Most investors believe they have diversified portfolios. The reality tells a different story. A 2023 Vanguard study found that only 6% of individual investors maintained truly diversified holdings across multiple asset classes, geographic regions, and sectors. Meanwhile, the SPIVA U.S. Persistence Scorecard documents that over 75% of actively managed funds underperform their benchmarks over 15-year periods—often because concentrated bets fail to deliver consistent returns. Building a portfolio that actually works requires moving beyond the simplistic advice of "don't put all your eggs in one basket" and understanding the mathematical principles that drive real diversification.

This guide provides a strategic framework for constructing a portfolio designed to weather market volatility, capture growth across economic cycles, and align with your specific financial objectives. Whether you're starting with $5,000 or $500,000, the principles remain the same.

What Diversification Actually Means

True diversification is not merely owning multiple stocks or funds. It is the deliberate distribution of capital across uncorrelated assets so that when one segment underperforms, others compensate. The concept originated with Harry Markowitz, whose 1952 research on portfolio theory earned him the Nobel Prize and established the mathematical foundation for modern asset allocation.

The core insight: portfolio risk is not the weighted average of individual asset risks. By combining assets with less-than-perfect correlation, you can reduce overall portfolio volatility without sacrificing expected returns.

Key Correlations to Understand:

- U.S. stocks and bonds typically show correlation around 0.1 to 0.3, providing genuine diversification benefit

- International stocks and U.S. stocks correlate at approximately 0.7 to 0.8, meaning they move together more often than not

- Gold and stocks often show near-zero or negative correlation during market stress

- Real estate investment trusts (REITs) provide diversification while maintaining reasonable correlation to broader equities

The practical implication: owning 50 different technology stocks is not diversified. You're concentrated in a single sector that rises and falls together. True diversification requires exposure to distinct asset classes that respond differently to economic conditions.

The Building Blocks: Asset Classes That Matter

A genuinely diversified portfolio incorporates multiple asset classes, each serving a specific purpose in the overall strategy.

Equities (Stocks)

Equities provide growth potential over long time horizons. Within this category, diversification means across:

- Market capitalization: Large-cap, mid-cap, and small-cap stocks

- Geographic regions: U.S., developed international, and emerging markets

- Sectors: Technology, healthcare, financial services, consumer goods, energy, utilities, and others

Research from Dimensional Fund Advisors spanning decades shows that across nearly every developed market, value stocks have generated higher returns than growth stocks over the long run—a premium that suggests intentional tilts can enhance returns.

Fixed Income (Bonds)

Bonds provide stability, income, and capital preservation. A diversified fixed income allocation considers:

- Duration: Short-term, intermediate-term, and long-term bonds respond differently to interest rate changes

- Credit quality: Government bonds, investment-grade corporate bonds, and high-yield bonds

- Inflation protection: Treasury Inflation-Protected Securities (TIPS) and I-Bonds

The 2022 bond market demonstrated why diversification within fixed income matters: long-term Treasuries lost significant value as rates rose, while short-term bonds and TIPS performed comparatively better.

Alternative Investments

This category has grown to include:

- Real estate: REITs provide exposure to commercial and residential properties without direct ownership

- Commodities: Precious metals, energy, and agricultural products offer inflation hedges

- Private credit: Direct lending and distressed debt strategies (typically available through institutional vehicles)

A 2022 Cambridge Associates study found that institutional investors increasing alternative allocations by 10% saw portfolio volatility decrease by an average of 2.3 percentage points while maintaining similar return profiles.

Strategic Asset Allocation: Your Foundation

Asset allocation—the percentage split among major asset classes—determines approximately 90% of portfolio return variability, according to research from Vanguard and others. This makes it the most critical decision in portfolio construction.

The Classic Starting Points

Conservative Allocation (40% stocks / 60% bonds):

This approach prioritizes capital preservation. Historically, a 40/60 portfolio has delivered approximately 6-7% average annual returns with significantly lower volatility than an all-stock portfolio.

Moderate Allocation (60% stocks / 40% bonds):

The most common "balanced" approach. Historically generated 8-9% average annual returns with moderate volatility—suitable for investors with 10-20 year time horizons.

Aggressive Allocation (80% stocks / 20% bonds):

Designed for younger investors with long time horizons who can tolerate significant short-term volatility. Historically produced 9-10% average annual returns.

Determining Your Target Mix

Your ideal allocation depends on three factors:

Time Horizon: A 30-year-old saving for retirement in 2045 can afford more stock volatility than a 65-year-old drawing income now. The classic "110 minus your age" rule suggests 110 minus age equals stock percentage—a 40-year-old would hold 70% stocks.

Risk Tolerance: This is more nuanced than simple comfort with loss. True risk tolerance encompasses your financial capacity to withstand loss (not just emotional ability), your confidence in earning future income, and your reliance on portfolio returns for goals.

Financial Goals: Retirement accumulation differs from saving for a house in five years. Each goal has its own appropriate allocation.

The CFP Board recommends completing a formal risk tolerance questionnaire and working with a certified financial planner to establish an appropriate target allocation before investing.

Implementation: Building Your Portfolio

With a target allocation established, the next question becomes implementation.

Core-Satellite Approach

This popular structure combines passive core holdings with satellite positions:

Core (60-80% of portfolio):

Low-cost index funds or ETFs tracking broad market indices. A three-fund portfolio—U.S. stocks, international stocks, and bonds—provides remarkably efficient diversification at minimal cost. Vanguard's Total Stock Market ETF (VTI), Total International Stock ETF (VXUS), and Total Bond Market ETF (BND) exemplify this approach.

Satellites (20-40% of portfolio):

Active positions in specific sectors, individual stocks, or alternative investments where you have conviction. This structure captures market returns efficiently while allowing opportunities for outperformance.

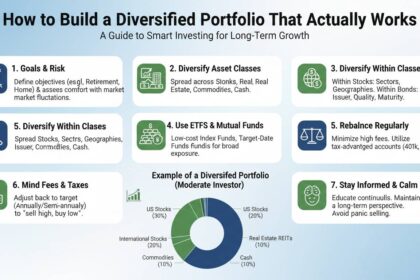

Sample Portfolio Construction

For a moderate 60/40 investor with $100,000:

| Asset Class | Allocation | Example Holdings | Amount |

|---|---|---|---|

| U.S. Large-Cap | 30% | VTI, VOO | $30,000 |

| U.S. Small/Mid Cap | 10% | VXF, IJR | $10,000 |

| International Developed | 12% | VEA, IEFA | $12,000 |

| Emerging Markets | 8% | VWO, IEMG | $8,000 |

| U.S. Bonds | 25% | BND, AGG | $25,000 |

| International Bonds | 10% | BNDX, IAGG | $10,000 |

| Real Estate | 5% | VNQ | $5,000 |

This portfolio provides exposure to thousands of securities across dozens of countries, multiple sectors, and several asset classes.

Tax-Advantaged vs. Taxable Accounts

Placement matters for after-tax returns. Generally:

- Hold tax-efficient investments (index funds, ETFs, municipal bonds) in taxable accounts

- Keep tax-inefficient investments (REITs, high-dividend funds, active funds) in tax-advantaged accounts like IRAs or 401(k)s

- Consider tax-loss harvesting—selling losing positions to offset gains—within taxable accounts

A 2023 Bank of America study found that strategic tax-loss harvesting added 0.3% to 0.5% to annual after-tax returns for taxable accounts.

Rebalancing: Maintaining Your Target Allocation

Over time, market movements cause your allocation to drift. When stocks outperform, they grow to represent a larger percentage than intended—increasing your risk exposure. Rebalancing restores your target allocation.

Rebalancing Methods

Calendar-based: Review and rebalance quarterly, semi-annually, or annually. This simple approach ensures consistent attention to allocation but may trigger unnecessary trades.

Threshold-based: Rebalance when any asset class deviates more than 5 percentage points from target. This method trades less frequently but requires ongoing monitoring.

Contribution-based: Use new contributions to rebalance by directing new money to underweight asset classes. This elegant approach minimizes taxable events in taxable accounts.

Research from Vanguard indicates that rebalancing frequency has minimal impact on long-term returns—consistency matters more than the specific method chosen.

Common Mistakes That Undermine Diversification

Even well-intentioned investors make errors that sabotage their diversification efforts.

Mistake #1: Home Bias

U.S. investors notoriously overweight domestic stocks. While understandable (familiarity, currency convenience), this limits diversification. International markets represent approximately 40% of global market capitalization. A portfolio with zero international exposure misses significant opportunities and increases concentration risk.

Mistake #2: Chasing Recent Performance

The Dalbar Quantitative Analysis of Investor Behavior consistently finds that the average investor underperforms relevant benchmarks by 3-5% annually, primarily due to buying recent winners and selling recent losers. This behavior destroys the mathematical benefits of diversification.

Mistake #3: Over-Confidence in Single Assets

Cryptocurrency, individual stocks, or sector-focused funds often dominate investor conversations. While these can form part of a diversified portfolio, concentration in any single investment contradicts diversification principles.

Mistake #4: Ignoring Bond Duration

Many investors treat all bonds as identical. During 2022, long-term government bonds lost over 30% while short-term bonds declined less than 2%. Duration diversification within bonds is essential.

Mistake #5: Neglecting to Rebalance

Without periodic rebalancing, a portfolio naturally drifts toward the asset classes that performed best—becoming increasingly concentrated and risky over time.

Advanced Strategies for Enhanced Diversification

Once you've mastered the fundamentals, several advanced approaches can further refine your portfolio.

Factor Investing

Rather than market-cap weighting, factor strategies tilt toward specific characteristics historically associated with higher returns:

- Value: Underpriced stocks with low price-to-book ratios

- Small cap: Smaller companies that historically outperform larger ones

- Quality: Companies with high profitability, low debt, and stable earnings

Research from Kenneth French's data library confirms these factor premiums persist across decades and geographies.

Risk Parity

This sophisticated approach equalizes risk contribution from each asset class rather than dollar allocation. A risk-parity portfolio might hold 60% bonds and 40% stocks (rather than 40/60) because bonds are less volatile—achieving similar risk from each component.

Bridgewater Associates' All Weather strategy exemplifies this approach, having delivered relatively stable returns across different economic environments since 1996.

Target-Date Funds

For investors preferring simplicity, target-date funds automatically adjust allocation over time, becoming more conservative as the target date approaches. Morningstar research shows these funds generally deliver results comparable to individual portfolio construction for most investors.

The Human Element: Behavioral Considerations

Understanding your own psychology is essential to maintaining a diversified portfolio through market cycles.

Loss aversion: The pain of losing $1,000 exceeds the pleasure of gaining $1,000. This can cause panic selling during downturns—locking in losses and preventing recovery participation.

Confirmation bias: Investors seek information confirming existing beliefs, potentially ignoring warning signs or alternative perspectives.

Herding behavior: Following the crowd—whether into boom markets or out of crashes—typically produces poor results.

A 2023 Fidelity analysis of 401(k) accounts found that investors who checked their portfolios daily were significantly more likely to make detrimental changes than those who reviewed quarterly or annually.

Frequently Asked Questions

How many different investments do I need for proper diversification?

You don't need dozens of individual stocks. Research from Vanguard indicates that owning 30-50 stocks across multiple sectors essentially eliminates unsystematic (company-specific) risk. A simple three-fund portfolio covering U.S. stocks, international stocks, and bonds provides remarkably effective diversification.

Should I include international stocks in my portfolio?

Yes. International diversification reduces portfolio volatility and captures growth in developing economies. Vanguard research recommends 20-40% international allocation for most U.S. investors. However, consider currency risk and the increasing correlation between global markets when determining your specific allocation.

How often should I rebalance my portfolio?

Annual or semi-annual rebalancing is sufficient for most investors. The specific frequency matters less than maintaining consistency. Consider using new contributions to rebalance (directing money to underweight asset classes) to minimize taxable events in taxable accounts.

What is the biggest mistake investors make with diversification?

The most common error is "false diversification"—believing they're diversified while actually holding concentrated positions. This often occurs when an investor owns many stocks but all within a single sector, or owns multiple funds that all hold similar large-cap U.S. technology stocks. Review your holdings to ensure genuine exposure across asset classes, geographies, and sectors.

Does diversification guarantee positive returns?

No. Diversification protects against permanent loss from individual security failures and reduces volatility, but it doesn't guarantee profits or protect against market declines. During severe market events, correlations between asset classes tend to increase, reducing diversification benefits precisely when they're most needed.

Should I work with a financial advisor for portfolio construction?

If your financial situation is complex—multiple income sources, significant assets, tax considerations, estate planning needs—a fee-only fiduciary financial advisor can provide valuable guidance. For straightforward situations, low-cost index funds through a reputable broker provide excellent diversification at minimal expense.

Building Your Path Forward

Diversification is not a one-time activity but an ongoing commitment to rational portfolio management. The most successful investors focus on the controllable elements: maintaining appropriate asset allocation, minimizing costs, managing taxes, and staying committed to their strategy through market volatility.

Start with a clear assessment of your time horizon, risk tolerance, and financial goals. Establish a target allocation aligned with these factors. Implement through low-cost, broad-market vehicles that provide genuine exposure across asset classes. Rebalance consistently, using new contributions when possible.

Remember that perfect is the enemy of good. A simple, well-executed diversified portfolio will outperform a theoretically optimal portfolio that you're too anxious to maintain. The goal is sustainable, implementable diversification that serves your long-term financial objectives.

Markets will fluctuate. Economic conditions will shift. Your commitment to diversification provides the framework for navigating uncertainty while building lasting wealth.