Compound interest is one of the most useful financial concepts to understand. It can grow your savings significantly over time—or increase your debt if you're not careful. This guide covers what compound interest is, how it works, and why it matters for your finances.

Understanding the Basics of Compound Interest

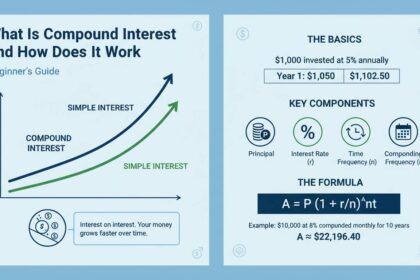

Compound interest is interest calculated on your initial principal plus the accumulated interest from previous periods. Simple interest, by contrast, only earns returns on the original amount. With compound interest, you earn interest on your principal and on all the interest you've already earned. This creates a snowball effect that helps money grow faster over time.

The key difference is how earnings are calculated. With simple interest, you earn interest only on your initial deposit. With compound interest, your earnings themselves earn returns.

Financial advisors often explain that this concept is fundamental to building wealth. One common saying among investment professionals is that compound interest "isn't about how much you start with—it's about giving your money time to grow."

How Compound Interest Works: The Formula

The formula for calculating compound interest is: A = P(1 + r/n)^(nt)

Here, A is the final amount, P is the principal (your initial investment), r is the annual interest rate, n is how many times interest compounds per year, and t is the number of years.

Here's a practical example. If you invest $10,000 at 7% annual interest compounded annually:

- After 10 years: approximately $19,672

- After 20 years: approximately $38,697

- After 30 years: approximately $76,123

Your money more than doubled without adding anything extra.

Compounding frequency matters. Interest can compound annually, semi-annually, quarterly, monthly, or daily. More frequent compounding means more growth. That same $10,000 at 7% would grow to $20,096 over 10 years with daily compounding, compared to $19,672 with annual compounding—a $424 difference.

Small differences in interest rates or compounding frequency lead to big differences over long periods. The growth curve gets steeper as time passes, which is why patience pays off.

The Power of Time: Why Starting Early Matters

Time is the most important factor in compound interest. The earlier you start investing, the longer your money has to grow.

Here's a comparison that surprises many people. Investor A puts $200 per month into an account starting at age 25 and stops at age 35—contributing for just 10 years. Investor B starts at age 35 and contributes $200 per month until age 65—30 years of contributions.

With a 7% annual return, Investor A would have around $303,000 at age 65, while Investor B would have around $202,000. The person who invested for only 10 years ended up with more money because their money had 30 years to compound, while Investor B's contributions had zero years of compounding behind them.

Each year of delay can cost tens of thousands in potential growth. Starting to invest in your 20s—even with small amounts—gives you a real advantage over waiting until your 30s or 40s.

Compound Interest in Investment Vehicles

Different investment options use compound interest in different ways.

Savings accounts pay compound interest, typically monthly. Rates are lower than riskier investments, but your money is secure and easy to access. The FDIC insures deposits up to $250,000 per account holder.

Certificates of Deposit (CDs) offer higher rates in exchange for locking your money for a set period—anywhere from three months to several years.

Bonds pay interest periodically, and bond funds reinvest those payments to buy more bonds, creating compound growth.

Retirement accounts like 401(k)s and IRAs benefit enormously from compound interest. Tax advantages let your investments grow faster than they would in taxable accounts.

Index funds and ETFs track market indexes and automatically reinvest dividends. Over decades, this creates significant wealth for investors who hold steady.

Compound Interest in Debt: The Other Side

Compound interest helps savers, but it hurts borrowers.

Credit card debt is the worst offender. Credit card companies charge interest daily or monthly on balances, and it compounds quickly. A $5,000 balance at 20% annual interest grows fast if you only make minimum payments.

Mortgages also use compound interest, calculated monthly over 15 or 30 years. The total interest often exceeds the original loan amount. A $300,000 mortgage at 6% over 30 years results in roughly $347,000 in interest payments.

Student loans, auto loans, and personal loans all work the same way. Making extra payments toward your principal reduces your balance faster and cuts down on accumulated interest. If you have high-interest debt, paying it off quickly saves you money.

Strategies to Maximize Compound Interest

Here's how to make compound interest work for you.

Start as early as possible. Even small amounts invested in your 20s grow far more than larger amounts started later. Getting into the habit of saving early matters too.

Be consistent. Regular contributions—whether monthly or biweekly—keep the compounding going. Setting up automatic transfers removes the temptation to skip contributions during uncertain times.

Reinvest dividends and earnings. Don't take interest payments as cash. Put them back into your principal to加速 the compounding effect.

Increase contributions over time. As your income grows, invest more. Small annual increases make a big difference over decades.

Choose accounts with more frequent compounding. Monthly beats annual. Daily beats monthly.

Stay focused on the long term. Market ups and downs happen. Staying invested lets compound interest work without interruption.

Conclusion

Compound interest is a fundamental force in building financial security. Whether you're saving for retirement, investing in education, or growing an emergency fund, understanding how it works helps you make better decisions.

The main points: start early, contribute regularly, and keep a long-term perspective. The math works the same for everyone—what differs is whether you use it.

The earlier you begin, the more time your money has to grow. There's no better time to start than today.

Frequently Asked Questions

What's the difference between simple and compound interest?

Simple interest is calculated only on your original principal. Compound interest is calculated on your principal plus all accumulated interest. This makes compound interest much more powerful for building wealth over time.

How often does compound interest typically compound?

It varies. Some accounts compound annually, others monthly or daily. More frequent compounding means more growth. Many savings accounts compound monthly.

Can compound interest work against me?

Yes. When you carry debt, compound interest works against you. Credit cards, loans, and mortgages all use compound interest, so unpaid balances grow larger over time. Paying more than the minimum on high-interest debt saves you money.

How much can I earn with compound interest?

It depends on your rate, initial amount, ongoing contributions, and time horizon. At a 7% annual return, $10,000 invested for 30 years grows to roughly $76,100 with no additional contributions.

Is compound interest guaranteed?

The formula is mathematically consistent, but actual returns depend on how your investments perform. Savings accounts and CDs have guaranteed rates. Stocks and bonds carry risk.

What's the most important factor in compound growth?

Time. Starting even small amounts in your 20s produces more wealth than starting larger amounts in your 40s, because of how the exponential growth works over time.