain accounts with limited management options. This works temporarily but may become impractical over time.

Direct rollovers—where the check is made payable to your new custodian—avoid tax withholding and ensure you don't accidentally trigger taxable events.

Frequently Asked Questions

Can I withdraw money from my 401k before retirement?

Generally, early withdrawals before age 59½ face a 10% penalty plus ordinary income taxes. Exceptions exist for certain hardships, first-time home purchases, qualified education expenses, and IRS-approved coronavirus-related distributions. However, any withdrawal reduces your retirement savings dramatically through lost compounding.

What happens to my 401k if I change jobs?

Your 401k balance can be rolled over to a new employer's plan, transferred to an IRA, left in your former employer's plan (if permitted), or cashed out. Rolling over to an IRA or new employer plan preserves tax-deferred status and avoids penalties.

How much should I contribute to my 401k?

Financial experts recommend contributing 15-20% of your gross income toward retirement. At minimum, contribute enough to receive your full employer match. If that's not possible, start with any amount—even 1-2%—and increase gradually.

Is a 401k better than an IRA?

401k plans offer higher contribution limits ($23,000 vs. $7,000 for IRAs in 2024) and immediate employer matching. IRAs typically offer more investment options and lower fees. Many workers benefit from contributing to both: 401k up to the employer match, then IRA, then returning to max out the 401k.

What is a Roth 401k and should I choose it?

A Roth 401k uses after-tax dollars for contributions but provides tax-free withdrawals in retirement. Choose a Roth if you expect higher taxes in retirement or want tax diversification. Choose a Traditional 401k if you want to reduce current taxable income.

Building Your Financial Future

A 401k represents one of the most powerful wealth-building tools available to American workers. The combination of tax advantages, employer matching, and compound growth potential creates an opportunity that few other financial instruments can match.

Starting early—even with small contributions—leverages time to work in your favor. The difference between beginning at age 25 versus 35 can mean hundreds of thousands of dollars in retirement savings. Don't let procrastination or confusion prevent you from capturing employer matches and tax benefits.

Take time to review your plan options, understand your employer's matching policy, and select appropriate investments for your timeline. Your future self will thank you for the effort you invest today in securing financial independence.